Original author: CM (X: @cmdefi)

DeFi is loosened, broker bill is repealed, CAKE governance attack, sUSD continues to decouple, and resumes recent thinking on DeFi:

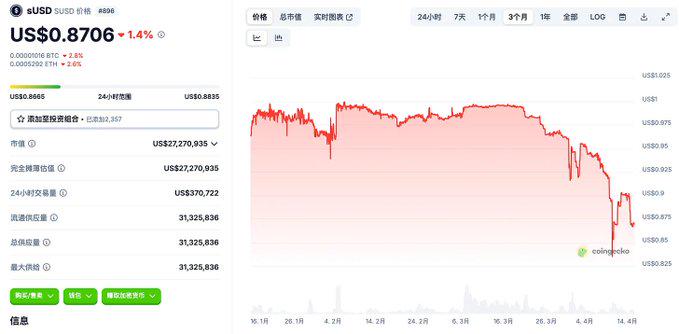

1/ sUSD continues to decouple, why has it not been repaired yet?

Since the SIP-420 proposal was passed at the beginning of the year, sUSD has been depegging and has recently entered a serious depegging range below $0.9. The key change in this proposal is the introduction of the delegation pool. The design of the delegation pool is to encourage users to mint sUSD through this mechanism. The benefits are

- 200% collateralization rate (originally designed to be 500% +)

- Debt can be transferred linearly to the protocol

- After all transfers are completed, users do not need to repay

- The protocol resolves debt through profit and appreciation of $SNX

The advantages are obvious. It improves the minting efficiency of SNX while eliminating the liquidation risk of borrowers. If the market has strong confidence in SNX, it will enter a positive cycle.

But problems immediately emerged:

- The market still has severe PTSD for SNX - sUSD, an endogenous collateral

- Lack of confidence and the improvement of SNX minting efficiency have resulted in additional sUSD flowing into the market, and Curve Pool has seriously deviated

- Due to the design of the delegation pool, users no longer actively manage their debts and cannot repay debts by purchasing low-priced sUSD in the market to arbitrage

The issue that everyone is most concerned about is whether it can return to the anchor. This issue is very dependent on the project party, because the demand or incentive for sUSD must be increased. @synthetix_io is also very clear about this, but whether the market will pay for this kind of algorithmic stablecoin with endogenous collateral is unknown. The sequelae of LUNA are still too great, but from a purely design perspective, the design of synthetix is still advanced, and if it was born in that stable and rough period, it might be favored.

(This does not constitute a buy or sell recommendation, it only states the reasons why things happened for study and research)

2/ veCAKE governance attack, cakepie protocol faces liquidation

What is dramatic is that the ve model itself was designed to prevent governance attacks, but veCAKE was killed by centralized sanctions.

I won’t go into details about the process of this incident. The main controversy is that Pancake believes that @Cakepiexyz_io used governance power to guide CAKE emissions to pools with inefficient liquidity, which is a parasitic behavior that harms Pancake’s interests.

But this result does not violate the operating principle of the ve mechanism. Cake emission is determined by the locked vlCKP, the governance token of cakepie. vlCKP is the representative of governance power and can form a bribery market. This is the significance of the existence of protocols such as cakepie and convex.

The relationship between Pancake - cakepie and Curve - Convex is basically the same. Frax and Convex benefited from the accumulation of a large number of veCRV votes, and the design of the ve model did not directly link the handling fee and emissions. The unreasonable emission guidance problem pointed out by cakepie is the result of insufficient competition for governance rights from a market perspective. The conventional practice is to wait for or promote market competition. If human intervention is required, there are actually better human adjustment solutions, such as setting an incentive cap on the pool, or encouraging more people to compete for vecake votes.

3/ Following the veCAKE governance attack above, Curve founder @newmichwill gave a quantitative calculation method:

- Measures the number of CAKEs that are locked as veCAKEs via Cakepie (these CAKEs are permanently locked).

- Compare a hypothetical scenario: If the same veCAKE is used to vote for the Quality Pool and all proceeds are used to buy back and destroy CAKE, how much CAKE will be destroyed?

- Through this comparison, it can be determined whether Cakepies behavior is more efficient than directly destroying CAKE.

According to Michael’s experience, on Curve, the veToken model is about 3 times more efficient in reducing the circulation of CRV tokens than directly destroying tokens.

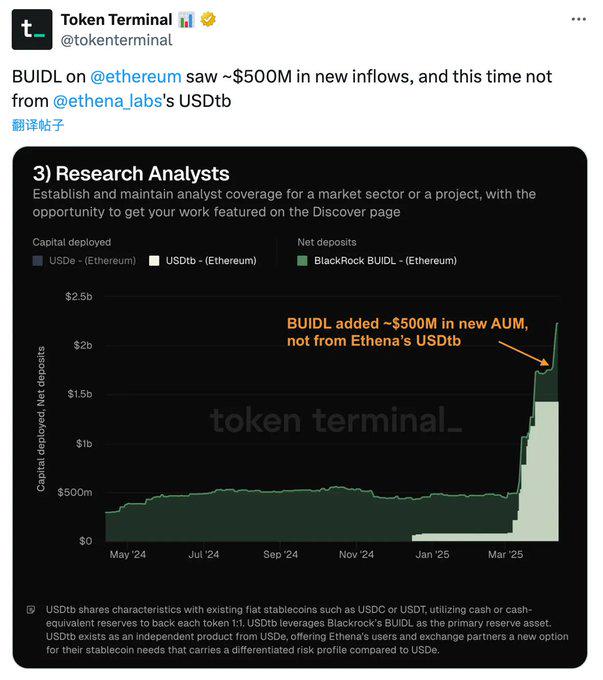

4/ BUIDL continues to grow, up 24% in 7 days

(1) Last time we paid attention to the breakthrough of 2 billion, and now it is close to breaking through 2.5 billion

(2) The latest $500 million increase did not come from Ethena

(3) May have attracted new investor groups

(4) From the traces on the chain, it may come from Spark, a lending protocol under Sky (MakerDAO).

The RWA business has continued to grow, but has not been well integrated into the DeFi Lego, and is currently in a state of being out of touch with the market and irrelevant to retail investors.

5/ IRS DeFi Broker Bill Officially Repealed

On April 11, US President Trump signed a bill announcing the official repeal of the IRS DeFi crypto broker rules.

The DeFi sector has risen, but not much. I personally think that this is actually a major positive for DeFi. The regulatory attitude is loosening up DeFi, which may unlock the possibility of more application innovation.

6/ Unichain launches liquidity mining, $5 million in $UNI tokens rewarded to 12 pools

Tokens involved: USDC, ETH, COMP, USDT 0, WBTC, UNI, wstETH, weETH, rsETH, ezETH

It has been 5 years since Uniswap last conducted liquidity mining. The last time was in 2020 with the launch of UNI tokens. This time the goal is to guide liquidity for Unichain. It is estimated that many people will go to mine and get the opportunity to obtain UNI tokens at a low cost.

7/ Euler expands to Avalanche, TVL has entered the top 10 lending protocols

(1) TVL increased by 50% in one month

(2) Most of the growth came from incentives, primarily from Sonic, Avalanche, EUL, etc.

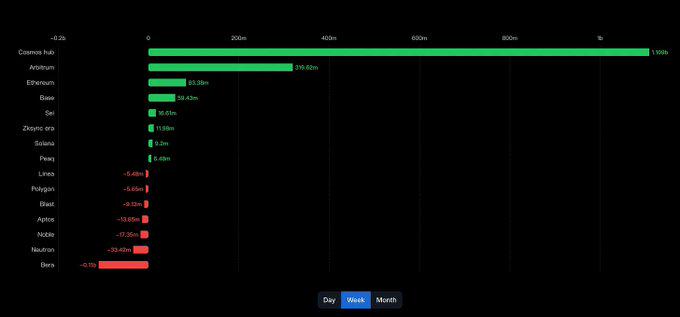

8/ Cosmos IBC Eureka is officially launched

(1) Based on IBC v2

(2) Gas $ATOM destroyed for each transaction

(3) Support cross-chain between Cosmos and EVM

(4) Currently supports mainstream assets on Ethereum mainnet and Cosmos, but has not yet been expanded to L2

(5) In the past week, the Cosmos hub has received $1.1 billion in cross-chain inflows

Strong empowerment has been introduced for ATOM. Any chain in Cosmos that can attract a large amount of capital will likely drive the value growth of ATOM, and the situation in which the ecological explosion that occurred during the LUNA period could not be associated with ATOM will be improved.

While there has been a significant inflow of funds in the last week, if ATOM’s fundamentals are to shift, sustainability needs to be examined.

9/Buyback

(1) AaveDAO officially starts buying back tokens

(2) Pendle proposed to list PT token on Aave

10/ Berachain farming

(1) Update the POL reward distribution rules and set a 30% upper limit on the distribution ratio of a single Reward Vault

(2) Berachain governance update introduces a new Guardian Committee responsible for reviewing and approving RFRV

(3) OlympusDAO is preparing to move some POL liquidity in response to new rules to maintain high incentives for the $OHM pool

(4) Yearn’s $yBGT is now available on Berachain

After Berachain experienced a golden March, the price and TVL of the coin have entered an adjustment period. The official has made modifications and restrictions on the unreasonable incentive distribution issues exposed. Although TVL has been flowing out in large amounts in the past few weeks, it is still one of the most DeFi chains. Continue to observe more protocol integrations and TVL inflows.