Original author: PSE Trading Analyst@Daniel flower

introduction

Since the development of blockchain, the DeFi sector has developed the most maturely, and lending is one of its cores. In a bull market, borrowing is often the engine that starts the market. Investors often mortgage BTC and lend USDT to buy BTC, driving the market up while also gaining more excess returns. However, as the craze in the cryptocurrency market fades, The decline in BTC prices also often leads to serial liquidations, with BTC prices falling to freezing points. In order to achieve the goal of the eternal bull market, many no liquidation agreements have been launched in the market, allowing investors to enjoy excess returns without facing the risk of liquidation. This article will analyze several common no liquidation agreements in the market. Let’s sort out the “liquidation” agreement and let’s talk about the conclusion first. The so-called no liquidation is essentially a transfer of risk, but when investors make profits when the wool comes out of the sheep, someone has to bear the risk.

1. The difference between no liquidation agreement

1.1 Use other mortgage assets to liquidate in advance

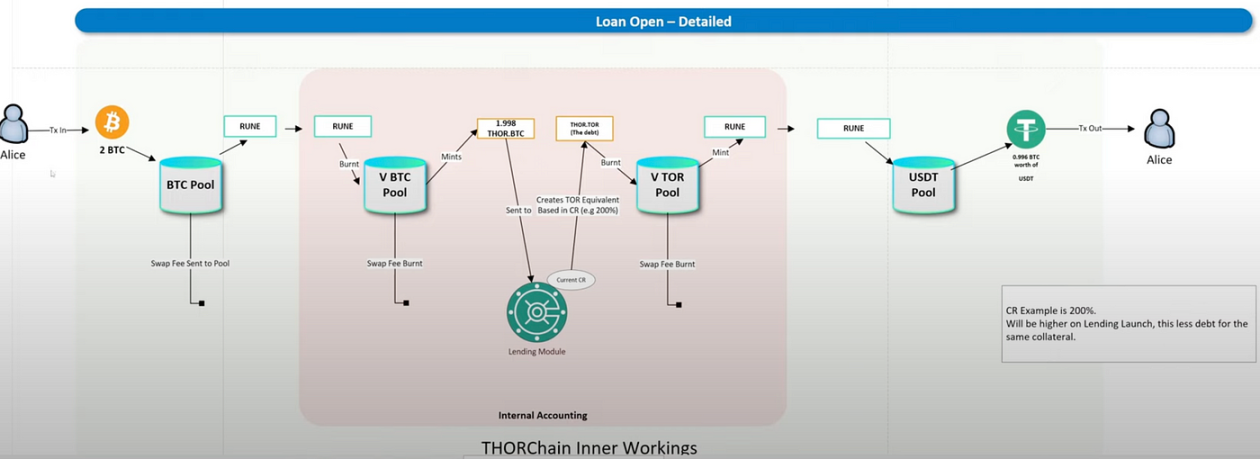

Thorchain is a typical representative. Thorchain is a cross-chain protocol that will establish various asset pools on each chain, such as BTC/RUNE (Rune is the platform currency), etc. When users need to cross assets, they need to add Arb chain Replace BTC with Rune, and then replace Rune with ETH of the OP chain. During the borrowing process, you need to exchange BTC for Rune > Rune, burn to generate Thor BTC (synthetic asset) > Thor BTC, exchange for Thor TOR (official stable currency), burn Mint to generate Rune > Rune, and finally exchange for USDT. In this process, Rune will eventually deflate because USDT is generated by burning, and users need to pay each Swap fee to LP, so no interest is charged for lending. In addition, unlike traditional lending protocols, the end user is mortgage USDT for lending. USDT, so you don’t need to care about the increase in BTC, it will never be “liquidated”, or it has already been “liquidated” in advance.

Figure 1 Thorchain lending method

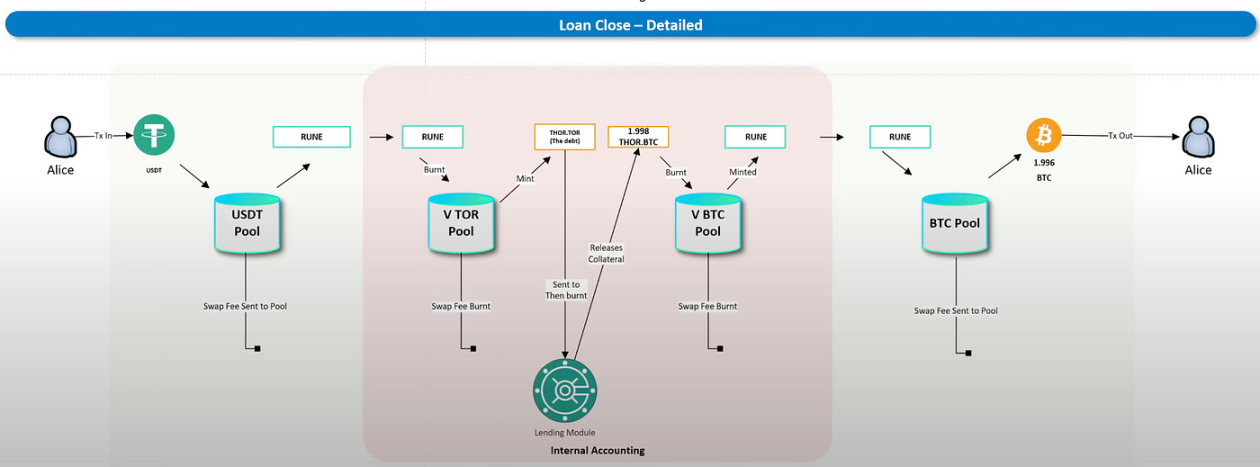

If the agreement has no liquidation and no interest, the lender can never repay the money. However, there is also an extreme situation. When the bull market comes, the lender will want to repay and get more money because of the increase in BTC price. Earnings in BTC. The process is as follows: USDT is replaced with Rune > Rune is burned into Mint to become Thor TOR, Thor TOR is replaced with Thor BTC and then burned to generate Rune, and finally the Rune is swapped into BTC and returned to the customer. In this process, you will find that Rune has become the biggest variable. Mint Rune will get back the mortgaged BTC. If too many people repay the money, unlimited Runes will be minted, eventually leading to a collapse.

Figure 2 Thorchain repayment method

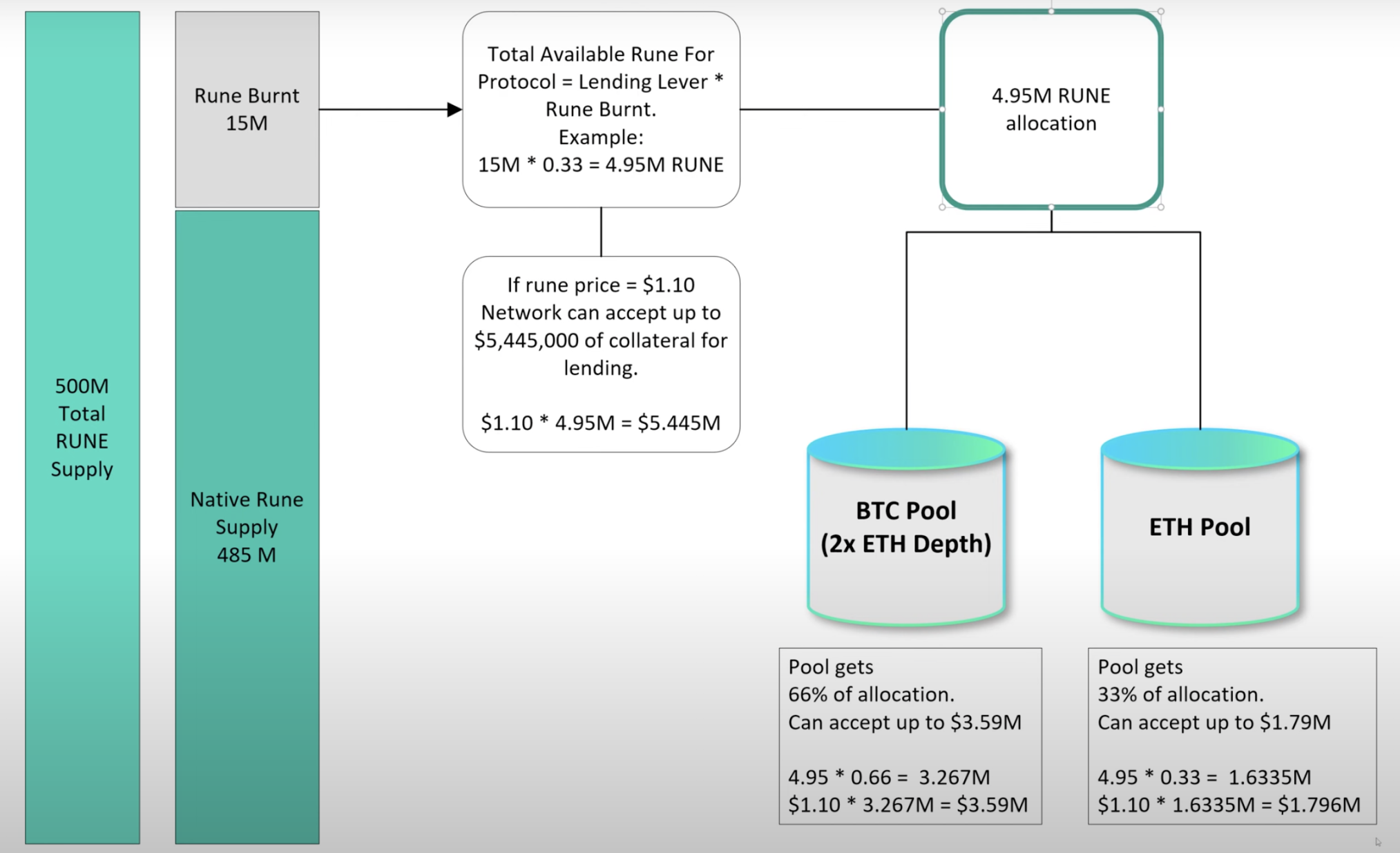

Therefore, Thorchain has set a maximum number of Mint, which is the debt ceiling. The current upper limit is 500 M, and the native Rune is 485 M, which is a Rune that can hold 15 M Mint. Thorchain will set the Lending Level value to be multiplied eventually equal to the amount of Rune that can be burned. Based on the current price of Rune, the value of USDT that can be loaned can be derived.

Figure 3 Total amount of Rune

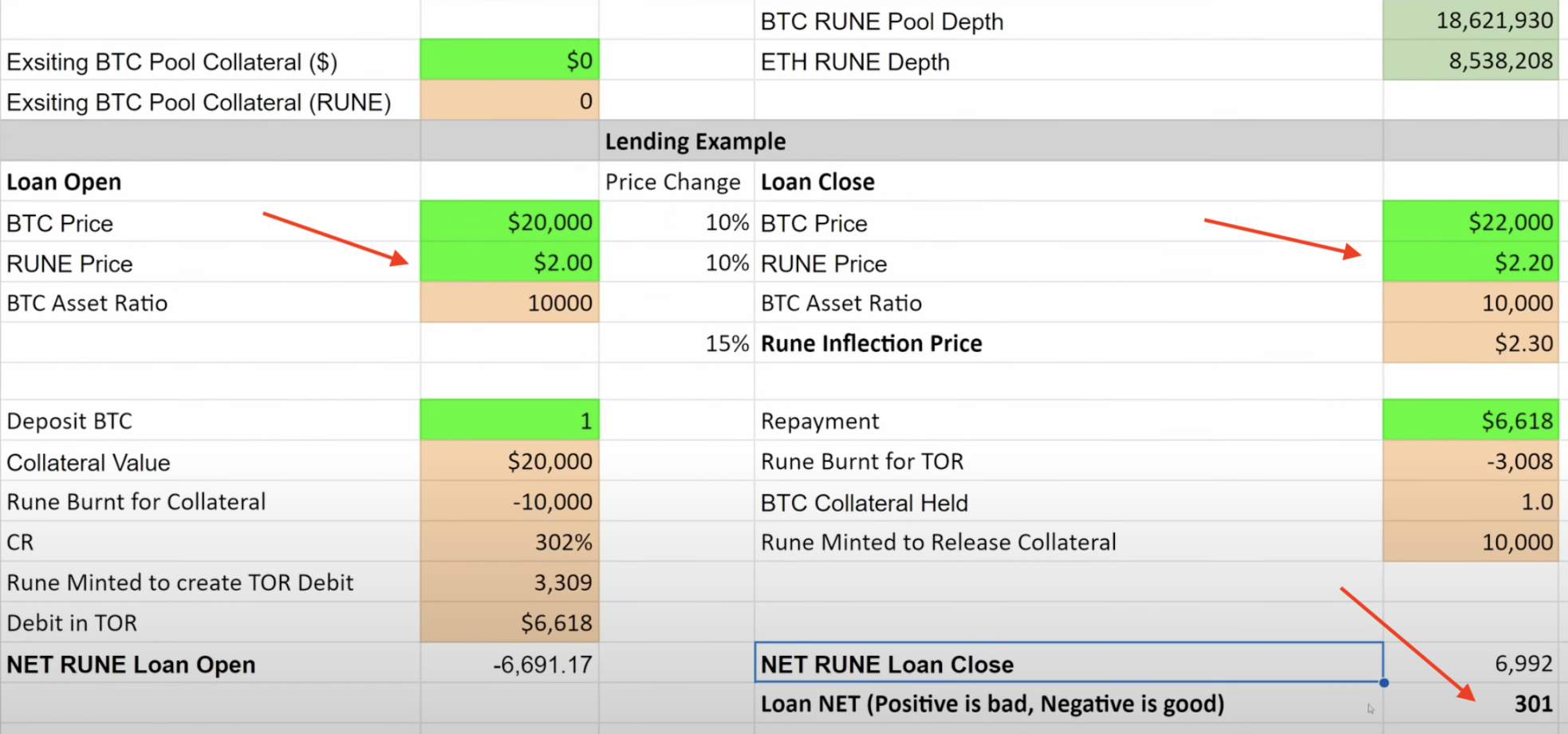

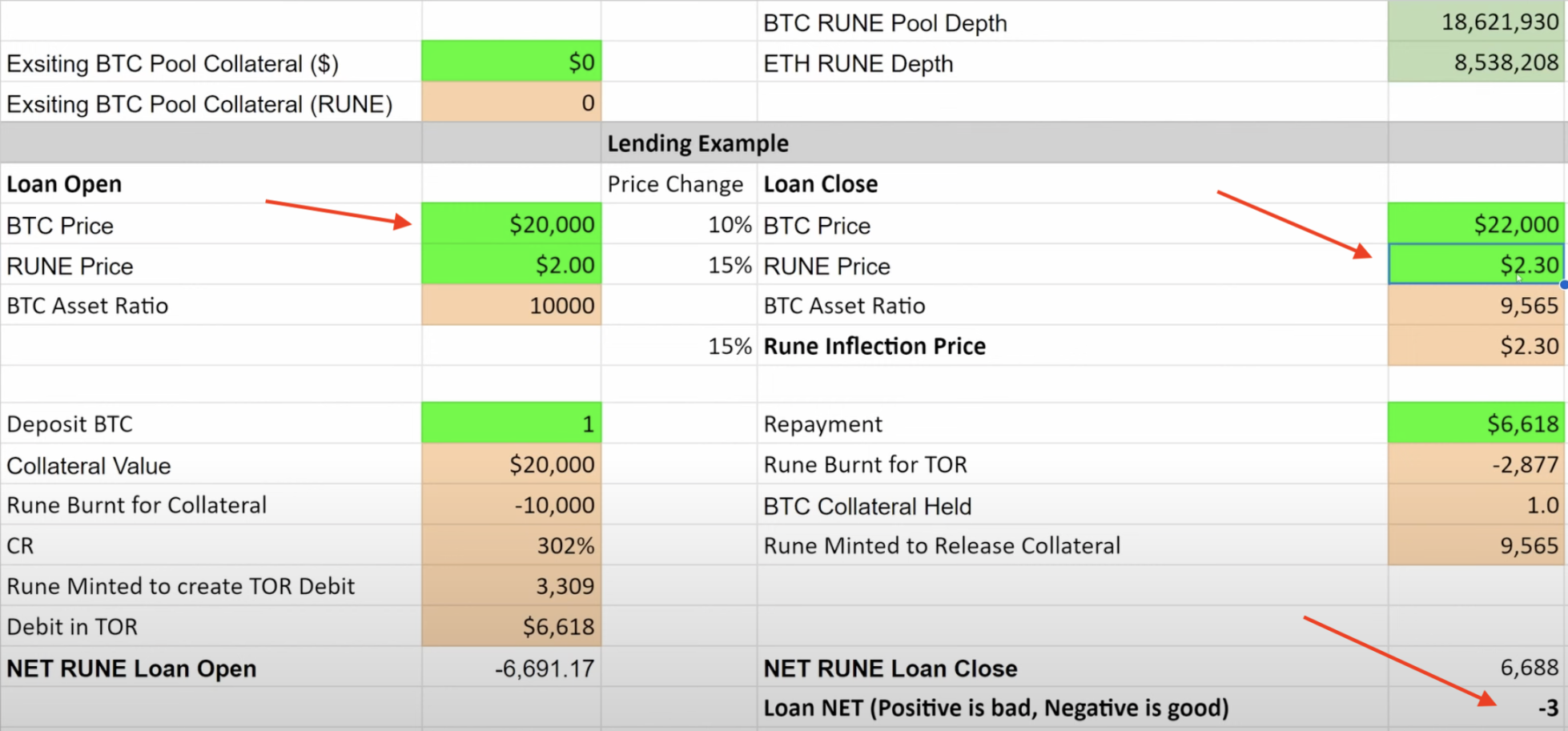

In addition, the ratio of the price of Rune to the price of BTC is also the key to the success of the agreement. As can be seen from the two figures below, when the prices of BTC and Rune increase by 20% at the same time, the user will pay 301 more Rune Mint for repayment, which is equivalent to Compared with Rune that is burned during a loan, when the price of Rune rises by 30%, Rune will not be mint during repayment, and the protocol is still in a state of full deflation. On the contrary, if the price of BTC rises far more than the rise of Rune price, the protocol will mint more Runes, causing the mechanism to collapse. Once the number of Mint is about to reach the online limit, the protocol will increase the Collateral ratio to a maximum of 500%, forcing users to no longer lend more USDT. Assume that it reaches 500 M Runes. Upon its launch, the protocol will also terminate all loan repayments until the price of BTC drops and there is no need to mint more Rune.

Figure 4 The impact of Rune price changes on the protocol

Figure 5 The impact of Rune price changes on the protocol

It is not difficult to see that only when the protocol keeps borrowing money, it is good for the protocol itself (Runes deflation), but it cannot withstand large-scale repayments (Runes inflation), so Thorchains model is destined to be incapable of success. If you want scale, that is the tragedy of Luna 2.0. Secondly, because the number of loans is also controlled through the collateral ratio, the CR of the platform is 200% -500%, which is much higher than the 120-150% of traditional lending platforms such as AAVE. The fund utilization rate is too low, which is not conducive to lending in mature markets. need.

1.2 Transferring liquidation risk to Lender

Cruise.Fi is a mortgage lending platform, and its collateral is stETH. By outsourcing the liquidation line to other Lenders, as long as there are always users taking over, theoretically there will be no liquidation. For loan users: liquidation risk With the reduction, there will be more room for carrying orders, and users who take orders can get more benefits (basic lending income + ETH additional rewards).

Borrowing process: When a user mortgages stETH, USDx will be generated. The user can take USDx to the Curve pool and eventually exchange it for USDC, and the interest generated by stETH will eventually be given to the Lender. There are two ways to maintain the price of USDx

1: When the price of USDx is too high, part of the stETH income will be given to Borrower to subsidize their borrowing costs. 2: When the price of USDx is too low, part of the stETH will be converted into borrowing costs and subsidized to Lender.

Figure 6 Price curve of USDx

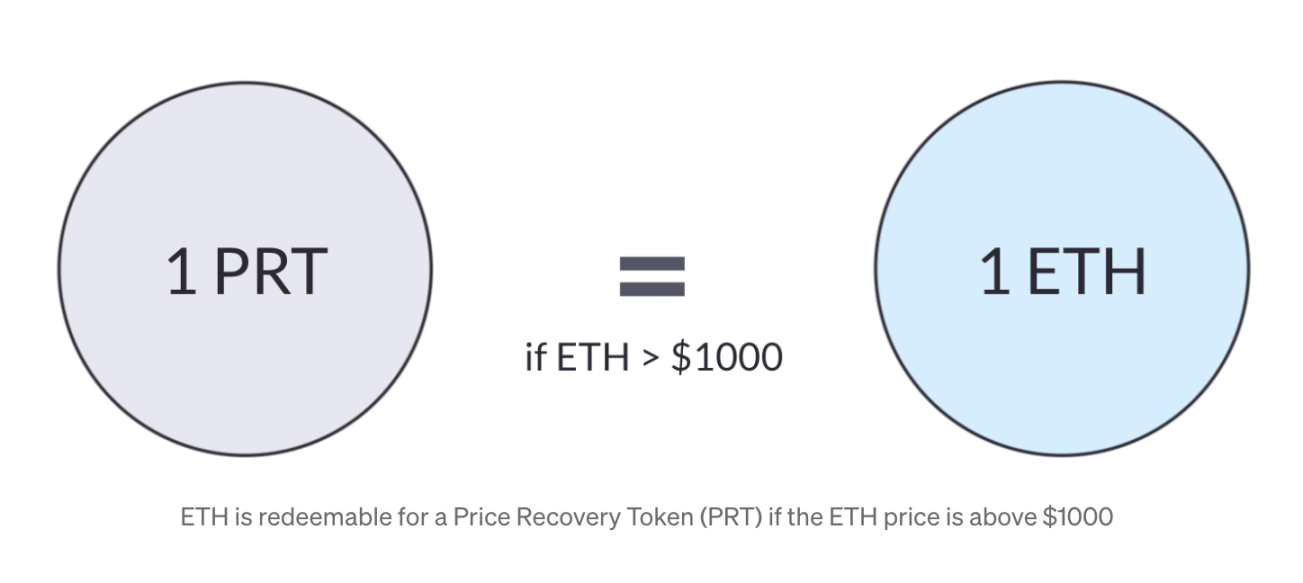

So how does the project achieve non-liquidation? It is assumed here that the mortgaged ETH is $1,500 and the liquidation price is $1,000. When liquidation occurs, the platform will first lock the collateral (stETH), and then give the stETH pledge income to Borrower, and use the stETH pledge income to retain part of the original position. The position exceeding the stETH income will be suspended, but in this way The disadvantage is that when the ETH pledge rate increases, it will affect the income of stETH, resulting in smaller positions that can be retained.

Regarding the positions that were originally to be liquidated, the platform will generate Price Recovery Token. When ETH returns above the liquidation line, Lender can take this part of PRT and exchange it for ETH at a ratio of 1:1. This way, compared with traditional lending platforms, it is much more profitable. It provides a layer of ETH’s excess income, not just loan interest. Of course, if Lender does not believe that ETH will rise above $1,000, Lender can also sell PRT in the secondary market. The project is still in its early stages, and many data and secondary markets are not yet complete. The author also makes a bold prediction , if Lender sells PRT in the secondary market, then Borrower can also take back his position at a lower price (compared to covering the position), and also obtain future excess returns from ETH.

Figure 7 Process of redeeming ETH

But the project also has a drawback. The project can only develop in a bull market (even if a major correction occurs, there will be holders of faith in ETH to provide liquidity). If a bear market comes and market sentiment drops to freezing point, liquidity will dry up. , it will also pose a considerable threat to the platform, and there may not be many users willing to come to the platform to be Lenders, because the agreement itself transfers all risks to Lenders.

1.3 Interest covers borrowing interest rate

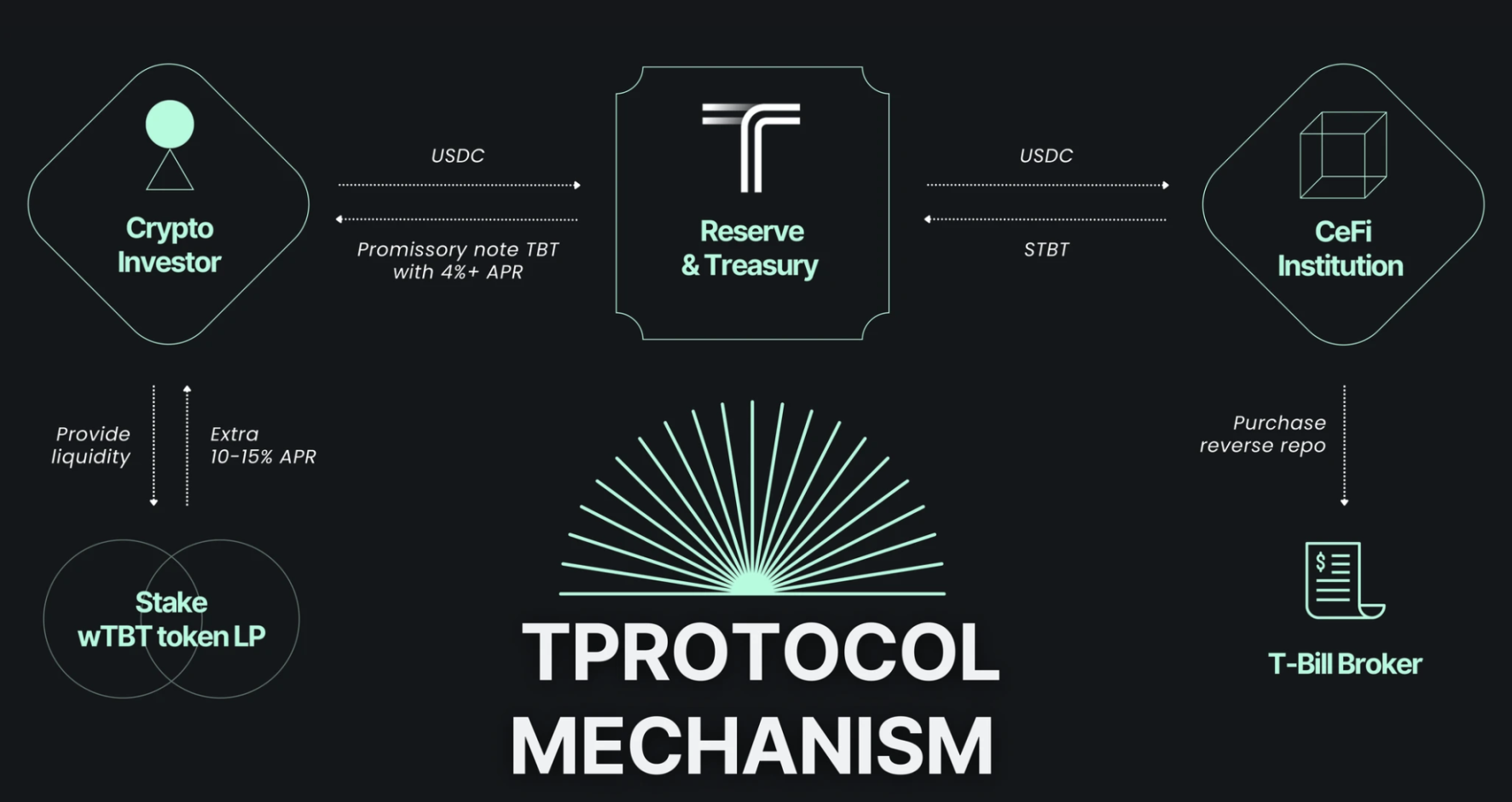

The wave of interest rate hikes by the Federal Reserve has also led to a number of RWA no liquidation protocols. The most noteworthy and largest is T Protocol. STBT is a U.S. bond encapsulation token issued by MatrixDock U.S. institutions, and the U.S. bond yield is 1:1 Rivet, TBT It is a packaged version of STBT issued by T Protocol. It uses the rebase method to issue U.S. bond proceeds to platform users. Users only need to input USDC to mint TBT and enjoy the U.S. bond proceeds.

Figure 8 T Protocol internal process

The biggest highlight is that the interest charged by the platform is always less than the U.S. bond yield. Assuming that the U.S. bond yield is 5%, the interest charged by the platform is about 4.5% and distributed to Lender, of which 0.5% is used as a handling fee, so that MatrixDock can mortgage the U.S. bond package. Tokens can be borrowed interest-free, but how to solve the problem of non-liquidation? Essentially, the platform also adopts the logic of lending US dollars as collateral and is not affected by assets such as BTC. The current LTV is 100%. When MatrixDock mortgages one million U.S. dollars of U.S. debt, it can lend out one million U.S. dollars of stable currency. When the user wants to return his stable currency, MatrixDock will liquidate the U.S. debt he owns. , equal payments will be made to users, and large users need to wait three working days for payment to be completed.

But there are also danger points. When MatrixDock gets the loan, if it makes high-risk investments and other behaviors, the user will be at risk of not being able to redeem U.S. debt immediately. All trust relies on the platform and U.S. debt institutions, and there are regulatory blind spots and opacity. Therefore, T Protocol’s process of seeking cooperation from other U.S. debt institutions has also become extremely slow, and the ceiling is limited. Secondly, with the easing of macro-monetary policies in the future, U.S. bond yields will begin to decline. When interest rates decrease, users will no longer need to deposit on this platform and turn to other lending platforms.

2. Summary and reflection

The author believes that most of the non-liquidation protocols so far are pseudo-liquidation, which actually transfers the risk from Borrower to other places. For example, Thorchain transfers the risk to the protocol itself and those who hold Rune tokens, and Cruise.Fi transfers the risk to the protocol itself and Rune token holders. By moving to Lender, T Protocol has transferred the risk to opaque regulation. It is not difficult to see that these types of agreements all have a pain point: it is difficult to achieve economies of scale, because the borrowing itself is unfair to a certain party, and the short-term high benefits brought about by this unfairness are difficult to achieve. Continuous and unstable for the user. Users will eventually use traditional lending platforms like AAVE to accept liquidation while embracing fairness. The essence of liquidation is insolvency. Any asset will fluctuate. There is no risk-free investment in the world. As long as there are fluctuations, there will be a moment of insolvency. Traditional finance has not been designed from its birth to the present. A perfect risk-free investment without the high volatility of the cryptocurrency world. The no liquidation agreement may reappear in the public eye in a relatively stable manner, but the wool comes from the sheep, and in the end one party will accept a painful price.