In the previous article, the Crypto Salad team explored the core concept of stablecoins in depth and conducted a systematic analysis of the operating mechanisms and application scenarios of mainstream stablecoins in the current market. It is not difficult to see from the analysis that the stablecoin track has huge growth potential. However, as a double-edged sword, the technological innovation of stablecoins has broad development prospects, but its potential risks cannot be ignored. According to the 2024 Global Crypto Crime Report released by Chainalysis, an on-chain analysis agency, the total amount of illegal transactions completed through stablecoins reached US$40 billion between 2022 and 2023 alone. Among them, 70% of crypto fraud crimes and more than 80% of sanctions evasion transactions used stablecoins.

Therefore, in order to balance innovation and risk, global regulators are accelerating the construction of a systematic regulatory framework for stablecoins: the United States continues to advance relevant legislative processes such as the Stablecoin Transparency Act (STABLE Act), and the Hong Kong Monetary Authority has passed the Stablecoin Ordinance and established a Stablecoin Sandbox regulatory mechanism. This dynamic balance between technology neutrality and risk prevention and control is shaping the next stage of stablecoin development paradigm, and also marks that the stablecoin industry is evolving from wild growth to compliance.

What are the risks of stablecoins and why do they need to be regulated?

Which countries and regions have currently established regulatory frameworks for stablecoins?

What are the specific contents of the regulatory framework? What are the entry barriers and compliance requirements for the stablecoin industry?

In the long run, what impact will the continuous improvement of the regulatory framework have on the future development of the stablecoin industry?

The Crypto Salad team has been deeply involved in the cryptocurrency industry for many years and has rich experience in dealing with complex cross-border compliance issues in the cryptocurrency industry. In this article, we will combine relevant industry research and the Crypto Salad team’s practical experience to sort out and answer the above questions from the perspective of professional lawyers.

What are the risks of stablecoins and why do they need to be regulated?

Why is the regulatory framework for stablecoins so important? Currently, there are two major risks in the stablecoin industry:

1. The inherent risk of stablecoins

The value stability of stablecoins is not absolutely guaranteed, but is based on the balance between market consensus and trust mechanisms. The core logic is that the relative stability of stablecoins does not come from the intrinsic value of reserve assets, but relies on the holders continued trust in the issuers ability to perform. This trust is essentially a consensus-driven currency balance - when most market participants trade and transfer based on the expectation of stable value of stablecoins, the risk of large price fluctuations will be suppressed by the consensus itself.

However, once the foundation of trust is broken, the stability of stablecoins will quickly collapse. For example, when the market perceives such risks, such as insufficient reserve assets or misappropriation of funds, the consensus mechanism of stablecoin holders may quickly reverse or collapse. Specifically, the panic selling of stablecoin holders will cause the currency value to depeg, and the market panic caused by the depegment of the currency value will further stimulate the selling tide, and finally form a self-reinforcing negative feedback loop - the so-called death loop. Even more, the collapse of a single stablecoin will eventually trigger a series of chain reactions in the cryptocurrency market, and eventually become a black swan event in the overall market.

This transmission mechanism of systemic risk was fully verified in the Luna-UST incident in 2022. As a representative of algorithmic stablecoins, UST relies on a complex algorithmic mechanism with the Luna token to maintain the currency value pegged to the US dollar. However, when the market liquidity crisis broke out, the inherent defects in the algorithm design were continuously magnified after malicious attacks. At the same time, the lack of transparency of UST further led to the rapid spread of the trust crisis and ultimately caused the currency value to collapse. This incident not only caused the evaporation of nearly US$40 billion in market value, but also further triggered a chain reaction in the crypto market, fully exposing the inherent risks contained in stablecoins that lack regulatory constraints.

Second, the external risks of stablecoins

The anonymity and cross-border liquidity of stablecoins have brought them significant convenience and advantages, but these characteristics also make them extremely easy to be exploited by black and gray industries and illegal criminal activities . Without effective supervision, especially unclear anti-money laundering (AML) and counter-terrorist financing (CFT) compliance requirements for stablecoins, stablecoins are likely to become a hidden channel for illegal capital flows, thereby posing a threat to the security of the financial system.

An Introduction to the Regulatory Framework of Stablecoins in the United States and Hong Kong

In recent years, the development of the global stablecoin regulatory framework has shown a rapid development trend. Hong Kong, the United States, Singapore, the European Union, the United Arab Emirates and other countries or regions are rapidly advancing and gradually implementing relevant laws and regulations.

Overall, the current regulatory frameworks for stablecoins in various countries are mainly centered around the following three major directions:

Entry threshold for issuers: Clarify the qualification requirements for stablecoin issuers to ensure that they have sufficient capital strength, risk management capabilities and industry experience.

Maintenance of currency stabilization mechanism and reserve assets: Issuers are required to maintain sufficient stablecoin reserve assets and ensure transparency and compliance through regular disclosure and independent audits.

Compliance in the circulation link: focus on strengthening the anti-money laundering (AML) and “know your customer” (KYC) mechanisms of stablecoins to prevent stablecoins from being used for illegal capital flows.

Next, this article will focus on Hong Kong and the United States, deeply analyze their latest stablecoin regulatory frameworks, and discuss them from the following dimensions: regulatory process, regulatory documents, regulatory authorities, and the core content of the regulatory framework.

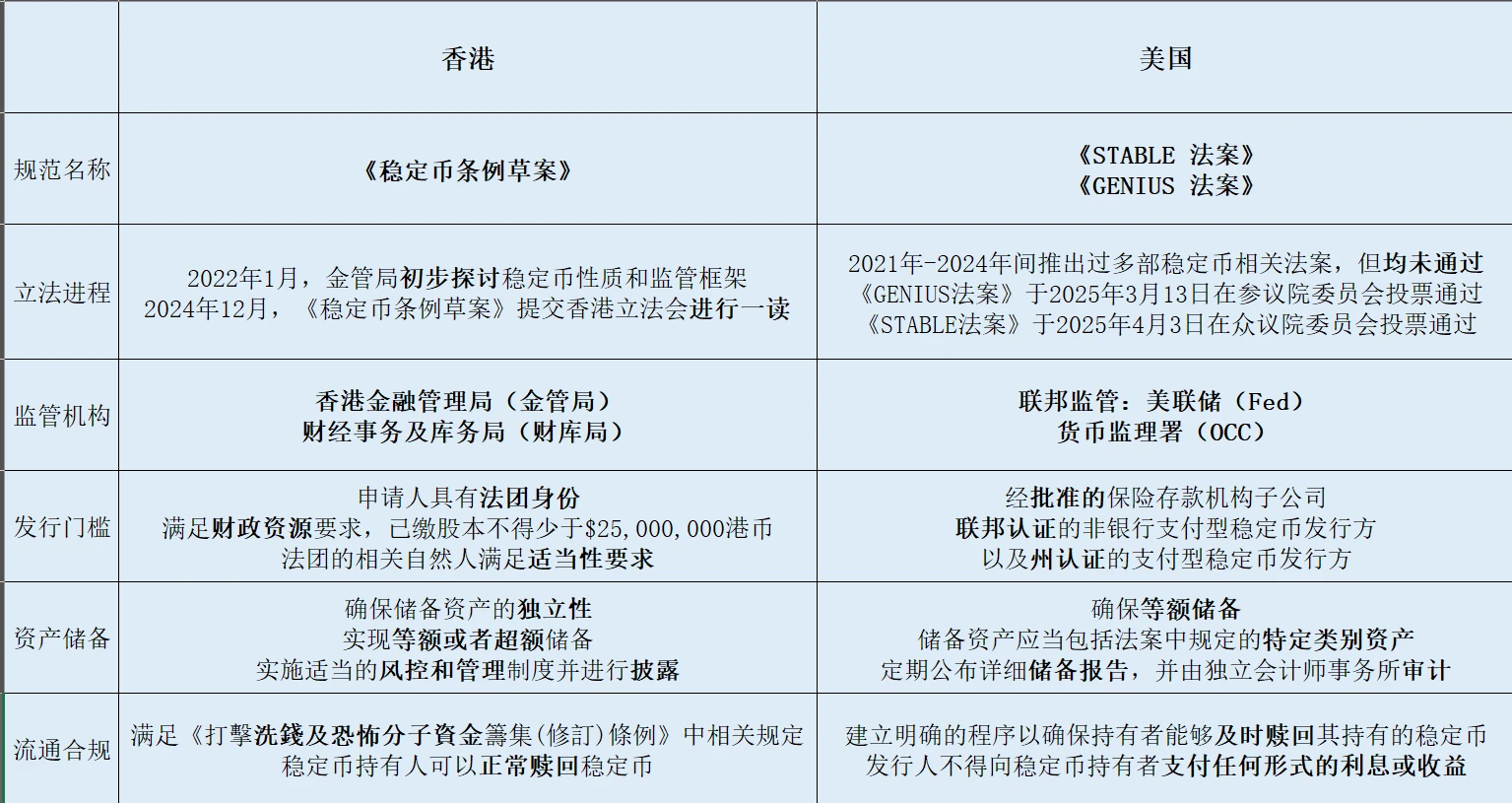

(The above figure is a comparative summary of the stablecoin regulatory frameworks in the United States and Hong Kong)

1. Hong Kong

1. Regulatory process

January 2022:

The Hong Kong Monetary Authority (hereinafter referred to as the “HKMA”) has published the “Discussion Paper on Crypto Assets and Stablecoins”, and has begun preliminary exploration of the nature of stablecoins and the relevant regulatory framework.

December 2023:

The HKMA and the Financial Services and the Treasury Bureau (FSTB) jointly issued the Consultation Document on Legislative Proposals for Implementing a Regulatory Regime for Stablecoin Issuers in Hong Kong, proposing a specific draft stablecoin regulatory framework. The document focuses on supervising issuers and protecting holders.

March-July 2024:

The Monetary Authority of Singapore has launched the Stablecoin Sandbox program and introduced a Sandbox for stablecoin issuers. Yuanbi Technology, JD Coin Chain and other companies have become the first participants in the Sandbox.

December 2024:

On December 6, 2024, the Hong Kong government published the Stablecoin Bill (hereinafter referred to as the Stablecoin Bill) in the Gazette and submitted it to the Hong Kong Legislative Council for first reading on December 18.

According to Hong Kong’s legislative procedures, before a bill becomes a formal law, it must complete the three-reading process of the Hong Kong Legislative Council, namely the first reading, the second reading and the third reading. In essence, this is a three-stage reading and deliberation of the bill. Therefore, the Stablecoin Ordinance must also complete this process before it is officially signed into law, and it is optimistically estimated that it may be completed within 2025.

2. Legal texts and corresponding regulatory authorities

The core regulatory document of Hong Kongs stablecoin regulatory framework is the Stablecoin Ordinance issued in December 24, and the regulatory system of Hong Kongs stablecoin is mainly responsible for the HKMA and the Treasury Department mentioned above.

3. Regulatory framework and main contents

a. Definition of Stablecoin

First, the Stablecoin Regulations first clarified the broad definition of stablecoin. Article 3 of the Stablecoin Regulations stipulates that stablecoins should have the following characteristics:

It is a unit of account or a form of storage of economic value;

A medium of exchange accepted by the public that can be used to purchase goods or services, settle debts, or make investments;

Deployed on a distributed ledger system and capable of being transferred, bought, sold and stored electronically;

Reference a single asset or basket of assets to maintain a stable value.

It should be noted that Hong Kongs Stablecoin Ordinance does not regulate all stablecoins in a broad sense, but specifically regulates specified stablecoins that meet specific conditions. Article 4 of the Stablecoin Ordinance clearly stipulates that stablecoins that maintain currency stability with full reference to one or more official currencies are specified stablecoins regulated by this Ordinance.

b. Regulated stablecoin-related activities

After clarifying the concept of stablecoins and specifying stablecoins, Article 5 of the Stablecoin Regulations points out the stablecoin-related activities that are subject to the regulations and require a license, such as

Issuing specified stablecoins in Hong Kong;

Issuing specified stablecoins pegged to the Hong Kong dollar in countries or regions outside Hong Kong;

And actively promote their ongoing stablecoin-related activities to the public.

c. Entry threshold for issuers

If you want to engage in regulated stablecoin-related activities, you need to obtain the corresponding stablecoin issuance license under the regulatory framework of the Stablecoin Regulations. The entry conditions for obtaining the license include but are not limited to the following:

Firstly, the license applicant must have legal status , either a company established in Hong Kong or a banking institution established outside Hong Kong.

Secondly, license applicants who want to engage in stablecoin-related activities need to meet basic financial resource requirements to meet their due obligations. Specifically, the paid-up capital of the license applicant must not be less than HK$25,000,000.

Finally, the shareholders, directors, actual controllers, senior executives and other relevant natural persons of the license applicant also need to meet the corresponding suitability requirements in the Stablecoin Regulations, which will not be discussed here.

d. Currency stabilization mechanism and maintenance of reserve assets

Regarding the management of reserve assets of designated stablecoins, the “Designated Stablecoins” stipulates the following:

First, the licensee needs to ensure that the reserve asset portfolio of the designated stablecoin is strictly separated from other assets to ensure the independence of the reserve assets.

Secondly, at all times, the market value of the reserve asset portfolio of the designated stablecoin must be greater than or equal to the circulating face value of the stablecoin in order to achieve equal or excess reserves.

Finally, licensees need to implement appropriate risk control policies and management systems for reserve assets, and make timely and complete disclosures to the public on the management policies, risk assessments, composition and market value of their reserve assets, and the results of regular audits.

e. Compliance requirements in the circulation process

First, the Stablecoin Ordinance clearly stipulates that licensees need to establish a special risk management system, which must comply with the relevant provisions of the Anti-Money Laundering and Terrorist Financing (Amendment) Ordinance promulgated in 2022 and prevent money laundering or terrorist financing activities related to its specified stablecoin activities.

Secondly, each holder of a specified stablecoin must have the right to redeem the stablecoin , and the issuance of the specified stablecoin shall not impose any overly stringent conditions to restrict the redemption of the stablecoin, nor shall it charge unreasonable fees related to the redemption.

f. Hong Kong Stablecoin Sandbox

While launching the Stablecoin Ordinance, the Hong Kong Monetary Authority also established a corresponding Stablecoin Sandbox mechanism to provide a testing environment and compliance support for relevant stablecoin issuers. Currently, there are many stablecoin issuers in the sandbox that have passed the initial approval of the HKMA, including Yuanbi Technology, JD.com and Standard Chartered Bank. These issuers are expected to become the first batch of entities to issue compliant stablecoins in Hong Kong.

Although the stablecoin sandbox mechanism was launched and tested last year, the relevant entities have not yet officially completed the official issuance of stablecoins. The Crypto Salad team learned that the stablecoin issuers in these sandboxes may officially launch stablecoin products that meet Hong Kongs compliance requirements in 2025.

2. United States

1. Regulatory process and regulatory documents

To understand the current regulatory framework for stablecoins in the United States, the two core regulatory documents are the Guiding and Establishing National Innovation for US Stablecoins Act (hereinafter referred to as the “ GENIUS Act ”) and the Stablecoin Transparency and Accountability for a Better Ledger Economy Act (hereinafter referred to as the “ STABLE Act ”).

The GENIUS Act was introduced by Senator Bill Hagerty and supported by several senators. The bill was passed by the Senate on March 13, 2025 with 18 votes in favor and 6 votes against. The STABLE Act was introduced by U.S. Representatives Bryan Steil and French Hill and passed by the House Financial Services Committee on April 3, 2025 with 32 votes in favor and 17 votes against.

According to the legislative process of the United States, the STABLE Act, which has been reviewed and passed by the House Financial Services Committee, will be submitted to the Senate or the House of Representatives for plenary debate. The bill needs to be passed by a majority in the Senate and the House of Representatives respectively and reach a consensus, and finally signed by the President to become a formal law.

It is important to note that the two bills are not mutually exclusive or contradictory. On the contrary, the positioning of the STABLE Act is based on the improvement and continuation of the GENIUS Act. Bryan Steil, Chairman of the U.S. House of Representatives Digital Assets Subcommittee, told reporters that after a new round of deliberations, the STABLE Act will be well aligned with the Senates GENIUS Act, which was achieved after several rounds of draft revisions in the House and Senate and technical assistance from the SEC and CFTC. In fact, there are 20% differences between the bill and the GENIUS Act, and these differences are only textual, not significant or substantive differences.

2. Corresponding regulatory authorities

To date, the regulation of stablecoins in the United States is still fragmented, and there is no unified federal framework to regulate the issuance and operation of stablecoins. This regulatory ambiguity has led to overlapping jurisdictions among federal agencies, while inconsistencies between state laws have further exacerbated regulatory complexity.

Currently, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) currently have primary regulatory authority over the stablecoin market. The SEC believes that many stablecoins are structurally similar to money market mutual funds and therefore argues that they should be subject to securities regulations.

However, on June 28, 2024, the U.S. District Court for the District of Columbia ruled in favor of Binance and rejected the SECs claim that the stablecoin BUSD is a security. BUSD is issued by Paxos in partnership with Binance and is regulated by the New York State Department of Financial Services (NYDFS). This ruling is consistent with previous judicial decisions on stablecoins and further emphasizes that stablecoins like BUSD and USDC - because they are pegged to fiat currencies at a 1:1 ratio - do not inherently meet the definition of investment contracts within the jurisdiction of the SEC.

On the other hand, the CFTC regulates some stablecoins by identifying them as commodities . CFTC Chairman Rostin Behnam told reporters in 2023 that stablecoins are commodities, so in the absence of explicit instructions from Congress that they are other types of assets, we must regulate this market. For example, the CFTC once fined Tether $41 million for violating relevant regulations on sanctioned transactions with its USDT.

In summary, the lack of a unified legal framework not only complicates the compliance work of stablecoin issuers, but may also pose financial stability risks to investors. Therefore, there are also views that incorporating stablecoins into a regulatory framework similar to that of banks may help reduce the systemic risks of stablecoins while providing the market with clearer compliance guidance.

The GENIUS Act and the STABLE Act have clarified the previously complex and confusing regulatory framework to a certain extent. Specifically, issuers of stablecoins with a market value of more than $10 billion will be regulated at the federal level. The Federal Reserve (Fed) is responsible for regulating depository institution issuers, while the Office of the Comptroller of the Currency (OCC) is responsible for regulating non-bank issuers. At the same time, state regulators are also allowed to regulate issuers of stablecoins with a market value of less than $10 billion. Therefore, the above two bills have established a parallel pattern of federal and state regulatory systems, hoping to provide a more comprehensive and systematic regulatory model for the stablecoin industry in the United States.

3. Regulatory framework and main contents

Next, we will analyze in detail based on the newly enacted STABLE Act.

a. Definition of Stablecoin

The bill stipulates that payment stablecoins regulated by this law should have the following characteristics:

A digital asset that is intended to be used as a means of payment or settlement;

Denominated in national currency;

The issuer is obliged to exchange, redeem or repurchase the bond for a fixed amount of monetary value;

It is not a national currency and is not a security issued by an investment company.

b. Entry threshold for issuers

Only “Permitted Payment Stablecoin Issuers” can issue stablecoins, including:

An approved insured depository institution subsidiary;

Federally certified non-bank payment stablecoin issuers;

and state-certified payment stablecoin issuers;

c. Currency stabilization mechanism and maintenance of reserve assets

The issuer needs to ensure that the reserve assets cover 100% of the total outstanding liquid stablecoins (i.e. 1:1 backing), and the reserve assets should include the following categories:

Cash in US dollars;

Federal Reserve Bank deposits;

demand deposits with insured depository institutions;

short-term U.S. Treasury bills maturing in 93 days;

Overnight repurchase agreements that meet certain conditions;

A money market fund that invests in the above assets.

At the same time, the issuer should publicly publish a detailed report on the composition of the reserve fund every month, which should be audited by an independent registered accounting firm. In addition, the report should be accompanied by a written certification from the companys Chief Executive Officer (CEO) and Chief Financial Officer (CFO) to ensure the authenticity and completeness of the information.

Finally, issuers must comply with capital adequacy, liquidity management, and risk management requirements set by the primary federal payment stablecoin regulator. Risk management covers key areas such as operational risk, compliance risk, information technology risk, and cybersecurity risk.

d. Compliance in the circulation process

First, issuers should publicly disclose the redemption policy of stablecoins and establish clear procedures to ensure that holders can redeem their stablecoins in a timely manner.

Second, issuers are not allowed to pay any form of interest or income to stablecoin holders to avoid potential conflicts of interest and market distortions.

Crypto Salad Explanation

The Crypto Salad team believes that the acceleration of the construction of stablecoin regulatory frameworks by major economies around the world actually reveals the core value of stablecoins in different dimensions:

First of all, as an indispensable key infrastructure in the digital asset market, stablecoins are accelerating the breakthrough of the boundaries of the on-chain ecology and are deeply embedded in the operating links of the traditional financial system and the real economy , thus achieving a deep integration of the on-chain and off-chain value systems.

Secondly, at the critical juncture when the global financial landscape is undergoing profound adjustments and the trend of de-dollarization is accelerating, stablecoins will play a more critical role in the game of the international monetary and financial system, and become an important strategic tool for countries to maintain their monetary sovereignty and financial security.

Finally, with the continuous optimization of stablecoin regulatory mechanisms in various countries, the stablecoin industry will inevitably enter a new stage of balanced development between standardization and innovation . This requires stablecoin issuers to further enhance their compliance capabilities within the regulatory framework, and also provides institutional space for them to explore new business paradigms. In the future, the development of the stablecoin industry will find new growth momentum and value creation points in the global financial regulatory system through technological iteration and institutional adaptation.

Special statement: This article only represents the personal views of the author and does not constitute legal advice or legal opinion on specific matters.