Original article from The Defi Report

Compiled by Odaily Planet Daily Golem ( @web3_golem )

Editor’s note: “That season seems to be coming.” Previously, people on social media were afraid to call the altcoin season directly because they had experienced too many disappointments. But on May 8, after a lapse of 3 months, when BTC once again reached $100,000, mainstream altcoins also rose collectively, with ETH performing the best. The topic of “40% surge in 3 days, what happened to Ethereum” even topped the Douyin hot list . Nick Tomaino, the founder of 1coinfirmation, even boasted that ETH would eventually surpass BTC .

But the price increase does not mean that the fundamentals of ETH have changed significantly. There are still doubts about Ethereum and discussions about whether its biggest competitor Solana will surpass it. In January 2023, SOLs trading price was 97% lower than ETH. Today, SOLs price is still more than 90% lower than ETH, and ETHs market value is still more than three times that of SOL. Is it really possible for SOL to surpass ETH?

Researchers at The DeFi Report believe that from a fundamental perspective, even if it cannot surpass ETH, the price of SOL should definitely not be lower than 90% of ETH. In the past, the analysis mainly used fees, DEX trading volume, stablecoin supply and trading volume, total TVL and other indicators to compare the two networks. The focus of this report of The DeFi Report turns to comparing the actual value available to ETH and SOL token holders. Statistics show that the actual value obtained by SOL token holders is 3.6 times that of ETH. Therefore, it is believed that the market currently values ETH higher than SOL. Odaily Planet Daily will compile the full text as follows, enjoy~

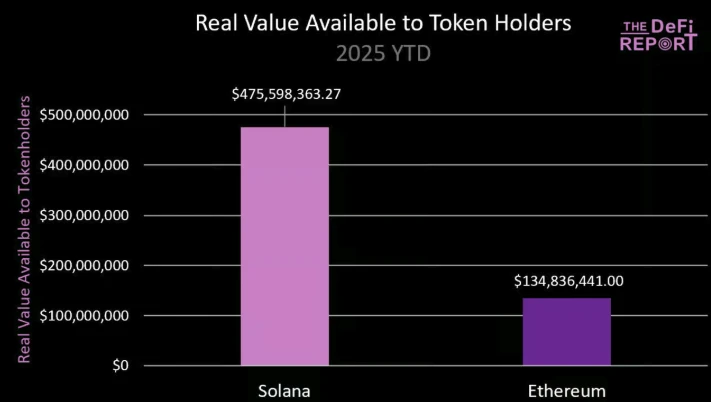

The actual value available to token holders

Solana

Real value available to Solana token holders/stakers = Jito Tips (MEV) earned by validators and shared with stakers. This does not include newly issued SOL, base fees, priority fees, or MEV earned by MEV hunters.

Solanas $475 million in the above chart is the net value after Jito charges a 6% fee to all validators running the Jito Tips router and block engine. If you hold SOL, you can stake to a trusted validator/LST, such as Helius (hSOL), which charges stakers $0 in commissions. In this case, SOL stakers can earn 94% of the MEV running through Jito (95% of Solanas stake runs on Jito).

Ethereum

The actual value available to Ethereum token holders/stakers = MEV + priority fees earned by validators and shared with stakers. It does not include new ETH issuance, base fees, block fees, and the share of MEV reserved by MEV hunters and block builders.

The $134 million Ethereum estimate in the above chart has already deducted the 10% fee charged by Lido (the most trusted liquidity staking provider on Ethereum).

Solana is a combination of Nasdaq and DTCC

Ethereum has 6.6x the TVL of Solana and 10x the stablecoin supply. However, in terms of actual value received by token holders year-to-date, Solana token holders have received 3.6x the actual value of Ethereum. Because the execution and velocity of the network determine actual value, validators and token holders can monetize TVL.

In traditional finance (TradFi), Nasdaq is responsible for execution and circulation speed, and DTCC (Depository Trust Clearing Corporation) is responsible for custody/settlement. Ethereum is becoming more and more like DTCC (custody + settlement/accounting of L2 transactions), Base and other L2 platforms are becoming more and more like Nasdaq (handling execution/speed). Solana is becoming more and more like a combination of the two.

Integrating Nasdaq + DTCC into one solution means that SOL holders can get 100% of the value generated by the execution/speed service, while ETH holders can only get about 10% of the value (from the L2 platform through burning ETH). Ethereum has these assets, but they are circulating on L2, and the current question is whether ETH token holders can eventually get this value - Solana does not have this problem yet.

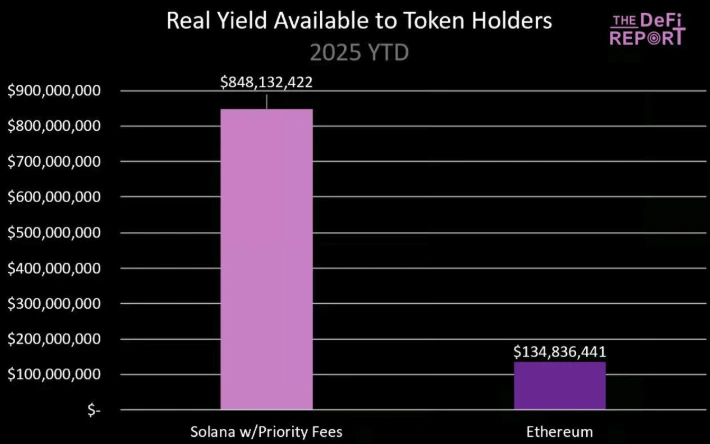

In addition to some innovative LST on the Sanctum platform, Solana validators are able to receive 100% of the priority transaction fees on user transactions (not shared with stakers). Jito wants to change this status quo, and the DAO currently has a governance proposal that will update the tip router to include priority fees in addition to the MEV that is currently routed and paid to stakers. According to Jito, the proposal is expected to be implemented in the next few months.

If you add in priority fees ($372 million after tip router fees), the year-to-date numbers are as follows:

It is not clear how strongly validators will choose to share priority fees, but we wanted to add this here so you can understand how your data may change in the future.

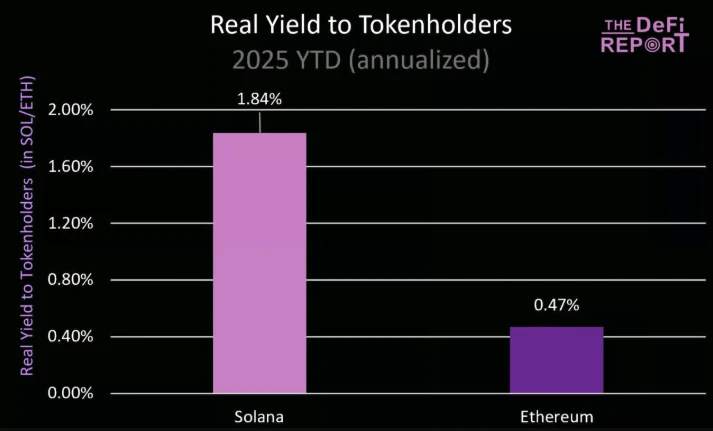

Actual rate of return

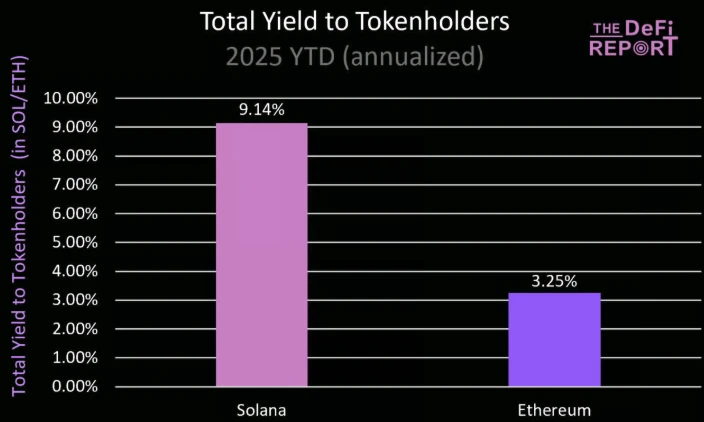

The following figure converts the above data into annualized actual yield (in SOL and ETH):

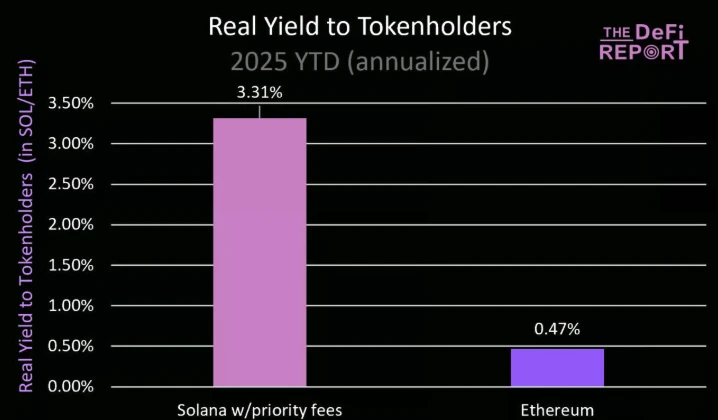

If Solana’s priority fees are included, Solana token holders receive an actual annualized return of 3.31%:

Total yield (including issuance/network inflation)

By staking their assets, token holders gain access to newly issued supply/issuance (used to incentivize validators/stakers to provide services). This is a key difference between crypto networks and traditional companies, as shareholders cannot avoid dilution.

Solana has an “issuance yield” of 7.3%, compared to Ethereum’s 2.78% based on actual network issuance as of May 6, 2025. Solana has issued 9.4 million tokens to date, which will be paid to the network’s SOL staked in validators (average stake of 385 million as of May 6, 2025). Ethereum has paid 329,380 ETH to the network’s 34.3 million tokens staked in validators.

Due to Ethereum’s extremely low network inflation (0.64% annualized based on actual year-to-date data), its “issuance yield” has normalized. Solana’s “issuance yield” will likely continue to decline as network inflation is currently 4.5% and decreases by 15% per year until it reaches a final level of 1.5%.

Actual value source

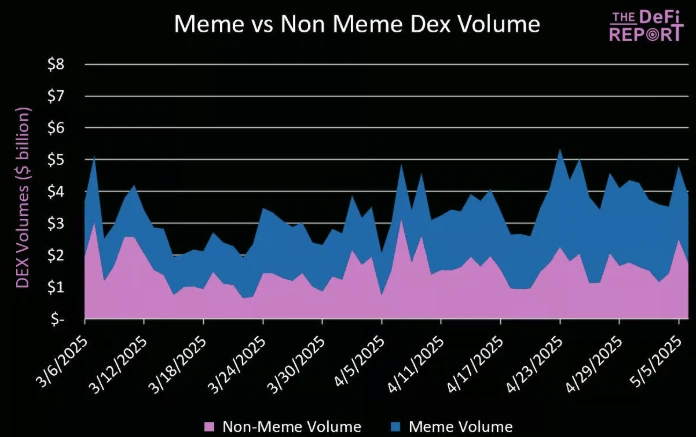

Meme coin has contributed more than half of Solana DEXs trading volume (up 51% in the past few months), SOL/USD accounts for about 35% of Solana DEXs trading volume, and the remaining 14% is stablecoins, LST and other assets.

Is this a problem for Solana? Yes and no.

Clearly, speculation is one of the strongest needs in crypto, and Solana has found product-market fit by providing a better user experience, which is not going away anytime soon. In addition, Meme coin transactions are also stress testing the system and providing valuable feedback to infrastructure providers.

Today it is Meme, maybe tomorrow it will be stocks, bonds, currencies and private assets, which may be Solanas goal. Currently, only 1-2% of the DEX transaction volume on the Ethereum mainnet is Meme coins, and stablecoin transactions account for about half. The transaction volume of ETH/stablecoins and other project tokens account for about 20% of the transaction volume.

But currently about 50% of the DEX transaction volume on Base comes from Meme, most of which are newly popular Memes.

MEV

Some crypto analysts believe that as base fees compress/commoditize, MEV (the value users pay for time-sensitive transactions) is the only sustainable long-term value in L1. We disagree, but we do believe that MEV will drive the majority of economics. Therefore, it is important to clarify the differences in how MEV works on Solana and Ethereum, and the impact this may have on L2.

Ethereum

Ethereum has a memory pool that all transactions go through before being sorted and submitted to validators. This is where MEV is obtained, and the main participants are:

Seekers (bots): These bots use machine learning algorithms to identify profitable opportunities in the mempool.

Block builders: Block builders are responsible for building blocks. In other words, they sort transactions into blocks and accept bribes from searchers in the process.

Validators: After block builders (with tips) submit blocks, validators approve them.

Workflow:

User submits transaction -> Ethereum memory pool -> Searchers (bots) identify value (arbitrage, sandwich attacks, liquidation) -> Submit replacement transaction to block builder (with tip) -> Block builder packages transaction -> Submit to validator (with tip) -> Validator approves transaction and keeps most of the tip (block builder and searcher keep a portion).

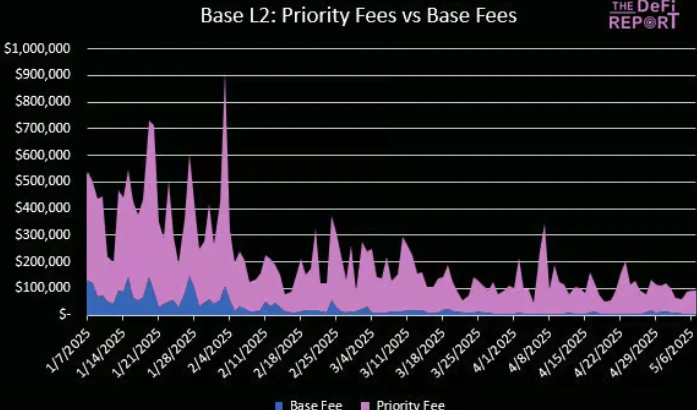

The biggest unknown facing Ethereum is what will happen to MEV if the majority of transactions move to L2 as expected?

We believe that MEV will transfer the priority fee to L2. The figure below shows that 85% of Base’s fees come from priority fees.

Solana

Solana does not have a mempool, but it has dedicated validator clients like Jito that implement some form of rolling, private mempool.

Working principle:

Jitos block engine creates a very brief (~200 milliseconds) window in which a seeker can submit a transaction package for inclusion in the next block. This rolling mempool is not public but is accessible to seekers connected to Jitos infrastructure, allowing them to discover and exploit potential arbitrage opportunities during this brief window.

Seekers monitor on-chain state (e.g., order books, liquidity pools) directly, typically by running their own full nodes or RPC endpoints. They detect arbitrage opportunities by observing state changes caused by confirmed transactions, rather than by looking at pending transactions in the memory pool.

When a profitable opportunity arises (such as a price imbalance between DEXs), bots quickly construct and submit their own trades (usually through Jito or a similar relayer) in the hope of seizing the opportunity before anyone else.

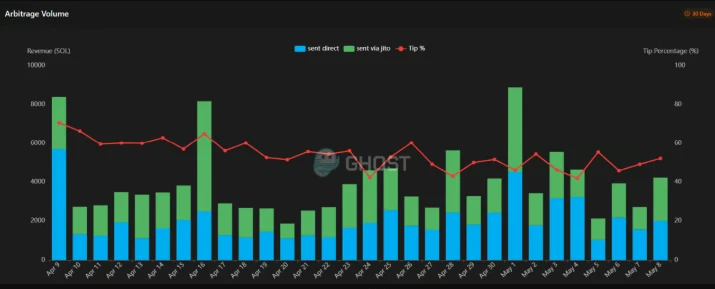

Currently, about 50% of arbitrage MEV on Solana is done through Jito (this value is shared with stakers via the tip router):

Data: sandwiched.me

If you invest in these networks, you need to understand how staking can accumulate MEV for you as a token holder. At the same time , SOL holders currently have a better chance of obtaining MEV (and possible priority fees) than ETH holders.

Summarize

Should SOL be trading 93% lower than ETH? From a fundamental point of view, absolutely not. Even considering ETHs superior network effects, decentralization, asset security, etc., the price difference is still too large.

Our conclusion is that the market currently values ETH higher than SOL based on ETH’s network effects and TVL.

The macro backdrop for ETH is that it will be home to trillions of tokenized assets like stocks, bonds, currencies/stablecoins, private assets, etc., and it may be so in the future. But ultimately, investors should focus on how ETH can extract real value from these assets.

Because investors have the option, if another chain can continue to bring more value to token holders, more capital will flow to that asset in the long run. As Benjamin Graham once said: In the short run, the market is a voting machine. But in the long run, it is a weighing machine.

ETH can try to change this situation through re-staking and blob fee adjustment. For example, MegaETH uses EigenLayer for data availability (DA), and ETH holders can capture additional real value from these networks through re-staking ETH.

But it must be clear that crypto assets rarely trade based on fundamentals today. Although we believe that prices will always return to value, this is not the case at present. Market narratives, trends, influence and liquidity conditions are still the factors that drive the market.

Of course, ETH has been at a disadvantage in the narrative over the past few years, but this situation is also improving after the recent price increase. For an asset worth more than $220 billion, a 20% increase in a single day is no small matter.

Remember: the crypto market is highly reflexive, price -> narrative -> fundamentals. Whether the recent turmoil in ETH is the beginning of a bigger trend, we will have to wait and see.