Ethena is a rare phenomenal DeFi project in this cycle. After its token was launched, its circulating market value once exceeded 2 billion US dollars (corresponding to FDV of more than 23 billion). However, since April this year, its token price has fallen rapidly. Ethenas circulating market value has retreated by more than 80% from its peak, and the token price has retreated by as much as 87%.

Since September, Ethena has accelerated its cooperation with various projects and expanded the use scenarios of its stablecoin USDE. The scale of stablecoin has also begun to bottom out and rebound. Its circulating market value has rebounded from the lowest point of US$400 million in September to the current US$1 billion.

In the article The continuous decline of altcoins may be the best time to deploy DeFi published by the author in early July, Ethena was also mentioned. The view at that time was:

“…Ethena’s business model (a public fund focusing on perpetual contract arbitrage) still has an obvious ceiling. The large-scale expansion of its stablecoin (the scale reached 3.6 billion US dollars at the time) is based on the premise that secondary market users are willing to take over its token ENA at a high price and provide high income subsidies to USDE. This slightly Ponzi-like design can easily lead to a negative spiral of business and coin prices when market sentiment is bad. The key point of Ethena’s business turning point is that USDE can one day truly become a stablecoin with a large number of “natural coin holders”. At this point, its business model has also completed the transformation from a public arbitrage fund to a stablecoin operator.”

Since then, the price of ENA has continued to fall by 60%. Even though the price has nearly doubled from its low point, it is still 30%+ away from the price at that time.

The author re-evaluates Ethena at this time and will focus on the following three issues:

1. Current business level: Ethena’s current core business indicators, including scale, revenue, comprehensive costs and actual profit level

2. Future business outlook: Ethena’s promising narrative and future development

3. Valuation Level: Is ENAs current price in the undervalued strike zone?

This article is the authors interim thinking as of the time of publication. It may change in the future, and the views are highly subjective. There may also be errors in facts, data, and reasoning logic. Criticism and further discussion from colleagues and readers are welcome, but this article does not constitute any investment advice.

The following is the main text.

1. Business level: Ethena’s current core business situation

1.1 Ethena’s business model

Ethena positions its business as a synthetic dollar project with native returns, that is to say, its track is the same as MakerDAO (now SKY), Frax, crvUSD (Curves stablecoin), and GHO (Aaves stablecoin) - stablecoin.

In my opinion, the business models of the current stablecoin projects in the cryptocurrency world are basically similar:

1. Raising funds, issuing debt (stablecoins), and expanding the project’s balance sheet

2. Use the raised funds to conduct financial operations and obtain financial benefits

When the income from project operating funds is higher than the combined cost of raising funds and running the project, the project is profitable.

Take Tether, the issuer of the centralized stablecoin project USDT, for example. Tether raises US dollars from users, issues debt (USDT) certificates to users, and then uses the raised funds to invest in interest-bearing assets such as government bonds and commercial paper to obtain financial returns. Considering the wide range of uses of USDT, its value is no different from that of the US dollar in the minds of users, but it can do many things that traditional US dollars cannot do (such as instant cross-border transfers), so users are willing to provide US dollars to Tether for free in exchange for USDT, and when you want to redeem USDT from Tether, you also need to pay a certain redemption fee.

As a latecomer stablecoin project, Ethena is obviously at a disadvantage compared to old projects such as USDT and DAI in terms of network effects and brand credit. This is reflected in its higher fundraising costs, because only when users have higher return expectations are they willing to provide their assets to Ethena in exchange for USDE. Ethenas approach is to raise funds by providing users with incentives for project tokens ENA and stablecoins (financial income from project operating funds).

1.2 Ethenas core business data

1.2.1 USDE issuance scale and distribution

Data source: https://app.ethena.fi/dashboards/solvency

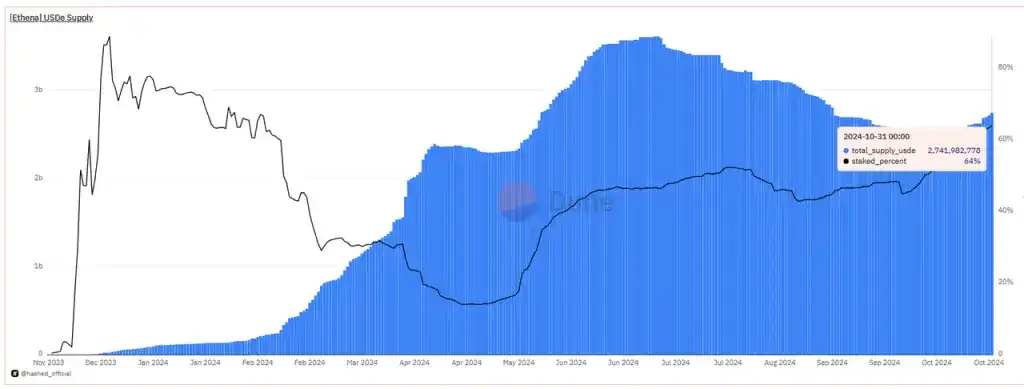

After the issuance scale of USDE hit a new high of 3.61 billion in early July 2024, its scale continued to decline to 2.41 billion in mid-October, and is now gradually recovering, reaching approximately 2.72 billion as of October 31.

Of the more than 2.72 billion USD, 64% of the USDE is pledged, and the current corresponding APY is 13% (official website data).

Data source: https://dune.com/queries/3456058/5807898

It can be seen that the purpose of most users holding USDE is to obtain financial management income. 13% is the risk-free return of the USDE standard, and it is also the current financial cost of Ethena to raise user funds.

During the same period, the yield on short-term U.S. Treasury bonds was 4.25% (data as of October 24), the deposit rate of USDT on Aave, the largest Defi lending platform, was 3.9%, and that of USDC was 4.64%.

We can see that in order to expand its fundraising scale, Ethena still maintains a relatively high fundraising cost.

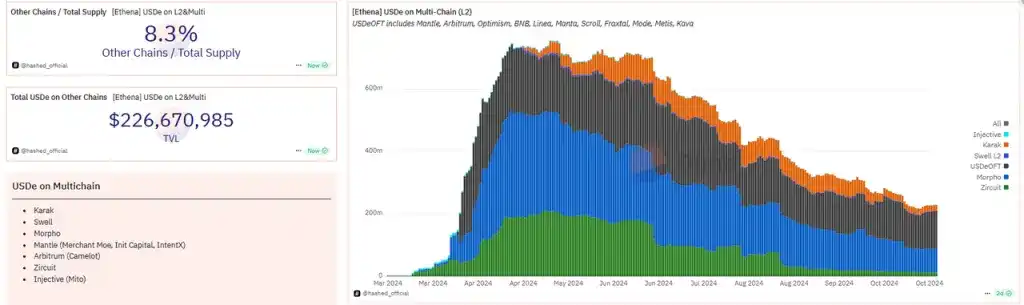

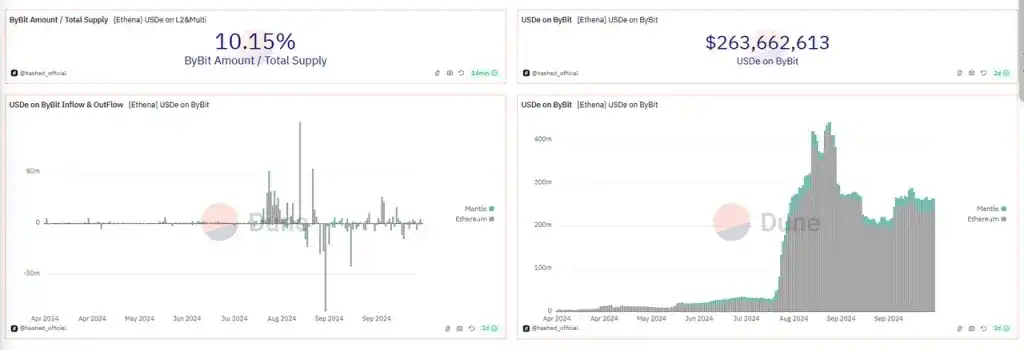

USDE is not only issued on the Ethereum mainnet, but also expanded on multiple L2 and L1 chains. Currently, the scale of USDE issued on other chains is 226 million, accounting for about 8.3% of the total.

Data source: https://dune.com/hashed_official/ethena

In addition, as an investor and important cooperation platform of Ethena, Bybit not only supports USDE as margin for derivatives trading, but also provides a yield of up to 20% for USDE deposited in Bybit (reduced to a maximum of 10% in September). Therefore, Bybit is also one of the largest custodians of USDE, currently with 263 million USDE (more than 400 million at peak times).

Data source: https://dune.com/hashed_official/ethena

1.2.2 Protocol Income and Underlying Asset Distribution

Ethena currently has three sources of protocol revenue:

1. Income from ETH pledged in the underlying assets;

2. Funding rates and basis income from derivatives hedging and arbitrage;

3. Financial returns: Hold in the form of stablecoins to obtain deposit interest or incentive subsidies, such as placing USDC in Coinbase to obtain rewards from the loyalty program (Coinbase’s cash subsidy for USDC, approximately 4.5% annualized); and sUSDS (formerly sDAI) in Spark, etc.

According to data from Token Terminal that has been officially approved by Ethena, Ethenas revenue in the past month has come out of the low point of last month. The agreement revenue in October was 10.63 million US dollars, a month-on-month increase of 84.5%.

Data source: Tokenterminal, Ethena protocol revenue and revenue allocated to USDE (cost of revenue)

Of the current protocol revenue, part of it is distributed to USDE pledgers, and part of it will go into the protocols reserve fund to deal with expenditures when the funding rate is negative and various risk events.

In the official document, it is stated that the amount of protocol revenue used for the reserve fund must be determined by governance. However, the author did not find any specific proposals on the reserve fund allocation ratio in the official forum, and the specific ratio changes were only announced in the official blog at the beginning. The actual situation is that the distribution ratio and distribution logic of the Ethena protocol revenue have been adjusted many times after the launch. During the adjustment process, the official will initially listen to the opinions of the community, but the specific distribution plan is still determined by the official subjectively and has not gone through a formal governance process.

It can also be seen from the data of the Token terminal in the above figure that the distribution ratio of Ethenas income between USDE pledger income (the red column in the above figure, i.e. cost of revenue) and reserves changes dramatically.

When the protocol revenue was high in the early stage of the project launch, most of the protocol revenue was allocated to the reserve fund, of which 86.7% of the protocol revenue in the week of March 11 was allocated to the reserve fund account. After entering April, as the price of ENA began to fall rapidly, the income from the ENA token side was insufficient to stimulate the demand for USDE. In order to stabilize the scale of USDE, the distribution of Ethena protocol revenue began to tilt towards USDE pledgers, and most of the revenue was allocated to USDE pledge users. It was not until the last two weeks that Ethenas weekly protocol revenue began to be significantly higher than the expenditure allocated to USDE pledge users (ENA token incentives are not considered here).

Ethenas underlying assets, data source: https://app.ethena.fi/dashboards/transparency

From the current underlying assets of Ethena, 52% are BTC arbitrage positions, 21% are ETH arbitrage positions, 11% are ETH pledged asset arbitrage positions, and the remaining 16% are stablecoins. Therefore, Ethena’s current main source of income is BTC-based arbitrage positions. The ETH Staking income, which was once the focus, has a small contribution rate to income due to its small proportion of assets.

BTC and ETH perpetual contract arbitrage quarterly average yield, data source: https://app.ethena.fi/dashboards/hedging

Judging from the average yield trend of BTC perpetual contract arbitrage, the average yield so far in the fourth quarter has escaped from the low range of the third quarter and returned to the position of the second quarter of this year. The average annualized yield so far this quarter is 8% +, but even in the third quarter when the market was sluggish, the overall average annualized yield of BTC arbitrage was above 5%.

The overall annualized yield of ETHs perpetual contract arbitrage is similar to that of BTC, and has now returned to 8%+.

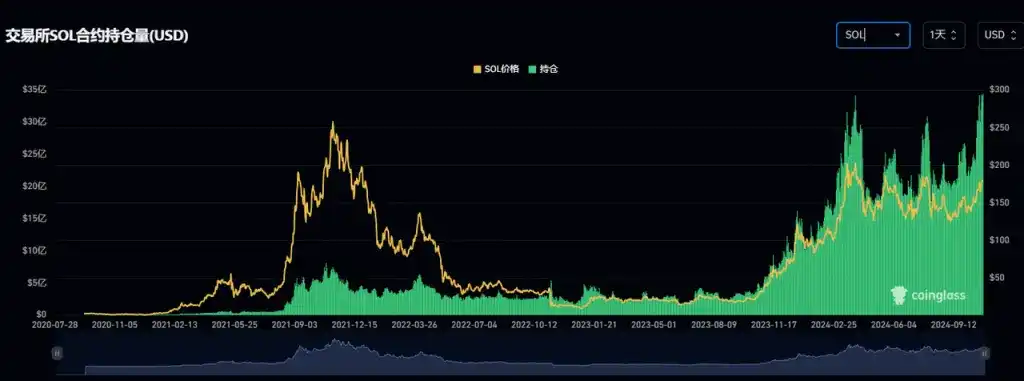

Let’s take a look at the market contract size of Sol, which will soon be included in the underlying assets of Ethena. Even though the contract holdings of Sol have increased significantly this year as the price of Sol has risen, and it has now reached 3.4 billion US dollars, it is still far from ETH’s 14 billion US dollars and BTC’s 43 billion US dollars (both excluding CME data).

SOL contract open interest trend, data source: Coinglass

As for Sol’s funding fee, judging from Binance and Bybit, which have the largest holdings, its annualized funding rate in recent days is similar to that of BTC and ETH. Its current annualized funding rate is around 11%.

The current annualized funding rate data source for mainstream currencies: https://www.coinglass.com/zh/FundingRate

In other words, even if Sol is included in Ethenas contract arbitrage targets in the future, its current scale and yield have no obvious advantages over BTC and ETH, and it cannot bring much incremental income in the short term.

1.2.3 Ethena’s protocol expenses and profit levels

Ethenas protocol expenses are divided into two categories:

1. Financial expenses are paid through USDE to USDE pledgers, and the source of income is Ethenas protocol income (derivatives arbitrage and ETH staking, as well as stablecoin financial management).

2. Marketing expenses are paid with ENA tokens. The payment targets users who participate in Ethena’s various growth activities (Campaigns). These users earn points by participating in the activities (different stages of the Campaign have different points names, such as Shards in the early stage and Sats later), and after each quarter’s activities, they can exchange their points for corresponding ENA token rewards.

Financial expenses are relatively easy to understand. For users who pledge USDE, they have clear income expectations. The official website clearly marks the current USDE yield rate:

The current yield on USDE staking is 13%. Source: https://ethena.fi/

What is more complicated is that Ethena has been carrying out various marketing campaigns since the project was launched. They have different rules, and use points to incentivize specific user behaviors. A weighting mechanism has also been introduced, involving the comprehensive calculation of activities on multiple cooperative platforms.

Let’s take a brief look at the series of growth activities after Ethena went online:

1.Ethena Shard Campaign: Epoch 1-2 (Season 1)

Time: 2024.2.19-4.1 (less than one and a half months)

Main incentive behavior: Provide stablecoin liquidity for USDE on Curve.

Secondary incentive behaviors: minting USDE, holding sUSDE, depositing USDE and sUSDE in Pendle, and holding USDE on various cooperative L2s.

Growth in size: During this period, the size of the USDE grew from less than 300 million to 1.3 billion.

The amount of ENA spent, that is, the marketing expenses of the event: a total of 750 million, accounting for 5%. Among them, the top 2,000 wallets can receive 50% of the ENA immediately, and the remaining 50% will be distributed linearly in the remaining 6 months. There is no unlocking restriction for the remaining small wallets. According to the Dune dashboard data created by @sankin, nearly 500 million ENA has been received in June. Before June, the highest price of ENA was about 1.5 $, the lowest was about 0.67 $, and the average price was about 1 $; after the beginning of June, ENA began to fall rapidly from 1 $, falling to a minimum of about 0.2 $, with an average price of 0.6 $, and the remaining 250 million ENA was basically received during this period.

We can make a very rough estimate that the corresponding value of 750 million ENA = 5* 1+ 2.5* 0.6, which is about 650 million US dollars.

That is to say, the size of USDE increased by about 1 billion US dollars in less than 2 months, and the corresponding marketing expenses were as high as 650 million US dollars, which does not include the financial expenses paid for USDE.

Of course, as the first airdrop of ENA, the huge marketing expenditure at this stage is special.

2.Ethena Sats Campaign: Season 2

Time: 2024.4.2-9.2 (5 months)

Main incentive behaviors: lock ENA, provide liquidity for USDE, use USDE as collateral for lending, deposit USDE in Pendle, deposit USDE in the Restaking protocol, and deposit USDE in Bybit.

Secondary incentive behaviors: lock USDE on the official platform, hold and use USDE on cooperative L2, use sUSDE as collateral for loans, etc.

Growth in size: During this period, the size of the USDE grew from 1.3 billion to 2.8 billion

The amount of ENA spent, i.e. the marketing expenses of the activity: As in the first season, the rewards for the second season are also 5% of the total amount, i.e. 750 million ENA (among which the 2,000 wallets that received the largest amount of airdrops also face 50% of the TGE and subsequent unlocking for up to 6 months). Based on the current price of ENA of $0.35, the corresponding value of 750 million ENA is approximately $260 million.

3. Ethena Sats Campaign: Season n3

Time: September 2, 2024 to March 23, 2025 (less than 7 months)

Main incentive behaviors: lock ENA, hold USDE in officially designated cooperation agreements (mainly DEX and lending), and deposit USDE in Pendle

Scale growth: As of now, despite the plans for the third quarter, the scale growth of USDE has encountered a bottleneck. The current scale of USDE is about 2.7 billion, which is slightly lower than the 2.8 billion at the beginning of the third quarter.

Amount of ENA spent: However, considering that the third season is nearly 7 months, which is longer than the second season, and the ENA reward incentive is likely to continue to decline, the total ENA incentive amount in the third season will remain at 5% of the total, which is 750 million.

At this point, we can roughly calculate the total protocol expenditure of the Ethena protocol since its launch this year (October 31):

Financial expenditure (paid to USDE pledgers in the form of stablecoins): $81.647 million

Marketing expenses (paid to users participating in the event in the form of ENA tokens): 6.5 + 2.6 = 910 million US dollars (potential expenses after September are not calculated here)

Ethenas quarterly protocol revenue and financial expenditure trends, source: tokenterminal

Total contract revenue for the same period: $124 million

In other words, contrary to everyone’s impression that “Ethena is very profitable”, in fact, after deducting financial and marketing expenses, Ethena’s net loss has reached 868 million US dollars by the end of October this year. The author has not yet considered the ENA token expenditure from September to October, so the actual loss amount may be higher than this figure.

A net loss of 868 million is the price USDE paid for increasing its market value to 2.7 billion U.S. dollars in one year.

In fact, like many DeFi projects in the previous round, Ethena uses token subsidies to increase core business indicators and protocol revenue. However, Ethena uses a unique points system in this round, delays the issuance of tokens, and includes more partners as participation channels, which makes it difficult for participating users to intuitively evaluate the final financial returns of their participation in Ethena activities, which in a sense improves user stickiness.

2. Future business outlook: Ethena’s promising narrative and future development

In the past two months, ENA has achieved a rebound of nearly 100% from its low point, and this was even before ENA opened the rewards for Season 2 in early October. These two months were also two months of intensive Ethena news and positive news, such as:

October 28: On-chain options and perpetual contracts project Derive (formerly Lyra) includes sUSDE as collateral

October 25: USDE is included as collateral for OTC transactions by Wintermute

October 17: Ethena launches proposal to integrate Ethena liquidity and hedging engine into Hyperliquid

October 14: Ethena community initiated a proposal to include SOL in the underlying assets of USDE

September 30: The first project of the Ethena ecological network debuted, the derivatives exchange Ethereal, and promised to airdrop 15% of the tokens to ENA users. After that, Ethena Network announced that it would release more information about the product launch schedule and new ecosystem applications developed based on USDE in the next few weeks.

September 26: Plans to launch USTB - the so-called new stablecoin launched in cooperation with BlackRock. In fact, USTB is a stablecoin with BUILD, an on-chain treasury bond token issued by BlackRock, as its underlying asset, and has limited direct relationship with BlackRock.

September 4: Cooperated with Etherfi and Eigenlayer to launch the first stablecoin AVS collateral asset - eUSD. You can get it by depositing USDE in etherfi. eUSD will be launched on September 25.

It can be said that in the past two months, the scenarios of USDE and sUSDE have increased a lot, although the demand stimulation for USDE may not be obvious. For example, the stablecoin AVS collateral asset eUSD launched in cooperation with Etherfi and Eigenlayer currently has a scale of only a few million.

In fact, what really drove this round of ENA price takeoff was the article published on October 12 by the well-known trader and crypto KOL Eugene @0x ENAS, which strongly called for Ethena: Ethena: The Trillion Dollar Crypto Opportunity .

After the publication of this article, which was forwarded nearly 400 times, liked more than 1,800 times, and viewed more than 700,000 times, the price of ENA rose from $0.27 to $0.41 in 4 days, an increase of more than 50%.

In addition to reviewing some of Ethenas product features in the article, Eugene mainly emphasized three reasons. However, in my opinion, except for the first reason, the remaining two reasons are full of complaints:

1. The US interest rate cut has led to a decline in global risk-free interest rates, making the USDE APY more attractive and attracting more capital inflows.

2. Cooperation with BlackRock The newly launched USTB stablecoin is an absolute gamechanger that will greatly increase the adoption of USDE, because when the perpetual arbitrage yield in the market is negative, USDE can switch the underlying assets to USTB and obtain the risk-free return of government bonds.

Complaints: USTB uses BUILD as the underlying asset, which does not mean that USTB is a stablecoin jointly launched by BlackRock and Ethena, just like Dais underlying assets have a large amount of USDC, but Dai is not a stablecoin jointly launched by Circle and MakerDAO. In fact, if USDE wants to obtain treasury bond returns during the period of negative perpetual returns, it can directly close the position and configure Build or sDAI, or change it to USDC and store it in Coinbase to receive a 4.5% annual subsidy, without having to issue another USTB to hold. USTB is more like a gimmick product that takes advantage of BlackRocks traffic. Calling such a useless product an absolute gamechanger can only make people doubt the authors cognitive level or writing motivation.

3. In the future, the emission rate of ENA will decrease, and the selling pressure will decrease rapidly compared with the previous one.

Complaints: The actual rewards for Season 2 still account for 5% of the total amount of ENA, that is, 750 million token incentives will enter circulation in the next 6 months, which is not much less than the total amount of incentives in the previous season. Moreover, in March next year, ENA will usher in a huge amount of unlocking by the team and investors, and the inflation expectations of ENA in the next six months are not optimistic.

However, there are still stories worth looking forward to about Ethena in the next few months to a year.

First, with the rising expectations of Trump’s inauguration and the Republican victory (the results will be seen in a few days), the warming of the crypto market will be conducive to the increase in the perpetual arbitrage yield and scale of BTC and ETH, and increase Ethena’s protocol revenue;

Second, more projects will emerge after Ethereal within the Ethena ecosystem, increasing ENA’s airdrop revenue;

Third, the launch of Ethena’s own public chain can also bring attention and nominal scenarios such as staking to ENA, but the author expects that this will be launched only after more projects have accumulated in the second line.

However, the most important thing for Ethena is that USDE can be accepted as a collateral and trading asset by more leading CEXs.

Among the leading exchanges, Bybit has reached in-depth cooperation with Ethena.

Coinbase has its own USDC to operate, and as a US-based company, considering the complexity of regulation, the possibility of it supporting USDE as collateral and stablecoin trading pairs is basically zero.

Among the two major CEXs, Binance and OKX, there is a possibility that OKX will include USDE in stablecoin trading pairs and contract collateral because it participated in two rounds of Ethena financing and has a certain consistency in financial interests. However, this possibility is not great because this move will also bring OKX operating and endorsement risks related to Ethena. Compared with OKX, Binance, which only participated in one round of Ethena investment, is less likely to include USDE in stablecoin trading pairs and collateral, and Binance itself also has its own supported stablecoin projects.

Eugene believes that USDE will become the contract margin asset of major exchanges, which is one of the reasons why he is optimistic about Ethena in his previous article, but the author is not optimistic about this.

3. Valuation Level: Is ENAs current price in the undervalued strike zone?

We analyze ENAs current valuation from two dimensions: qualitative analysis and quantitative comparison.

3.1 Qualitative analysis

Events that are likely to be favorable to the price of ENA tokens in the coming months include:

The recovery of the crypto market has led to an increase in arbitrage profits, which is reflected in the improvement of the protocols revenue expectations, causing the price of ENA to rise and promoting the growth of the USDE scale.

Incorporating SOL into the underlying assets can attract the attention of SOL ecosystem investors and project owners

The Ethena ecosystem may see more Ethereal-like projects in the coming months, bringing more airdrops to ENA

Before the next wave of ENA unlocking, the project has the motivation to push up the price of the coin. First, it promotes the upward spiral of business and coin price, and second, it provides itself with a higher shipping price.

In addition, judging from Ethenas performance in more than half a year since its launch, the Ethena project team has very strong business capabilities. It can be said that it is the best among many stablecoin projects in terms of external cooperation expansion, and is more aggressive and efficient than the leading stablecoin project MakerDAO.

The factors that are currently unfavorable to the value of ENA tokens and suppressing ENA prices include:

ENA lacks real money profit distribution, and is more of a floating pledge scenario (such as using AVS assets to ensure Ethenas multi-chain security) and self-mining.

The actual profitability of the Ethena project is not good. The huge subsidies implemented to open up the market have caused the project to suffer serious net losses. This part of the loss is actually borne by ENA token holders.

ENA will still face great inflationary pressure in the next six months. On the one hand, it comes from the expenditure of ENA tokens in marketing activities, and on the other hand, it will face the unlocking of the core team and investors after one year in late March next year. According to tokenomist data, ENA tokens will face inflationary pressure of 85.4% of the current circulation in the next 6 months.

Data source: https://tokenomist.ai/

3.2 Quantitative comparison

Ethenas business model is actually no different from other stablecoin projects. Its innovation lies in the use of raised assets, that is, using the raised assets to make profits through perpetual contract arbitrage.

Therefore, we will use MakerDAO (now SKY), the stablecoin project with the largest current market value, as a valuation benchmark for comparison.

It can be seen that compared with the old protocol MakerDAO, the current price of Ethenas token ENA is not cost-effective in terms of protocol revenue or profit.

Summarize

Although many people call Ethena a highly representative innovative project in this round, its core business model is no different from other stablecoin projects. They all aim to raise funds for financial operations and make profits, and strive to promote the use scenarios and acceptance of their own bonds (stablecoins) to minimize their own fundraising costs.

At the current stage, Ethena, which is in the early stage of stablecoin promotion, is still in a stage of huge losses and is not a very profitable project as many KOLs say. Its valuation is not underestimated compared with the representative stablecoin project MakerDAO.

However, as a new player in this field, Ethena has shown a very strong business development capability and is more aggressive than other projects. Like many Defi projects in the previous cycle, rapid scale expansion and more project adoption will increase investors’ and researchers’ optimistic expectations for the project, thereby pushing up the price of the currency. The rising price of the currency will bring higher APY, further pushing up the scale of USDE, forming an upward spiral with the left foot stepping on the right foot.

Then, such projects will eventually face a critical point, where people begin to realize that the growth of the project is driven by token subsidies, while the price increase of the newly issued tokens seems to be supported only by optimistic sentiment and lacks a value hook.

At this point, a game of running fast begins.

In the end, only a few projects can be reborn from such a downward spiral. The last round of stablecoin star Luna (UST issuer) has been buried, Fraxs business has shrunk significantly, and Fei has ceased operations.

As a stablecoin product with an obvious Lindy effect (the longer it exists, the stronger its vitality), Ethena and its USDE still need more time to verify the stability of its product architecture and its ability to survive after the subsidy reduction.

References and data sources

Asset price: https://www.coingecko.com/

Token unlocking information: https://tokenomist.ai/

Financial data: https://tokenterminal.com/

Project data dashboard: https://app.ethena.fi/dashboards/transparency

Official announcement: https://mirror.xyz/0xF99d0E4E3435cc9C9868D1C6274DfaB3e2721341

KOL Eugene’s milk article: https://x.com/0x ENAS/status/1844756962854212024