Original article by: Sumanth Neppalli, Joel John

Original translation: Luffy, Foresight News

Remember Sam Bankman-Fried? He used to work at Jane Street and later became famous for his “effective altruism” experiments and embezzlement. In the past month, Jane Street has been in the news for two things:

One is suspected of assisting the coup (allegedly); the other is conducting arbitrage trading experiments in the Indian options market (also allegedly, after all, I cant afford a lawyer who can beat them in court).

Some of these trades were so large that the Indian government decided to ban Jane Street from doing business in the country altogether and seized their funds. Matt Levine wrote a great summary of this in his Bloomberg column, but in short, this “arbitrage” works like this:

Sell put options in a liquid market (e.g. $100 million);

Steadily go long the underlying asset in a thinly liquid market (e.g. $10 million in daily trading volume).

In markets like India, options trading volume is often several times that of the underlying stock. This is a market feature, not a bug. Even if the underlying asset is insufficient, the market can always find liquidity. For example, the total volume of gold ETFs far exceeds the actual gold reserves; for another example, the surge in GameStops stock price in 2022 was partly due to the fact that the size of its short position exceeded the number of outstanding shares. Lets get back to the topic and return to the Jane Street case.

When you buy a put option, you are betting that the price will fall, or in other words, you buy the right to sell the asset at a predetermined price (i.e., the strike price). Buying a call option is the opposite: you buy the right to buy the asset at a preset price. Let me explain this using the example of the upcoming PUMP token.

Assuming I bet that the fully diluted valuation (FDV) of PUMP tokens will be less than $4 billion when it launches (perhaps out of dislike for VCs and the meme market), I will buy put options. The person who sells me the options may be a VC who holds a quota of PUMP tokens and believes that the price will be higher when it launches.

The venture capital firm that sells the put option will receive a premium. Assuming I pay a premium of $0.10, if the token is listed at $3.10 and my strike price is $4, then I can make a profit of $0.90 by exercising the put option, and the actual profit after deducting the premium is $0.80. The venture capital firm is forced to sell the token at a price lower than expected ($3.10), which is equivalent to a loss of $0.90 in price difference.

Why would I do this? Because the leverage is extremely high: I can short an asset worth $4 by investing $0.1. Why is the leverage so high? Because the person selling the option (the VC) believes that the price will not fall below $4. Worse, the VC (and his network) may buy the PUMP at $4 to ensure that the price remains at $4.5 when the option is exercised. This is exactly what the Indian government accused Jane Street of doing.

Source: Bloomberg

In Jane Street’s case, though, they weren’t trading PUMP tokens. They were trading Indian stocks, specifically, the NIFTY banking index. Retail investors often trade options because of the high leverage offered in that market. All they have to do is buy some of the relatively illiquid underlying stocks that make up the index.

Then, as spot buying pushes up the index price, sell index call options at a higher premium; buy index put options at the same time; and finally sell stocks to pull down the index. Profits come from call option premiums and put option gains. There may be a small loss in spot trading, but the put option gains are usually enough to cover this loss.

The above chart explains how this trade works: the red line is the index trading price, and the blue line is the option trading price. In effect, they sell options (pushing the price down and collecting premiums) and buy the underlying asset (pushing the price up and not having to pay for the option) - its all arbitrage.

How does this relate to today’s topic?

It doesnt matter. I just want to explain the concept of puts, calls and strike prices to people who are new to these terms.

In this episode, Sumanth and I discuss a simple question: Why hasn’t the crypto options market exploded? With Hyperliquid leading the narrative, on-chain perpetual swaps are hot again, and stock perpetual swaps are about to go live, but what about options? As with most things, we start with historical context, then analyze the details of how these markets work, and finally look to the future. Our hypothesis is: if perpetual swaps take hold, the options market will follow.

The question is: which teams are developing options products, and what mechanisms will they adopt to avoid repeating the mistakes of DeFi Summer 2021?

We don’t have definitive answers yet, but we can offer some clues.

The puzzle of perpetual contracts

Remember the pandemic? The “good old days” when we sat at home and speculated on how long this massive social isolation experiment would last. That’s when we saw the limitations of the perpetual contract market. Like many commodities, oil has a futures market where traders can bet on its price. But like all commodities, oil is only valuable if there is demand for it. The restrictions caused by the pandemic have led to a sharp drop in demand for oil and related products.

When you buy a physically delivered futures contract (non-cash settled), you acquire the right to receive the underlying asset at an agreed price in the future. So if I am long oil, I will receive the oil when the contract expires. Most traders do not actually hold the commodity, but instead sell it to a factory or counterparty that has the logistics capabilities (such as tanker trucks).

But in 2020, things got out of control. No one wanted that much oil, and traders who bought futures contracts had to take on custody responsibilities. Imagine: Im a 27-year-old analyst at an investment bank, and I have to take delivery of 1 million gallons of oil; my 40-something compliance director will definitely make me sell it all first. And thats exactly what happened.

In 2020, oil prices fell to negative values. This vividly demonstrates the limitations of physical futures: you have to take delivery of the goods, and taking delivery of goods costs money. If I am just a trader betting on the price of oil, chicken or coffee beans, why should I take delivery of the physical goods? How can I transport the goods from the place of production to the port of Dubai? This is the structural difference between cryptocurrency futures and traditional futures.

In the cryptocurrency space, receiving the underlying asset costs almost nothing: it just needs to be transferred to a wallet.

However, the cryptocurrency options market has never really exploded. In 2020, the U.S. options market traded about 7 billion contracts; today, that number is close to 12 billion, with a notional value of about $45 trillion. The U.S. options market is about seven times the size of the futures market, with nearly half of the trades coming from retail investors who are keen on short-term options that expire that day or weekend. Robinhoods business model is based on this: providing fast, convenient, and free options trading channels, and making profits through a pay for order flow model (paid by market makers such as Citadel).

But the situation of cryptocurrency derivatives is completely different: the monthly trading volume of perpetual contracts is about 2 trillion US dollars, which is 20 times that of options (about 100 billion US dollars per month). The cryptocurrency market did not inherit the existing model of traditional finance, but built its own ecosystem from scratch.

The regulatory environment has shaped this difference. Traditional markets are subject to the constraints of the U.S. Commodity Futures Trading Commission (CFTC), which requires futures to be rolled over, which brings operational friction; U.S. regulations set the upper limit of stock margin leverage at about 2 times and prohibit 20x perpetual contracts. Therefore, options have become the only way for Robinhood users (such as retail investors with only $500) to convert a 1% fluctuation in Apple stock into a return of more than 10%.

The unregulated environment of cryptocurrencies has created space for innovation. It all started with BitMEX’s perpetual futures: As the name suggests, these futures have no “delivery” date and are permanent. You don’t need to hold the underlying asset, you just trade it over and over again. Why do traders use perpetual contracts? Two reasons:

Compared with spot trading, perpetual contracts have lower fees;

Perpetual contracts have higher leverage.

Most traders like the simplicity of perpetual contracts. In contrast, options trading requires understanding multiple variables at the same time: strike price selection, underlying asset price, time decay, implied volatility, and delta hedging. Most cryptocurrency traders transition directly from spot trading to perpetual contracts, skipping the options learning curve completely.

In 2016, BitMEX launched perpetual contracts, which instantly became the favorite leverage tool for cryptocurrency traders. In the same year, a small Dutch team launched Deribit, the first trading platform dedicated to cryptocurrency options. At the time, the price of Bitcoin was below $1,000, and most traders thought options were too complicated and unnecessary. 12 months later, the wind suddenly changed: Bitcoin soared to $20,000, and miners with huge inventories began buying put options to lock in profits. In 2019, Ethereum options went online; by January 2020, options open interest exceeded $1 billion for the first time.

Today, Deribit handles more than 85% of cryptocurrency options trading volume, which shows that the market is still very concentrated. When institutions need to trade large amounts, they don’t choose the order book, but contact the inquiry desk or communicate on Telegram, and then settle through the Deribit interface. A quarter of Deribit’s trading volume comes from this private channel, highlighting the dominance of institutions in this seemingly retail-dominated market.

Deribit is unique in that it allows cross-market collateralization. For example, you go long futures ($100,000 in Bitcoin) and buy a $95,000 put option at the same time. If the price of Bitcoin falls, the long futures will lose money, but the value of the put option will avoid liquidation. Of course, there are many variables here, such as option expiration time or futures leverage, but Deribits cross-market collateralization feature is a key reason for its dominance.

In theory, on-chain options can easily achieve this: smart contracts can track strike prices and expiration dates, custody collateral, and settle proceeds without intermediaries. However, after five years of experimentation, the total trading volume of decentralized options exchanges is still less than 1% of the options market, while perpetual contract decentralized exchanges account for about 10% of futures trading volume.

To understand why, we need to review the three stages of development of on-chain options.

The Stone Age of Options

In March 2020, Opyn started democratizing the issuance of options: lock ETH as collateral, select the strike price and expiration date, and the smart contract will mint ERC 20 tokens representing the rights. These tokens can be traded on any platform that supports ERC 20: Uniswap, SushiSwap, or even direct wallet transfers.

Each option is a separate tradable token: the July $1,000 call option is one token, the $1,200 call option is another, which leads to a fragmented user experience, but the market works normally. At expiration, the in-the-money option holder can exercise the option and receive a profit, and the contract returns the remaining collateral to the seller. To make matters worse, the seller must lock in the full notional value: selling a 10 ETH call option requires freezing 10 ETH until expiration to earn a 0.5 ETH premium.

This system worked well until the DeFi Summer. When gas fees soared to $50-200 per transaction, the cost of issuing an option often exceeded the premium itself, and the entire model collapsed almost overnight.

Developers are turning to a Uniswap-style liquidity pool model. Hegic has led this change, allowing anyone from retail investors to whales to deposit ETH into a public vault. Liquidity providers (LPs) pool collateral into a pool, and smart contracts quote options buys and sells. Hegics interface allows users to select strike prices and expiration dates.

If a trader wants to buy a 1 ETH call option for next week, the automated market maker (AMM) will use the Black-Scholes model to price and obtain ETH volatility data from an external oracle. After the trader clicks Buy, the contract will take 1 ETH from the pool as collateral, mint an NFT that records the strike price and expiration date, and send it directly to the buyers wallet. The buyer can resell the NFT on OpenSea at any time, or wait for expiration.

For users, it’s almost like magic: a trade is done, no counterparty is needed, and the premium flows to LPs (minus protocol fees). Traders like the one-click experience, and LPs like the yield; the vault can issue multiple strike prices/expirations at the same time without active management.

This magic lasted until September 2020. Ethereum experienced a violent crash, and Hegics simple pricing rules caused put options to be sold too cheaply. Put option holders exercised their options, forcing the vault to pay far more ETH than expected. In just one week, a years premium income was wiped out, and LPs learned a painful lesson: issuing options in a calm market seems easy, but without proper risk management, a storm can empty everything.

AMMs must lock up collateral to underwrite options

Lyra (now renamed Derive) attempts to solve this problem by combining liquidity pools and automated risk management: After each trade, Lyra calculates the net delta exposure of the pool (the sum of option deltas for all strike prices and expiration dates). If the vault has a net short exposure of 40 ETH, it means that for every $1 increase in the price of ETH, the vault will lose $40. Lyra will establish a long position of 40 ETH on the Synthetix perpetual contract to hedge directional risk.

AMM uses Black-Scholes pricing, which offloads expensive on-chain computations to off-chain oracles to control gas fees. This delta hedging reduces treasury losses by half compared to an unhedged strategy. Despite its ingenious design, the system relies on Synthetix’s liquidity.

When the Terra Luna crash triggered panic, traders withdrew from the Synthetix staking pool, and liquidity dried up, causing Lyra’s hedging costs to soar and spreads to widen significantly. Complex hedging requires deep sources of liquidity, which DeFi has so far struggled to reliably provide.

Finding Fire

Decentralized Option Vaults (DOVs) sell order flow via auction. Source: Treehouse Research

In early 2021, decentralized option vaults (DOVs) emerged. Ribbon Finance pioneered this model, and the strategy is simple: users deposit ETH into the vault and sell covered call options through off-chain auctions every Friday. Market makers bid on order flow, and the premium is returned to depositors as income. The entire process is reset every Thursday after the options are settled and the collateral is unlocked.

During the 2021 bull run, implied volatility (IV) remained above 90%, and weekly premiums converted into amazing annualized returns (APYs). Weekly auctions continued to generate impressive returns, and depositors enjoyed seemingly risk-free ETH returns. But when the market peaked in November and ETH began to fall, the vault began to have negative returns, and the premium income was not enough to cover the decline in ETH.

Competitors Dopex and ThetaNuts copied this model and added rebate tokens to cushion the blow during periods of loss, but still failed to address the core vulnerability to large fluctuations. In both the AMM and DOV models, funds are locked until the expiration date. Users who deposit ETH to earn premiums will be stuck when ETH falls and cannot close their positions when needed.

Order Book

The Solana ecosystem team has learned from the limitations of AMMs in early options protocols and taken a completely different approach. They tried to replicate Deribits central limit order book (CLOB) model on the chain, using a complex order matching engine to achieve near-instant settlement and introducing market makers as the sellers counterparty for each option.

First-generation products such as PsyOptions attempt to place order books entirely on-chain. Each quote takes up block space, and market makers must lock 100% of collateral, so quotes are scarce. Second-generation products such as Drift and Zeta Markets move order books off-chain and settle on-chain after matching. The Ribbon team returned to the battlefield with Aevo, placing the order book and matching engine on the high-performance Optimism Layer 2.

More importantly, these products support perpetual contracts and options on the same platform, with a combined margin system that calculates the net exposure of market makers. This is the same success factor of Deribit, allowing market makers to reuse collateral.

The results were mixed. Spreads narrowed as market makers could frequently update quotes without paying high gas fees. But the weakness of the CLOB model emerged during non-trading hours: when professional market makers in the United States went offline, liquidity evaporated, and retail traders faced huge spreads and poor execution prices. This reliance on active market makers led to temporary dead zones, which AMMs, despite their flaws, never experienced. Teams such as Drift turned completely to perpetual contracts and abandoned options.

Teams such as Premia are exploring the AMM-CLOB hybrid model, seeking a middle ground between the full-chain order book that provides 24/7 liquidity and the market maker that can increase depth. However, the total locked value (TVL) has never exceeded $10 million, large transactions still require market makers to intervene, and slippage remains high.

Why options are struggling

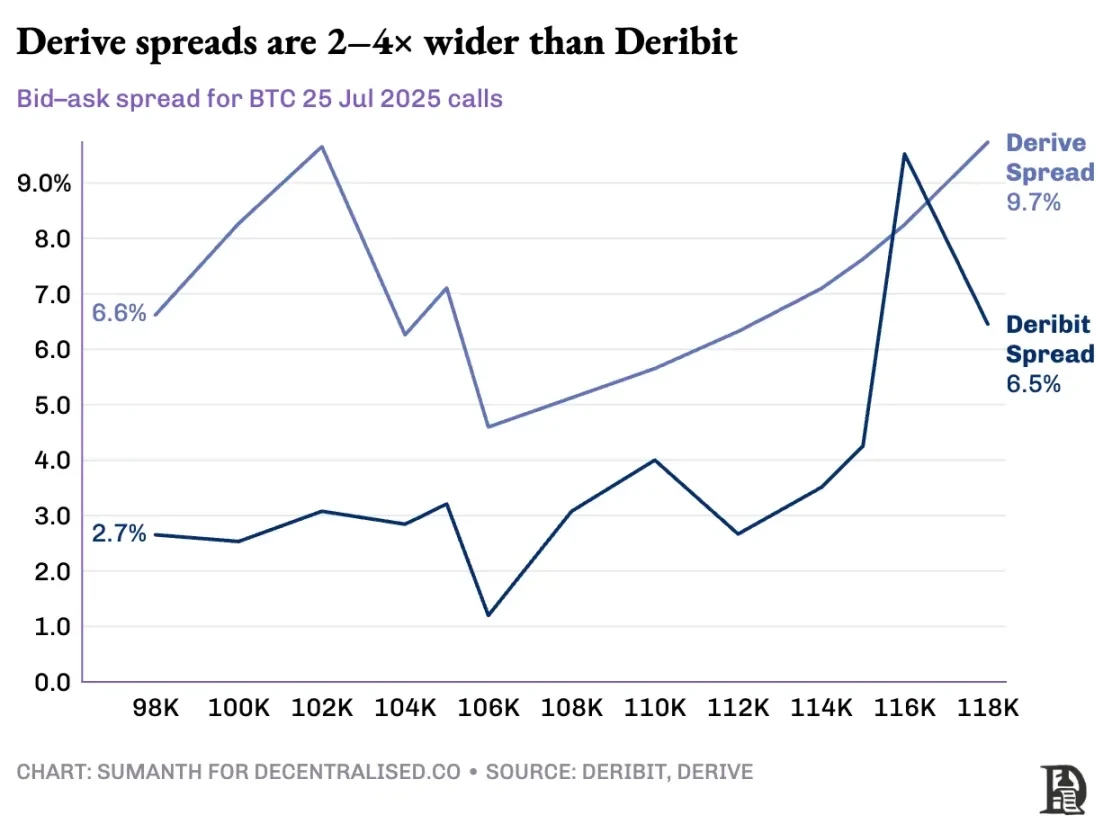

Options liquidity is flowing from AMM to order books. Derive decommissioned the on-chain AMM, rebuilt the exchange around the order book, and equipped it with a cross-margin risk engine. This upgrade attracted Galaxy and GSR, among others, and the platform now handles about 60% of on-chain options trading volume, making it the largest decentralized options exchange in DeFi.

Vlad on limit order book design

When a market maker sells a $120,000 BTC call option and hedges it with spot BTC, the system identifies these offsetting positions and calculates margin requirements based on net portfolio risk rather than individual position requirements. The engine continuously evaluates each position: underwriting a $120,000 call option expiring in January 2026, shorting the weekly contract for next week, buying spot BTC, and requiring traders to post margin based on the net directional exposure.

Hedging offsets risk, freeing up collateral to be redeployed into the next quote.

On-chain protocols break this cycle when they tokenize each strike price and expiration date into their own ERC-20 token pool. The 120k call options minted next Friday cannot identify the hedge of the BTC perpetual contract. While Derive has partially solved this problem by adding perpetual contracts to its clearinghouse to enable cross-margining, the spreads are still much higher than Deribit; the spreads for equivalent positions are often 2-5 times higher.

Note: Let’s use the price of mangoes to explain. Suppose I sell someone the right to buy mangoes for $10 and receive a $1 premium. These mangoes will ripen in three days. As long as I have mangoes (spot assets), I can collect the premium ($1) without worrying about the market price of mangoes rising.

I won’t lose money (hence hedged) unless the price of mangoes goes up and there is an opportunity cost. If Sumanth buys the option (paying me $1), he can turn around and sell the mangoes for $15, netting $4 after deducting the premium. These three days are the expiration date of the option. At the end of the trade, I either still have the mangoes or I get a total of $11 ($10 mango money + $1 premium).

On a centralized exchange, my mango farm and the market are in the same town, and they know the collateral for my trade, so I can use the premium paid by Sumanth as collateral to offset other expenses (such as labor costs). But on an on-chain market, the two markets are theoretically located in different locations and do not trust each other. Since most markets rely on credit and trust, this model is capital inefficient - I may lose money just to pass on Sumanths payment to the logistics provider.

Deribit benefits from years of API development and systems optimized for its platform by many algorithmic trading platforms. Derive’s risk engine has been online for just over a year and lacks the large order books required for spot and perpetual contract markets for effective hedging. Market makers need instant access to deep liquidity in multiple instruments to manage risk, and they need to be able to hold option positions simultaneously and hedge easily through perpetual contracts.

Perpetual swap decentralized exchanges solve the liquidity problem by completely eliminating fragmentation. All perpetual swaps for the same asset are the same: one deep pool, one funding rate, and uniform liquidity regardless of whether the trader chooses 2x or 100x leverage. Leverage only affects margin requirements, not market structure.

This design has made platforms like Hyperliquid remarkably successful: its vaults typically act as counterparties to retail trades, distributing transaction fees to vault depositors.

In contrast, options fragment liquidity into thousands of “micro-assets”: each strike-expiration combination forms an independent market with unique characteristics, resulting in fragmented funds and almost impossible to reach the depth required by sophisticated traders. This is the core reason why on-chain options have not taken off. However, given the liquidity emerging on Hyperliquid, this situation may change soon.

The Future of Crypto Options

Looking back at the launch of all major options protocols over the past three years, a clear pattern emerges: capital efficiency determines survival. Protocols that force traders to lock up separate collateral for each position eventually lose liquidity, no matter how sophisticated their pricing models or how slick their interfaces.

Professional market makers work on razor-thin margins, and they need every penny to operate efficiently across multiple positions. If a protocol requires them to post $100,000 in collateral for a Bitcoin call option, and another $100,000 for a perpetual swap used for hedging, instead of treating that collateral as an offset to risk (which might only require $20,000 in net margin), then participating in the market is unprofitable. Simply put: no one wants to tie up a lot of money and make only a little money.

Source: TheBlock

Spot markets such as Uniswap often trade over $1 billion per day with minimal slippage, and perpetual contract decentralized exchanges such as Hyperliquid process hundreds of millions of dollars in daily volume with spreads that compete with centralized exchanges. The liquidity foundation that options protocols so desperately need now exists.

The bottleneck is always infrastructure: the “plumbing” that professional traders take for granted. Market makers need deep liquidity pools, instant hedging capabilities, instant liquidation when positions go bad, and a unified margin system that treats the entire portfolio as a single exposure.

We’ve written about Hyperliquid’s shared infrastructure approach before, which creates the positive-sum state that DeFi has long promised but rarely achieved: each new application strengthens the entire ecosystem rather than competing for scarce liquidity.

We believe that options will eventually come on-chain through this infrastructure first approach. Early attempts focused on mathematical complexity or clever token economics, while HyperEVM solves the core plumbing problems: unified collateral management, atomic execution, deep liquidity, and instant liquidation.

We see several core areas where market dynamics are changing:

After the FTX crash in 2022, fewer market makers participated in new primitives and took risks; today, traditional institutional players are returning to the cryptocurrency market.

There are more proven networks that can handle higher transaction throughput needs.

The market is more accepting of some logic and liquidity not being fully on-chain.

If options are to return, three types of talent may be needed: developers who understand how the product works, experts who understand market maker incentives, and people who can package these tools into retail-friendly products. Can on-chain options platforms enable some people to make life-changing fortunes? After all, Memecoin did it - they made the dream of making millions with a few hundred dollars a reality. Memecoins high volatility made it work, but it lacked the Lindy effect (the longer it exists, the more stable it becomes).

In contrast, options have both the Lindy effect and volatility, but are difficult for the average person to understand. We believe there will be a class of consumer applications focused on bridging this gap.

Todays cryptocurrency options market is similar to the state before the Chicago Mercantile Exchange (CBOE) was established: a bunch of experiments, lack of standardization, and mainly for speculation rather than hedging. But as the crypto infrastructure matures and truly goes into commercial operation, this situation will change. Institutional-grade liquidity will be on-chain through reliable infrastructure, supporting cross-margin systems and composable hedging mechanisms.