Original author: MaxWong@IOSG

TL;DR

Infrastructure is saturated; consumer applications are the next frontier. After years of pouring money into new L1s, roll-ups, and development tools, the marginal gains in technology are minimal, and users are not automatically flocking in just because the technology is “good enough.” Value is now created by attention, not architecture.

Liquidity is stagnant and retail investors are absent. The total market value of stablecoins is only about 25% higher than the historical high in 2021. The recent increase mainly comes from institutions purchasing BTC/ETH for their balance sheets, rather than speculative capital circulating within the ecosystem.

Core conclusion

Friendly regulatory policies will unlock the “second wave” of development. Clearer US policies (Trump administration, stablecoin bill) will expand TAM and attract Web2 users who only care about tangible applications rather than the underlying technical architecture.

Narrative markets reward real usage. Projects with significant revenue and PMF — like Hyperliquid (~$900M ARR), Pump.fun (~$500M ARR), Polymarket (~$12B in volume) — far outperform infrastructure projects with high funding but few users (Berachain, SEI, Story Protocol).

The essence of Web2 is the attention economy (distribution > technology); as Web3 and Web2 are deeply integrated, the market will also be like this - B2C applications will become a bigger pie.

Consumer tracks that have reached PMF (crypto-native):

Trading/Perpetual Contracts (Hyperliquid, Axiom)

Launchpad/Memecoin Factory (Pump.fun, BelieveApp)

InfoFi and prediction markets (Polymarket, Kaito)

The next wave of rising tracks (Web2 coding):

One-stop deposit/withdrawal + DeFi super app - wallet, bank, earnings, trading in one (Robinhood experience but without ads).

Entertainment/social platforms replace advertising with on-chain monetization (exchange, betting, prize pools, creator tokens), optimize UX and improve creator revenue.

AI and games are still in the pre-PMF stage. Consumer AI requires more secure account abstraction and infrastructure; Web3 games are plagued by the wool party economy. They will only break through after a blockchain game with gameplay as the core, rather than encryption elements, explodes.

Superchain theory. Activity is concentrating on a few consumer-friendly chains (Solana, Hyperliquid, Monad, MegaETH). Killer applications of these ecosystems and the infrastructure that directly supports them should be selected.

Investing in consumer applications perspective:

Distribution Execution > Pure Technology (network effects, viral loops, branding).

UX, speed, fluidity, and narrative fit determine the winner.

Evaluated as a “business” rather than a “protocol”: real revenue, scalable model, clear path to industry domination.

Bottom line: Pure infrastructure deals will have a hard time replicating 2021-style valuation doublings. Excess returns over the next 5 years will come from consumer applications that transform crypto assets into everyday experiences for millions of Web2 users.

introduction

In the past, the industry has paid great attention to technology/infrastructure, focusing on building tracks - new Layer-1, expansion layers, developer tools, and security primitives. The driving force is the industry creed of technology is king: as long as the technology is good enough and innovative enough, users will come naturally. However, this is not the case. Look at projects such as Berachain, SEI, Story Protocol, etc., which have outrageous financing valuations but are touted as the next big thing.

In this cycle, as consumer application projects have come into the spotlight, the discussion has clearly turned to what are these tracks used for. When the core infrastructure reaches a sufficient maturity and marginal improvements tend to decrease, talent and capital begin to pursue consumer-oriented applications/products - social, games, creators, business scenarios - to show the value of blockchain to retail and everyday users. The consumer application market is essentially an attention economy, which also makes the entire crypto market a battlefield for narrative and attention.

This insights report will explore:

1. Overall market background

2. Types of consumer applications in the market

a. Tracks with PMF

b. Tracks that can be upgraded with the help of encrypted tracks and eventually reach PMF

3. Propose a framework and investment thesis for consumer applications - How can institutions identify winners?

Narrative – Why now?

This cycle lacks the 2021 level of retail FOMO and NFT/Alt hype. In addition, the tightening macro environment has restricted the capital investment of VCs and institutions, and the growth of new liquidity has fallen into a stagflation situation.

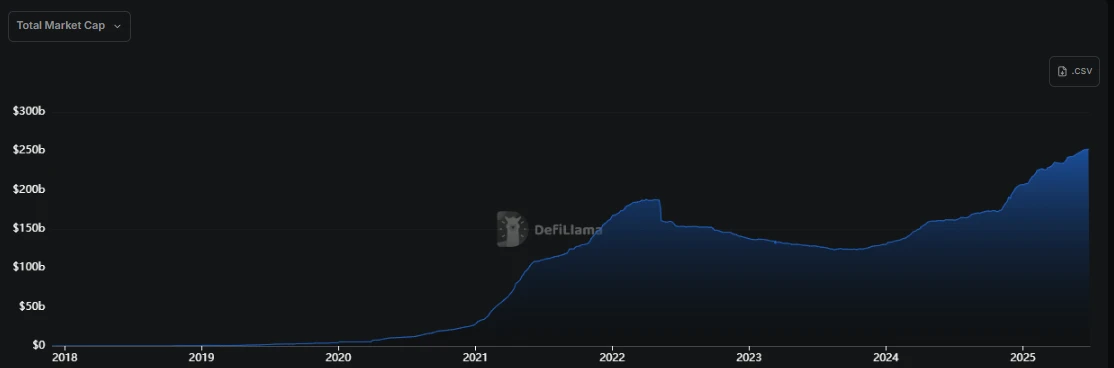

▲ Stablecoin market value trend chart

As shown in the above chart, the total market value of stablecoins increased by about 5 times from 2021 to 2022, while this round (second half of 2023-2025) only increased by 2 times. At first glance, it seems to be an organic and healthy steady growth, but it is actually misleading: the current market value is only ~25% higher than the 2021 high, which is a low speed for any industry in a 4-year dimension. This is still in the context of the most clear regulatory tailwind for stablecoins and the emergence of a strong president who supports the currency.

The growth rate of capital inflows has slowed significantly, and it mainly started after Trumps election in January 2025. So far, new capital is not speculative or real live water, but more due to institutions adding BTC/ETH to their balance sheets and governments and companies expanding stablecoin payments. Liquidity is not due to market interest in new products/solutions, but regulatory benefits; these funds are non-speculative and will not be directly injected into the secondary market. This is not free capital, nor is it driven by retail investors, so even with the high prices, the industry has not yet reproduced the 2021 frenzy.

The overall analogy is that after the .com bubble in 2001, the market was looking for the next growth direction - this time the direction will be consumer applications. Past growth was also driven by consumer applications, but the products were NFTs and altcoins, not applications.

Core conclusion

In the next five years, the crypto market will usher in a second wave of growth driven by Web2/retail investors

Trump administration’s clearer crypto policy gives green light to founders

Stablecoin legislation significantly expands the TAM of all crypto applications

In the past, the bottleneck of liquidity was the lack of a clear framework and the obvious market island effect; now the clear regulations on stablecoins are beneficial to liquidity

Strong positive sentiment at the political level has a greater impact on consumer applications than infrastructure, because consumer applications attract a large number of Web2 users.

Web2 users only care about the application layer that they can interact directly with and the products that can bring value to themselves - they want the Robinhood of Web3, not the crypto AWS

Robinhood

Google/YouTube

Facebook

Instagram

Snapchat

ChatGPT

Market maturity → Focus on real users + revenue + PMF > Infrastructure + Technology

In the narrative market, capital continues to flow to projects with real revenue and real PMF, and most of them are consumer applications because they have real users.

Hyperliquid

Pump.fun

Polymarket

Significance: Technology is important, but good technology alone will not attract users; good technology must be implemented → The easiest path is consumer application

Method: Projects with unified extreme UX + value capture mechanism will attract users. Users don’t care whether the technology is slightly better unless they can “feel” it.

Builders are shifting from technology is king to user first in 2019-2023. Chains with actual demand, rather than just subsidized ecosystems or tool availability, will attract developers.

In the past, the market made developers write extensions for Firefox for subsidies instead of acquiring real users on Chrome.

Typical counterexample: Cardano

Web2 has always been an attention economy (distribution > technology); this will also be the case after Web3 and Web2 are deeply integrated - B2C applications will expand the overall market

Virality and attention are the keys to success → Consumer apps are easiest to implement

Because network effects are easy to embed in consumer applications → e.g. integrating with Twitter and receiving protocol rewards for posting (Loudio, Kaito)

Therefore, consumer application content is easy to generate → easy to spread virally and occupy the mind

B2C apps can also easily create buzz through user behavior, incentives, or communities (Pump.fun vs Hyperliquid)

Virality brings attention, attention brings users → viral apps will attract new retail investors and expand the market

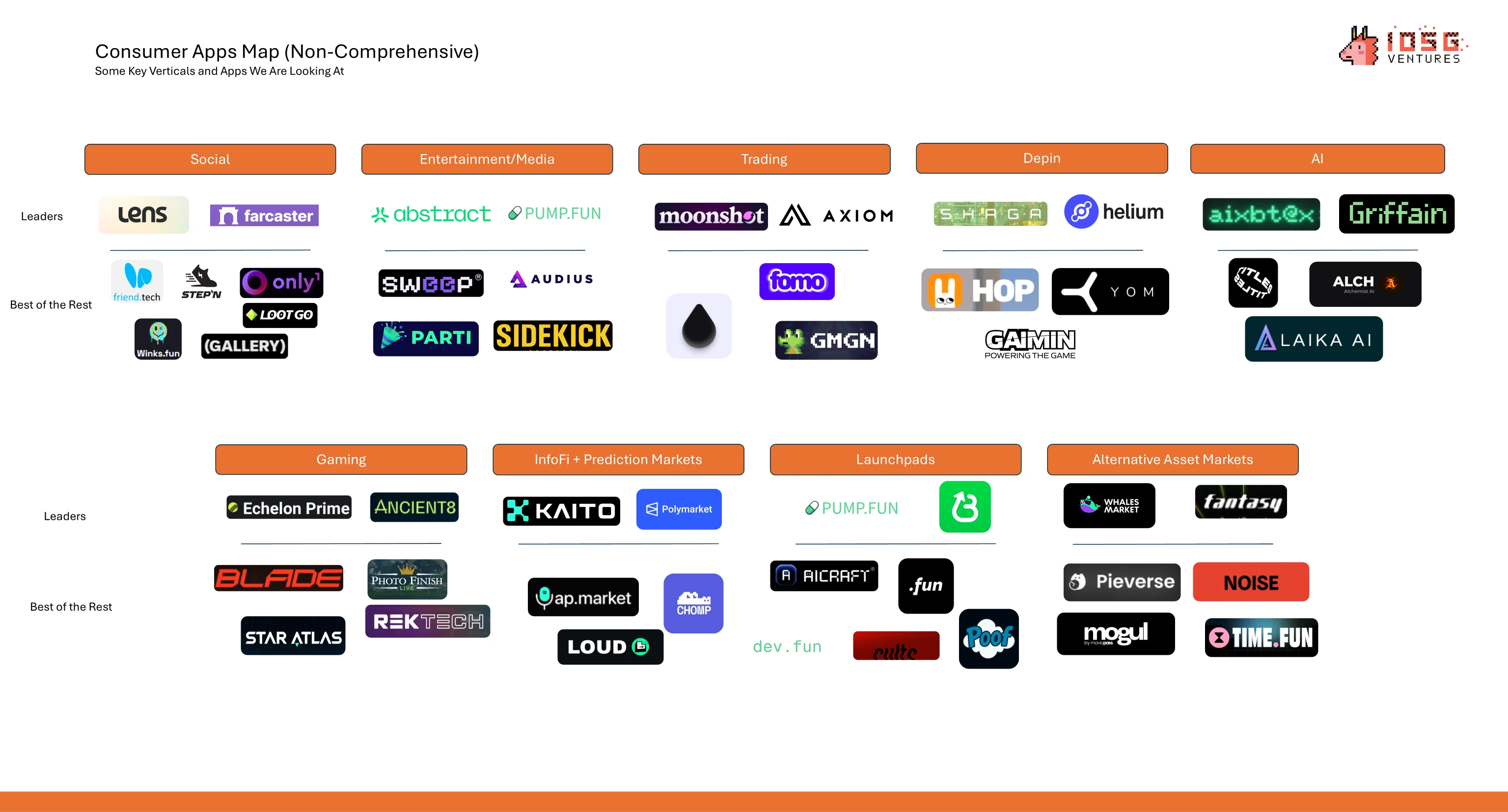

Types of consumer applications in the market

The vertical track of PMF has been reached – Crypto Coded

trade

Hyperliquid: ~$900 million ARR; $0

Axiom: ~$120 million ARR; $21 million raised

Launchpad

Pump.fun: ~$500 million ARR; $0

BelieveApp: Annualized costs of approximately $60 million; financing of $0

InfoFi + Prediction Market

Polymarket: Annual volume of approximately $12 billion (0% fee); financing of $0

Kaito: ~$33 million ARR; $10.8 million raised

Such track projects should be given special attention.

contrast:

Berachain: Only $165,000 in fees since launch; $142 million in funding; +85% drop from ATH

SEI: Annualized cost is only $68,000; raised $95 million; drop of 75%+

Story Protocol: Only $24,000 in fees since launch; $134 million in funding; 60% drop

Pure technology/infrastructure without real use cases is no longer a solution. Institutions can no longer rely on such targets to replicate 2021-style excess returns.

From these platforms, we can see that most of them are more Web3 native, which is in line with their encryption function positioning. However, there are also traditional consumer tracks (see below) that have been subverted by the encryption track and are moving towards the public.

The vertical track that can be upgraded through encryption technology and eventually reach PMF - Web2 Coded

Web2⇄Web3 deposit/withdrawal + DeFi front-end

As Web2 users continue to flock to Web3, it’s time for one or two mainstream solutions to emerge that everyone can use to deposit/withdraw and access DeFi. The market is currently highly fragmented and the user flow is clunky.

The pain of the status quo

Hopscotch-style on-chain: 75-80% of first-time coin buyers still buy coins on centralized exchanges (Binance, Coinbase) first, and then transfer to self-custodial wallets or DeFi protocols, resulting in 2 KYCs, 2 sets of fees, and at least 1 cross-chain bridge.

Difficulty in withdrawing cash: US licensed CEX can freeze fiat currency for 24-72 hours; EU banks increasingly mark outbound SEPA transfers as high risk.

High fees: Deposit spreads ~ 0.8% (ACH) to 4-5% (credit card); stablecoin withdrawal fees fluctuate between 0.1-7% depending on region and volume.

Lack of aggregated yield solutions: There is no one-stop DeFi module that allows users to centrally obtain yield stacks.

Payment giants are rushing to the beach

PayPal now allows US users to withdraw PYUSD directly to Ethereum and Solana and refund to any debit card in <30 seconds (fee rate 0.4-1%).

Stripe opened the Crypto Withdrawal API to all platforms in April 2025, allowing instant withdrawal of USDC to local channels in 45 countries.

MoonPay processed $18.6 billion in transactions for 14 million users last year, achieving a year-on-year growth of 123% due to the addition of instant withdrawal services covering 160+ countries.

Portrait of PMF

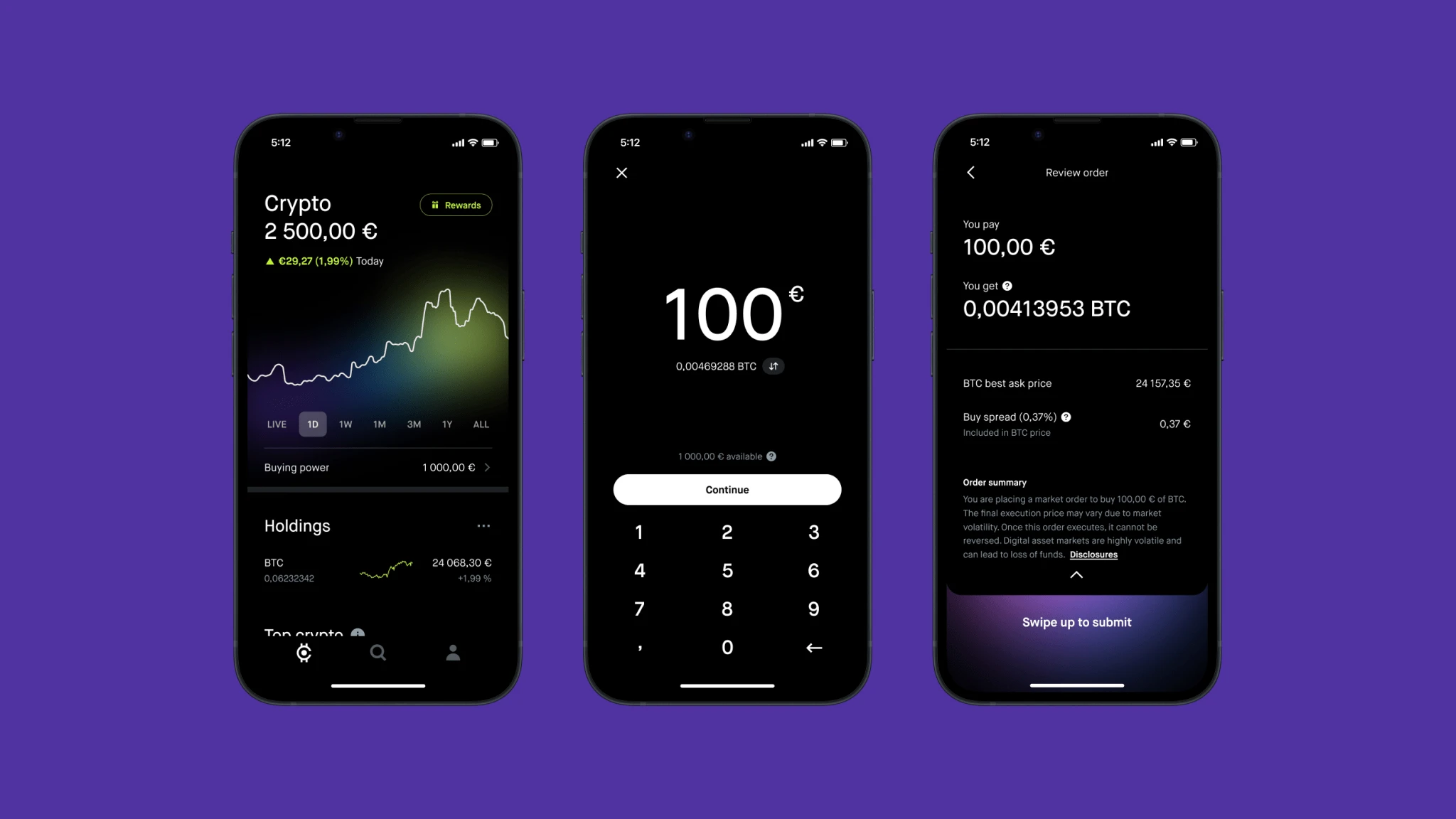

A global super app that allows users to deposit/withdraw seamlessly, have a simple interface, and access all DeFi functions on a single platform.

A single platform account holds funds, which can be seamlessly connected to bank accounts and crypto wallets

Only large amounts require KYC

No high fees or withdrawal delays

Like a savings account but denominated in crypto

Yield aggregator, integrated with major lending protocols (Aave, Kamino, Morpho) and staking

Covers mainstream spot/perpetual trading interfaces

The closest thing to this North Star at the moment is Robinhood: minimalist UI/UX, coupled with bank and wallet integration; it may be the leader in this field.

Entertainment/ Media/ Social

Current content platforms (YouTube, Twitch, Facebook) mainly rely on grabbing user attention and selling it to advertisers through display ads. However, this conversion chain is inherently inefficient, losing potential customers at multiple stages of the funnel. More importantly, display ads forcefully insert content, which naturally destroys UX.

The encryption paradigm can completely rewrite and optimize the traditional Web2 entertainment platform structure.

Platform level unlocking:

Introducing and generating new revenue streams

DEX Integration — Exchange Fees

Creator Pegged Tokens

Live Event Betting

Prize Pool

Airdrop to users

Remove ads to improve user retention

No more reliance on external stakeholders

A new profit sharing method with creators

Exchange Fee Share

Competition fee share

In this new paradigm, the platform itself is a distribution channel rather than a monetization product. Web2 has precedents: Twitch → Amazon, Kick → Stake, Twitter → Membership Subscription + GrokAI; Web3 has also taken shape, such as Parti and Pump.fun live broadcasts.

User level unlock

Removing ads brings better UX

Benefit from supporting/watching your favorite creators through bonus pools and airdrops

Token dividends

Creator Tier Unlock

Contribution-based revenue model; more transparent and fair

Exchange Fee Share

Competition fee share

Creator tokens enable direct value flow from fans to creators

Removing advertisements improves user retention

The platform model brings inherent user growth, and creators benefit

Why not AI or games?

At present, AI consumer applications are still in their early stages. We need to wait until the emergence of applications that can truly achieve one-click DeFi/account management before we can usher in an explosion; the current level of security and feasibility infrastructure is still insufficient.

In terms of games, it is difficult for blockchain games to break through the circle because the core users are mostly farmers who pursue money rather than game fun, and the retention rate is low. However, in the future, there may be games that implicitly use encryption paradigms (such as economic and item systems) at the bottom layer, and the focus of players/developers is still on playability - if CSGO had used the on-chain economy, it might have been very successful.

In this regard, there have been some successful cases of mini-games that utilize encryption mechanisms (Freysa, DFK, Axie).

Argument and Framework

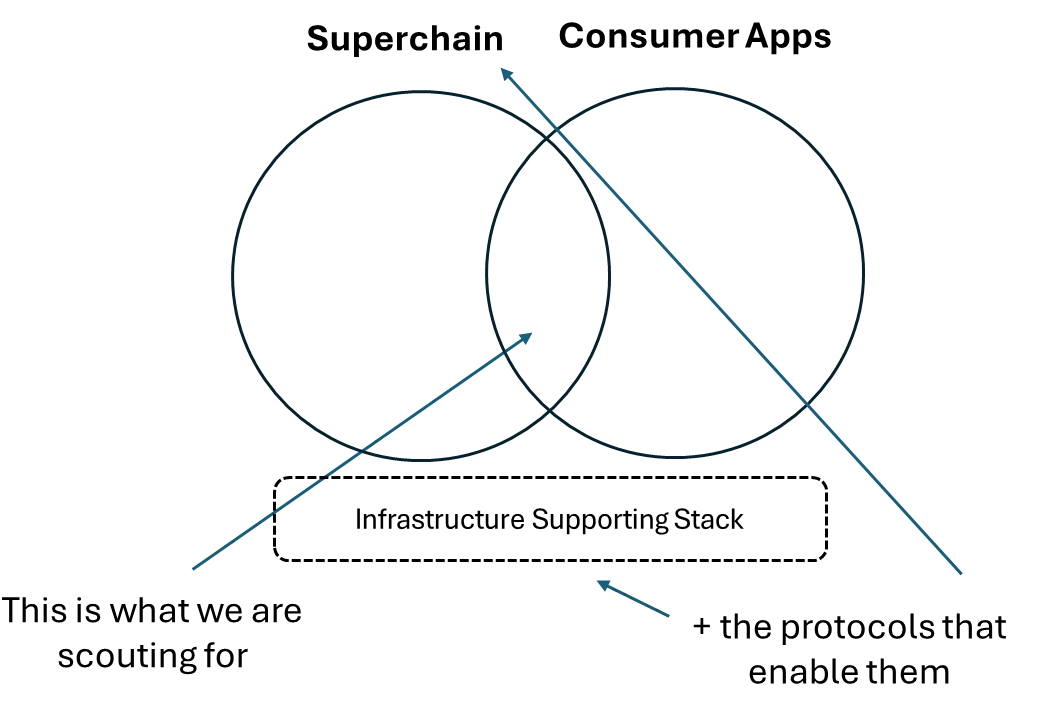

Overall view: Market maturity → Inter-chain fragmentation reduction → A few super chains win → Institutions should bet on the next generation of consumer applications and their supporting infrastructure on these super chains.

This trend is already happening, with activity becoming concentrated in a small number of chains rather than being spread across 100+ L2s.

Here, super chain refers to consumer-centric chains that optimize speed and experience, such as Solana, Hyperliquid, Monad, and MegaETH.

analogy:

Hyperchain: iOS, Android

Apps: Instagram, Cash App, Robinhood

Support stack: AWS, Azure, Google Cloud

As mentioned earlier, consumer applications can be broken down into two key areas:

Web2 Native: Applications that attract Web2 users first, leveraging the crypto paradigm to unlock new behaviors - products that seamlessly integrate crypto on the backend but don’t call themselves “crypto applications” (e.g. Polymarket) should be the focus.

Web3 native: The proven determining factors are better UX + ultra-fast interface + sufficient liquidity + one-stop solution (breaking fragmentation). The new generation of Web3 users value UX more than revenue or technology, and only care about the latter two after exceeding a certain threshold. Teams and applications that understand this deserve a valuation premium.

The following elements are generally required:

Conclusion

Consumer investment targets do not have to rely entirely on differentiated value propositions (although they can). Snapchat is not a technological revolution, but a re-combination of existing technologies (chat module, camera AIO) to create new unlocking. Therefore, it is biased to evaluate consumer targets from the perspective of traditional infrastructure; institutions should consider: Can the project become a good business and ultimately generate returns for the fund.

To this end, it should be assessed:

Distribution capabilities are more important than the product itself - can they reach users?

Are the existing modules effectively reorganized to create a new experience?

Funds can no longer rely on pure infrastructure to drive returns. It’s not that infrastructure is unimportant, but they must have real appeal and use cases in a market where narrative is king, rather than value propositions that no one cares about. In general, for consumer targets, most investors are too right-biased - too literally pursuing first principles, while the real winners often rely on better brands and UX - these characteristics are implicit but critical.