Original author: Will Awang, investment and financing lawyer, Digital Assets Web3; independent researcher, tokenization RWA payment.

If I were to imagine how finance would work in the future, I would undoubtedly introduce the many advantages that digital currency and blockchain technology can bring: 24/7 availability, instant global liquidity, fair access without permission, asset composability, and transparent asset management. And this imagined future financial world is being gradually built through tokenization.

Blackrock CEO Larry Fink emphasized the importance of tokenization for the future of finance in early 2024: “We believe that the next step in financial services will be the tokenization of financial assets, which means that every stock, every bond, every financial asset will run on the same general ledger.”

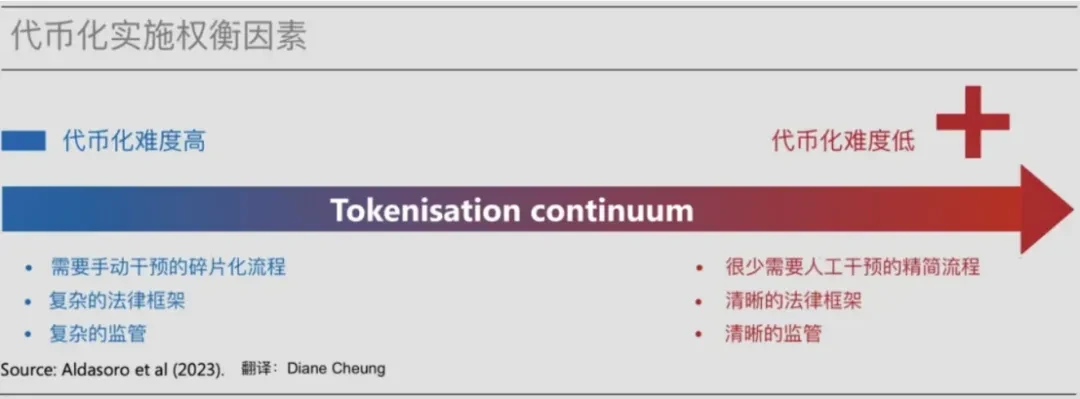

Asset digitization can be fully rolled out with the maturity of technology and measurable economic benefits, but the large-scale and widespread adoption of asset tokenization will not happen overnight. The most challenging point is that in the strictly regulated industry of financial services, the infrastructure of traditional finance needs to be transformed, which requires the participation of all players in the entire value chain.

Nevertheless, we can already see that the first wave of tokenization has arrived, mainly benefiting from investment returns in the current high interest rate environment and driven by practical use cases of existing scale (such as stablecoins, tokenized US bonds). The second wave of tokenization may be driven by use cases of asset classes that currently have a smaller market share, less obvious returns, or require solving more severe technical challenges.

This article attempts to examine the potential benefits and long-standing challenges of tokenization from the perspective of traditional finance through McKinsey Cos analytical framework for tokenization. At the same time, combined with real and objective cases, it concludes that although challenges still exist, the first wave of tokenization has arrived.

TL;DR

Tokenization refers to the process of creating a digital representation of an asset on a blockchain;

Tokenization brings many advantages: 24/7 availability, instant global liquidity, permissionless and fair access, asset composability, and transparency in asset management;

In financial services, the focus of tokenization is shifting to “blockchain, not cryptocurrency”;

Despite the challenges, the first wave of tokenization has arrived with the massive adoption of stablecoins, the launch of tokenized U.S. Treasuries, and the clarification of the regulatory framework;

McKinsey estimates that by 2030, the total market value of the tokenized market could reach approximately $2 trillion to $4 trillion (excluding the market value of cryptocurrencies and stablecoins);

Comparing the current state of the tokenization market to major paradigm shifts in other technologies shows that we are in the early stages of the market;

The next wave of tokenization is likely to be led by financial institutions and market infrastructure players.

1. What is tokenization?

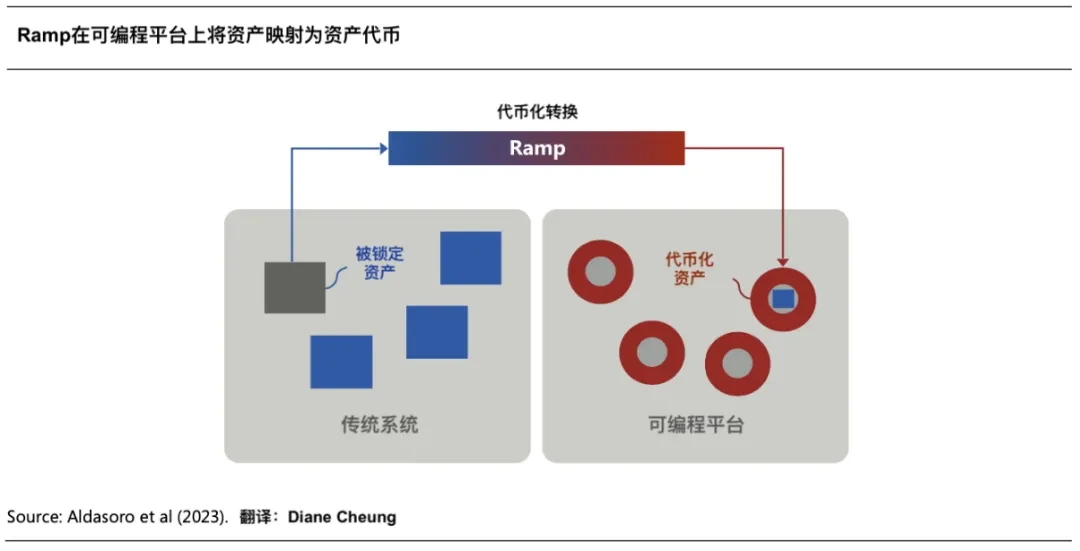

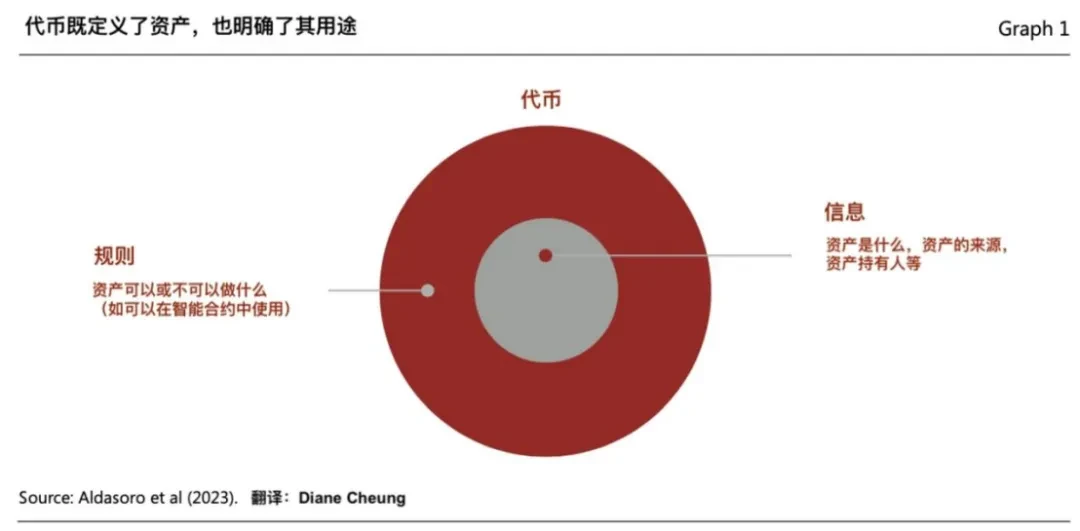

Tokenization refers to the process of recording the ownership of financial or real assets that exist on traditional ledgers onto a blockchain programmable platform to create a digital representation of the assets. These assets can be traditional tangible assets (such as real estate, agricultural or mining commodities, analog artworks), financial assets (stocks, bonds) or intangible assets (such as digital art and other intellectual property).

The resulting tokens refer to ownership certificates (Claims) recorded on the blockchain programmable platform for trading. Tokens are not just single digital certificates, but also usually bring together the rules and logic that manage the transfer of underlying assets in traditional ledgers. Therefore, tokens are programmable and customizable to meet personalized scenarios and regulatory compliance requirements.

(Tokenization and unified ledger - blueprint for building a future monetary system)

The “tokenization” of an asset involves the following four steps:

1.1 Determine the underlying assets

The process begins when an asset owner or issuer determines that an asset would benefit from tokenization. This step requires clarity on the structure of the tokenization, as the specifics will determine the design of the entire tokenization scheme, for example, the tokenization of a money market fund is different from the tokenization of carbon credits. The design of the tokenization scheme is critical to clarify whether the tokenized asset will be considered a security or a commodity, what regulatory framework will apply, and which partners will be worked with.

1.2 Token Issuance and Custody

Creating a blockchain-based digital representation of an asset requires first locking in the underlying asset to which the digital representation corresponds. This will involve transferring the asset to a controlled entity (whether physical or virtual), usually a qualified custodian or licensed trust company.

A digital representation of the underlying asset is then created on the blockchain in the form of a specific token with embedded functionality to execute the code for the predetermined rules. To do this, the asset owner chooses a specific token standard (ERC-20 and ERC-3643 are common standards), a network (private or public blockchain), and the functionality to be embedded (e.g., user transfer restrictions, freezing functions, and clawbacks), which can be implemented by the tokenization service provider.

1.3 Token Distribution and Trading

Tokenized assets can be distributed to end investors through traditional channels or new channels such as digital asset exchanges. Investors need to set up an account or wallet to hold digital assets, and any physical asset equivalents remain locked in the issuers account at a traditional custodian. This step usually involves a distributor (for example, the private wealth department of a large bank) and a transfer agent or trading broker.

Depending on the issuer and asset class, it may also be possible to list through secondary market trading venues to create a liquid market for these tokenized assets after issuance.

1.4 Asset Services and Data Verification

Digital assets that have been distributed to end investors still require ongoing services, including regulatory, tax and accounting reporting, and periodic calculation of net asset value (NAV). The nature of the services depends on the asset class. For example, services for carbon credit tokens require different audits than fund tokens. Services need to coordinate off-chain and on-chain activities and handle a wide range of data sources.

The current tokenization process is relatively complex. In a money market fund tokenization scheme, up to nine parties are involved (asset owner, issuer, traditional custodian, tokenization provider, transfer agent, digital asset custodian or trading broker, secondary market, distributor and end investor), which is two more parties than the traditional asset process.

2. Advantages of Tokenization

Tokenization enables assets to access the enormous potential of digital currencies and blockchain technology. Broadly speaking, these benefits include: 24/7 operations, data availability, and so-called instant atomic settlement. In addition, tokenization provides programmability - the ability to embed code in tokens and the ability for tokens to interact with smart contracts (composability) - allowing for a higher degree of automation.

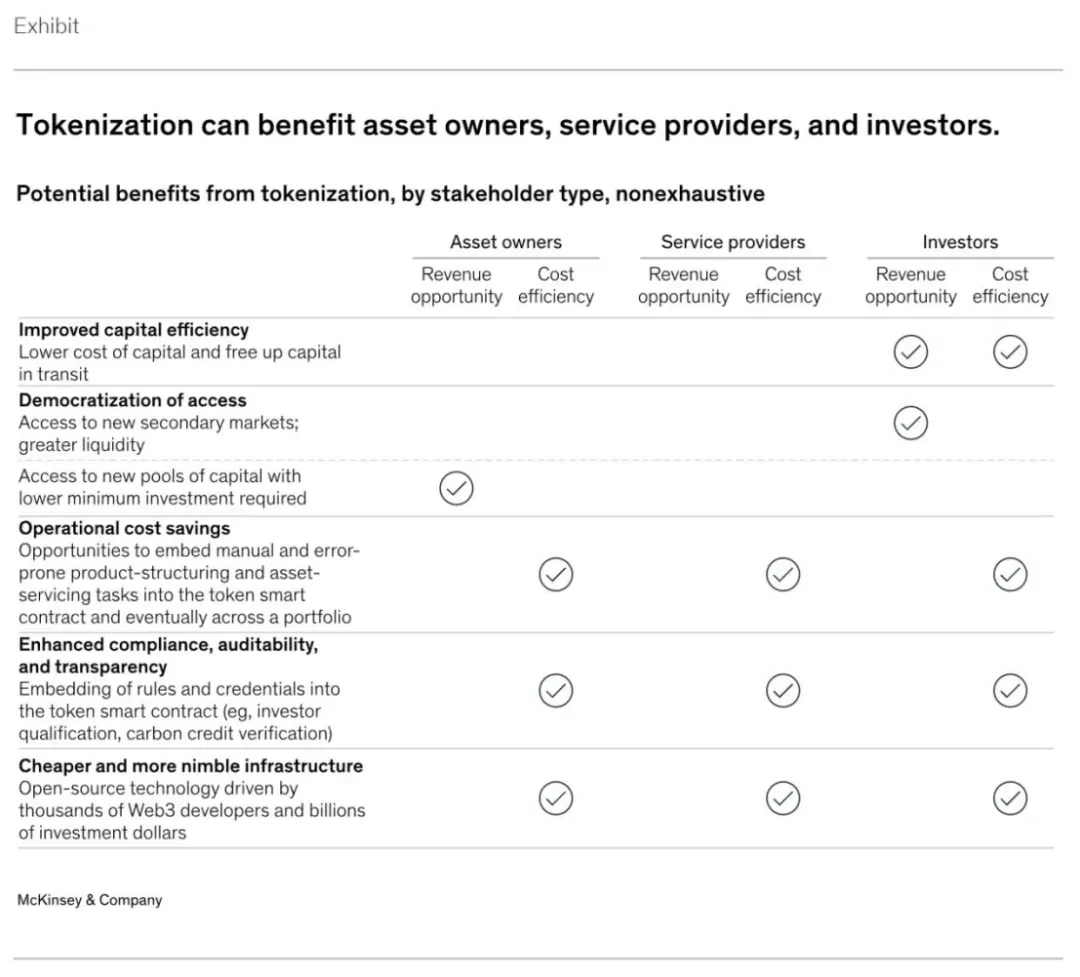

More specifically, when asset tokenization is promoted on a large scale, in addition to proof of concept, the following advantages will become increasingly prominent:

2.1 Improving capital efficiency

Tokenization can significantly improve the capital efficiency of assets in the market. For example, tokenized repurchase agreements (Repo) or money market fund redemptions can be completed instantly in a few minutes T+0, while the current traditional settlement time is T+2. In the current high-interest market environment, shorter settlement times can save a lot of money. For investors, these savings in funding rates may be the reason why recent tokenized U.S. debt projects can have a huge impact in the near future.

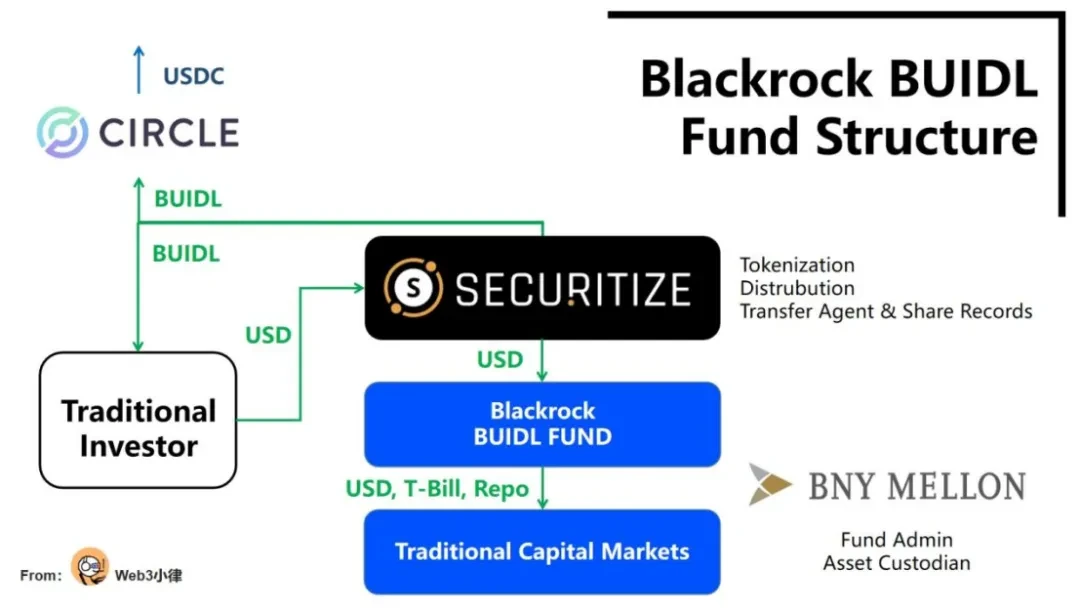

On March 21, 2024, Blackrock and Securitize jointly launched the first tokenized fund BUIDL on the public blockchain Ethereum. After the fund is tokenized, it can achieve real-time settlement of the unified ledger on the chain, greatly reducing transaction costs and improving capital efficiency. It can achieve (1) 24/7/365 fund subscription/redemption of fiat currency USD. This instant settlement and real-time redemption function is what many traditional financial institutions are very eager to achieve; at the same time, in cooperation with Circle, it can achieve (2) 24/7365 real-time exchange of stable currency USDC and fund token BUIDL at a 1:1 ratio.

This tokenized fund, which can link traditional finance and digital finance, is a milestone innovation for the financial industry.

(Analysis of Blackrocks tokenized fund BUIDL, opening up a brave new world of DeFi for RWA assets)

2.2 Permissionless Democratic Access

One of the most touted benefits of tokenization or blockchain is the democratization of access. This permissionless entry barrier, coupled with the fragmentation of tokens (i.e., dividing ownership into smaller shares, lowering the investment threshold), may increase asset liquidity, but only if the tokenized market can be popularized.

In some asset classes, streamlining intensive manual processes through smart contracts can significantly improve unit economics, making it possible to serve a smaller pool of investors. However, access to these investments may be subject to regulatory restrictions, meaning that many tokenized assets may only be available to accredited investors.

We can see that well-known private equity giants Hamilton Lane and KKR have cooperated with Securitize respectively. By tokenizing the Feeder Fund of the private equity funds they manage, they provide investors with a cheap way to participate in top private equity funds. The minimum investment threshold has been greatly reduced from an average of US$5 million to only US$20,000. However, individual investors still need to pass the qualified investor verification of the Securitize platform, and there is still a certain threshold.

(RWA 10,000-word research report: The value , exploration and practice of fund tokenization )

2.3 Save operating costs

Asset programmability can be another source of cost savings, especially for asset classes whose servicing or issuance is often highly manual, error-prone, and involves numerous intermediaries, such as corporate bonds and other fixed-income products. These products often involve custom structures, imprecise interest calculations, and coupon payment outlays. Embedding operations such as interest calculations and coupon payments into smart contracts on tokens will automate these functions, significantly reducing costs; system automation through smart contracts can also reduce the cost of services such as securities lending and repo transactions.

The Bank for International Settlements (BIS) and the Hong Kong Monetary Authority launched the Evergreen project in 2022 to issue green bonds using tokenization and a unified ledger. The project makes full use of the distributed unified ledger to integrate the participants involved in bond issuance on the same data platform, supports multi-party workflows, and provides specific participant authorization, real-time verification and signing functions, which improves transaction processing efficiency. The bond settlement realizes DvP settlement, reduces settlement delays and settlement risks, and the platforms real-time data updates of participants also improve transaction transparency.

(https://www.hkma.gov.hk/media/eng/doc/key-information/pr ess-release/2023/20230824 c 3a 1.pdf)

Over time, tokenized asset programmability can also create benefits at the portfolio level, enabling asset managers to automatically rebalance portfolios in real time.

2.4 Enhance compliance, auditability and transparency

Current compliance systems often rely on manual checks and retroactive analysis. Asset issuers can automate these compliance checks by embedding specific compliance-related actions (e.g., transfer restrictions) into tokenized assets. In addition, the 24/7 data availability of blockchain-based systems creates opportunities for simplified consolidated reporting, immutable record keeping, and real-time auditability.

(Tokenization and unified ledger - blueprint for building a future monetary system)

An intuitive case is Carbon Credits. Blockchain technology can provide an immutable and transparent record of credit purchase, transfer and exit, and build transfer restrictions and measurement, reporting and verification (MRV) functions into the smart contract of the token. In this way, when a carbon token transaction is initiated, the token can automatically check the latest satellite imagery to ensure that the energy-saving and emission-reduction project underlying the token is still in operation, thereby enhancing trust in the project and its ecosystem.

2.5 Cheaper and more flexible infrastructure

Blockchain is open source in nature, and is continually evolving with thousands of Web3 developers and billions of dollars in venture capital. Assuming financial institutions choose to operate directly on public permissionless blockchains, or public/private hybrid blockchains, innovations in these blockchain technologies (such as smart contracts and token standards) can be easily and quickly adopted, further reducing operating costs.

(Tokenization: A digital-as set déjà vu)

Given these advantages, it’s easy to see why many large banks and asset managers are so interested in the prospects of this technology.

However, some of the listed advantages remain theoretical at present due to the lack of use cases and adoption of tokenized assets.

Challenges of Mass Adoption

Despite the potential benefits of tokenization, few assets have been tokenized at scale to date. Potential factors include:

3.1 Inadequate technical and infrastructure preparation

The adoption of tokenization is hampered by the limitations of existing blockchain infrastructure. These limitations include a continued shortage of institutional-grade digital asset custody and wallet solutions that do not provide sufficient flexibility to manage account policies, such as transaction limits.

Additionally, blockchain technology, especially permissionless public blockchains, has limited ability to operate the system properly at high transaction throughput, a limitation that prevents it from supporting tokenization for certain use cases, especially in mature capital markets.

Finally, decentralized private blockchain infrastructure (including developer tools, token standards, and smart contract guidelines) brings risks and challenges to interoperability between traditional financial institutions, such as interoperability between chains, cross-chain protocols, liquidity management, etc.

3.2 Current business cases are limited and implementation costs are high

Many of the potential economic benefits of tokenization will only be realized at scale when tokenized assets reach a certain scale. However, this may require an education cycle to transition and adapt to mid- and back-office workflows that were not designed for tokenized assets. This situation means that short-term benefits are unclear and business cases are difficult to gain organizational buy-in.

Not everyone will be able to master digital currency and blockchain technology at the beginning, and operations during the transition period will be complicated and may involve running two systems at the same time (for example, digital and traditional settlement, on-chain and off-chain data coordination and compliance, digital and traditional custody and asset services).

Finally, many traditional clients in the capital markets have not yet shown interest in the infrastructure and liquidity of value that is available 24/7, which poses further challenges to the way tokenized products are brought to market.

3.3 Market supporting facilities need to mature

Tokenization requires instant cash settlement for faster settlement times and greater capital efficiency. However, despite progress in this area, there is currently no large-scale cross-bank solution: tokenized deposits are currently only piloted within a few banks, and stablecoins currently lack regulatory clarity and cannot be treated as bearer assets to provide real-time ubiquitous settlement. Secondly, tokenization service providers are currently in their infancy and are not yet able to provide comprehensive and mature one-stop services. In addition, the market lacks large-scale distribution channels for appropriate investors to access digital assets, which is in stark contrast to the mature distribution channels used by wealth and asset managers.

3.4 Regulatory uncertainty

To date, regulatory frameworks for tokenization vary by region or simply do not exist. Challenges facing U.S. participants in particular include unclear settlement finality, the lack of legal binding force of smart contracts, and unclear requirements for qualified custodians. Further unknowns remain regarding the capital treatment of digital assets. For example, the U.S. Securities and Exchange Commission has stated through Regulation SAB 121 that digital assets must be reflected on the balance sheet when providing custody services - a standard that is more stringent than for traditional assets, making it costly for banks to hold or even distribute digital assets.

3.5 Industry needs coordination

Capital market infrastructure participants have not yet shown a unanimous willingness to build tokenized markets or move markets to the chain, and their participation is crucial because they are the ultimate recognized holders of assets on the ledger. The motivation to move to new infrastructure on the chain through tokenization is not consistent, especially considering that the functions of many financial intermediaries will undergo significant changes or even be disintermediated.

Even carbon credits, as a relatively new asset class, have faced challenges in their early days of being established and operational on blockchains. Despite the obvious benefits of tokenization, such as increased transparency, Gold Standard currently appears to be the only registry that publicly supports tokenized carbon credits.

4. The first wave of tokenization has arrived

Despite the many challenges mentioned above, as well as the unknown unknowns, we can see from the trends and mass adoption in recent months that tokenization has reached a turning point in certain asset classes and their use cases, and the first wave of tokenization has arrived (Tokenization in Waves).

4.1 Massive adoption of stablecoins

Tokenized assets with 24/7 instant settlement must be supported by tokenized cash, and the representative of tokenized cash - stablecoin, is the most important part of the tokenized market.

Stablecoin definition: Most digital currencies have large price fluctuations and are not suitable for payments, just like Bitcoin can fluctuate greatly in a day. Stablecoins are digital currencies that aim to solve this problem by maintaining a stable value, usually pegged 1:1 to a fiat currency such as the US dollar. Stablecoins have the best of both worlds: they maintain low daily volatility while providing the advantages of blockchain - efficient, economical and globally applicable.

According to SoSoValue data, there is currently about $153 billion in tokenized cash in circulation in the form of stablecoins (such as USDC, USDT). Some banks have launched or are about to launch tokenized deposit functions to improve the cash settlement link of commercial transactions. These nascent systems are by no means perfect; liquidity is still fragmented, and stablecoins have not yet been recognized as bearer assets. Even so, they have proven sufficient to support meaningful trading volumes in the digital asset market. Stablecoin on-chain transaction volume typically exceeds $500 billion per month.

(https://soso value.xyz/dashboard/Stablecoin_Total_Market_Cap)

4.2 Tokenized U.S. Treasury Bonds for Short-term Commercial Purposes

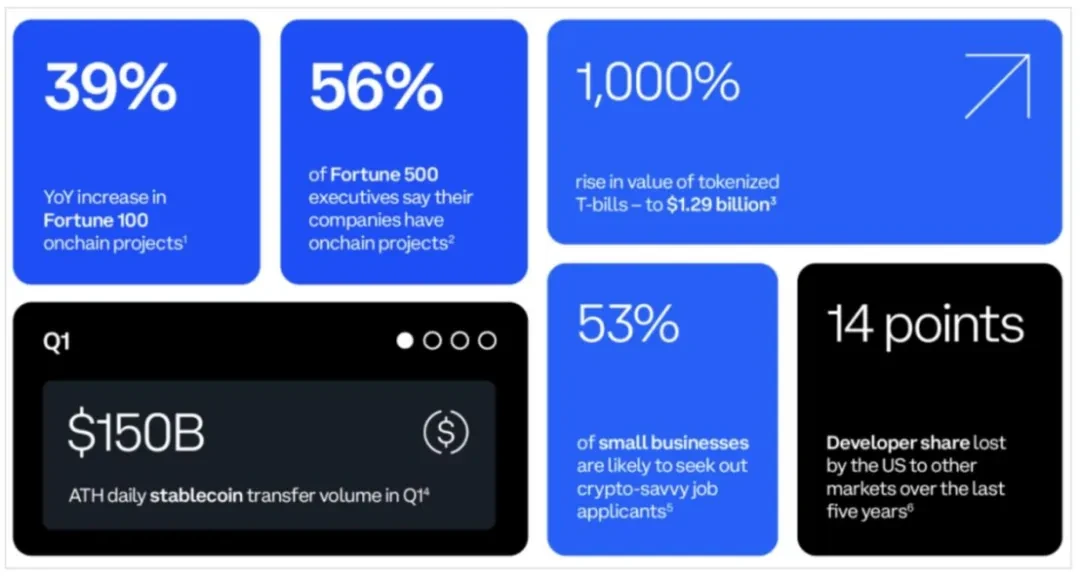

The current high interest rate environment has attracted much attention from the market for tokenized use cases based on US Treasuries, and its products can indeed achieve economic benefits and improve capital efficiency. According to RWA.XYZ data, the market size of tokenized US Treasuries has increased from US$770 million at the beginning of 2024 to US$1.75 billion today (as of July 1), an increase of 227%.

(https://app.rwa.xyz/travels )

At the same time, short-term liquidity transactions such as tokenized repo and securities lending are more attractive when interest rates rise. JPMorgan Chases institutional-level blockchain payment network Onyx is currently able to process $2 billion in transactions per day. Onyxs transaction volume can be attributed to JPMorgan Chases Coin System and Digital Asset solutions.

Additionally, in the U.S., traditional banks have onboarded a number of large (and often lucrative) digital asset businesses, such as stablecoin issuers. Retaining these customers requires 24/7 flow of value and tokenized cash, further bolstering the business case for accelerated tokenization capabilities.

4.3 The gradual clarification of the regulatory framework for tokenization

At the end of June, the European Union has implemented the regulatory requirements for stablecoins in the Crypto Asset Market Regulation Act (MiCA), while Hong Kong is also seeking opinions on the implementation of stablecoins. Other regions such as Japan, Singapore, the UAE and the UK have also issued new guidelines to increase regulatory transparency for digital assets. Even in the United States, market participants are exploring various tokenization and distribution methods, using existing rules and guidance to mitigate the impact of current regulatory uncertainty.

Following the hearing of the House Digital Assets, Financial Technology and Inclusion Subcommittee on June 7 on Next Generation Infrastructure: How to Promote Efficient Market Operations by Tokenizing Real-World Assets?, on June 14, SEC Commissioner Mark Uyeda emphasized the potential of tokenization to change the capital market at a securities market event. Especially with the advancement of the important issue of digital currency in the process of the US election, whether it is the demand for financial innovation or the relaxation of supervision, the focus of traditional financial capital on digital currency has shifted from the previous passive speculation to how to actively transform traditional finance.

4.4 Market penetration and infrastructure maturity

Over the past five years, many traditional financial services firms have added digital asset talent and capabilities. Several banks, asset managers, and capital markets infrastructure firms have built digital asset teams of 50 or more people, and these teams are growing. At the same time, established market participants are gaining a greater understanding of the technology and its promise.

(Coinbase, The State of Crypto: The Fortune 500 Moving Onchain)

According to Coinbase’s Q2 State of Cryptocurrency report, 35% of Fortune 500 companies are considering launching tokenization projects. Executives at 7 of the top 10 Fortune 500 companies are learning more about stablecoin use cases, primarily for low-cost, real-time settlement of stablecoin payments. 86% of Fortune 500 executives recognize the potential benefits of asset tokenization for their companies, and 35% of Fortune 500 executives say they are currently planning to launch tokenization projects (including stablecoins).

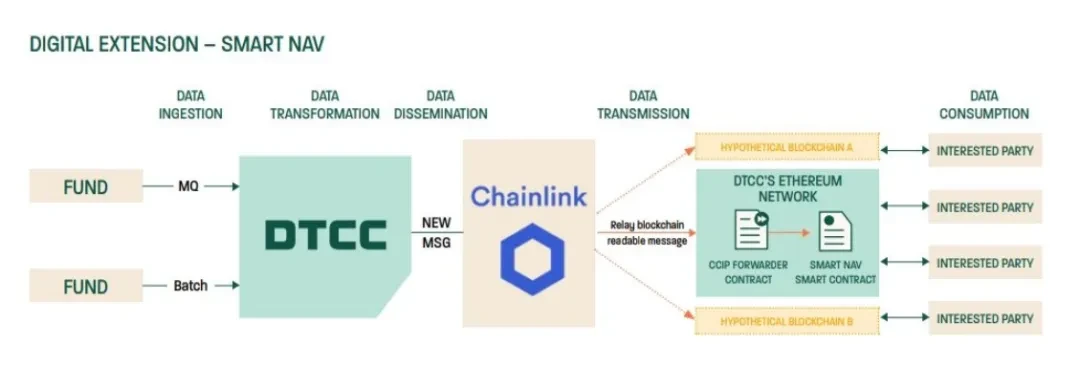

In addition, we are currently seeing more experiments and planned functionality expansions at some important financial market infrastructures. For example, on May 16, the Depository Trust Clearing Corporation (DTCC), the world’s largest securities settlement system that processes more than $200 trillion in transactions each year, and blockchain oracle Chainlink completed the pilot Smart NAV project. The project used Chainlink’s cross-chain interoperability protocol CCIP to enable the introduction of mutual fund net asset value (NAV) quote data on almost all private or public blockchains.

Market participants in the pilot included American Century Investments, Bank of New York Mellon, Edward Jones, Franklin Templeton, Invesco, JPMorgan Chase, MFS Investment Management, Mid-Atlantic Trust, State Street and Bank of America. The pilot found that by providing structured data on the chain and creating standard roles and processes, the underlying data can be embedded in a variety of on-chain use cases, opening up a variety of innovative application scenarios for the tokenization of funds.

(DTCC, Smart NAV Pilot Report: Bringing Trusted Data to the Blockchain Ecosystem)

While tokenization has yet to reach the scale needed to realize all of its benefits, the ecosystem is maturing, the underlying challenges are becoming clearer, and the business cases for adopting tokenization are gradually increasing.

In particular, the argument that tokenization can improve capital efficiency in the current high interest rate environment has been strongly supported by the successful launch of tokenized funds by Blackrock (from a traditional financial perspective), the large-scale adoption of Ondo Finances tokenized U.S. debt products (from a crypto financial perspective), and the popularity of $ONDO tokens. It can be said that the first wave of tokenization has arrived.

As for the argument that tokenization can provide liquidity for traditional illiquid assets, it remains to be further proven by the market. This argument will be built on the large-scale adoption of tokenized assets.

Regardless, these real-world use cases demonstrate that tokenization can continue to gain traction and create meaningful positive value for global markets over the next two to five years.

5. Most widely adopted asset classes

Asset classes with large market size, high value chain friction, less mature traditional infrastructure, or low liquidity may be most likely to gain huge benefits from tokenization. However, being most likely to profit does not mean being the first to land.

The rate and timing of tokenization adoption will depend on the nature of the asset class, with different expected returns, feasibility, timing of impact, and risk appetite of market participants. These factors will determine if and when the relevant asset class can achieve mass adoption.

Specific asset classes can lay the foundation for the subsequent adoption of other asset classes by introducing clearer regulation, more mature infrastructure, better interoperability, and faster and more convenient investment. Adoption will also vary by region and be influenced by the dynamic and changing macro environment, including market conditions, regulatory frameworks, and buyer demand. Finally, the success or failure of star projects may drive or limit the further adoption of tokenization.

(Tokenization and unified ledger - blueprint for building a future monetary system)

5.1 Mutual Funds

Tokenized money market funds have attracted more than $1 billion in assets under management, indicating that in a high-interest environment, investors with on-chain capital have a large demand for tokenized money market funds. Investors can choose funds managed by established companies such as Blackrock, WisdomTree, Franklin Templeton, and Web3 native projects such as Ondo Finance, Superstate, and Maple Finance. The underlying assets of these tokenized money market funds are basically U.S. Treasuries.

This is the first wave of tokenization at present, namely the mass adoption of tokenized funds, and as the scope and scale of tokenized funds continue to expand, additional related products and operational advantages will be realized.

As Paypal said when it launched its stablecoin on Solana at the end of May: the first step towards mass adoption is cognitive awakening - that is, simply introducing people to the fact that new technology exists; the next step in adopting new payment technology is to achieve utility, that is, to transform the initial cognitive awakening of ideas into utility in real life. The idea of Paypal promoting its stablecoin can also be used in the mass adoption of the tokenized market.

(Analysis of the internal logic of PayPal stablecoin payment and the evolutionary thinking towards Mass Adoption)

The transition to on-chain tokenized funds can significantly improve the utility of funds, including instant 24/7 execution, instant settlement, using tokenized fund shares as payment instruments, etc. In addition, based on the composability of the chain, Web3 native project issuers are improving the utility of tokens based on their own characteristics. For example, Superstate, the team behind $USTB (initiated by the founder of Compound), announced that their tokens can now be used to collateralize transactions on FalconX. Ondo Finance, the team behind $USDY and $OUSG, announced that $USDY can now be used to collateralize perpetual contract transactions on Drift Protocol.

Furthermore, through the composability of hundreds of tokenized assets, highly customized investment strategies will become possible. Putting data on a shared ledger reduces errors associated with manual reconciliation and increases transparency, thereby reducing operational and technical costs.

While the overall demand for tokenized money market funds will depend in part on the interest rate environment, it undoubtedly plays a vital role in driving the development of the tokenized market. Other types of mutual funds and ETFs can also provide on-chain capital diversification for traditional financial instruments.

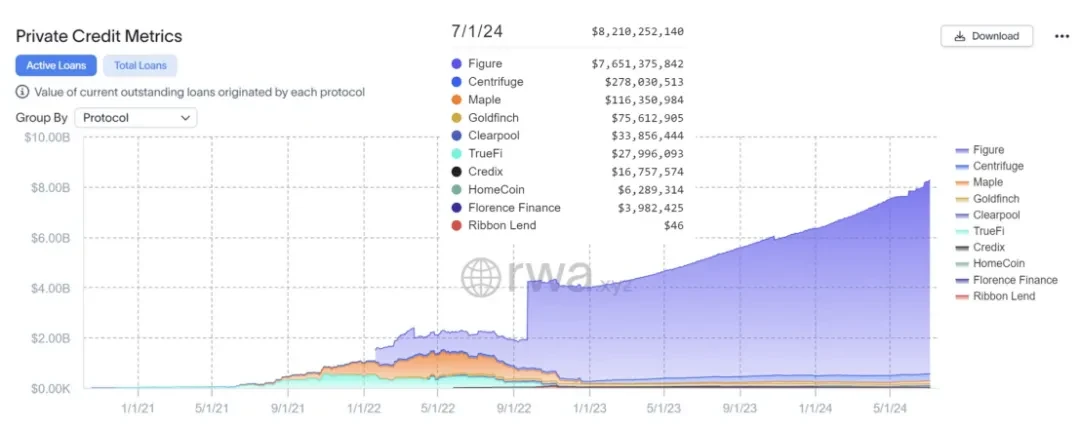

5.2 Private Credit

While blockchain-based private lending is still in its infancy, disruptors are already starting to succeed in this space: Figure Technologies is one of the largest non-bank home equity lines of credit (HELOC) lenders in the U.S., with billions of dollars in loan originations. Web3 native projects like Centrifuge and Maple Finance, along with companies like Figure, have facilitated over $10 billion in on-chain credit originations.

(https://app.rwa.xyz/private_credit )

The traditional credit industry is a process-intensive, labor-intensive industry with high levels of intermediary involvement and high barriers to entry. Blockchain-based credit offers an alternative with many advantages: Real-time on-chain data, stored in a unified general ledger, serves as a single source of truth, promoting transparency and standardization throughout the loan lifecycle. Smart contract-based payout calculations and simplified reporting reduce the costs and labor required. Shortened settlement cycles and access to a wider pool of funds speed up the transaction process and potentially reduce borrowers funding costs.

Most importantly, global liquidity can provide funds for on-chain credit without permission. In the future, tokenizing the borrowers financial metadata or monitoring their on-chain cash flow can achieve fully automated, fairer and more accurate financing for projects. Therefore, more and more loans are turning to private credit channels, and financing cost savings and fast and efficient financing are extremely attractive to borrowers.

The non-standardized business of private credit may have greater potential for explosive growth, and Securitize CEO also clearly expressed his optimism about the development of the tokenized private credit industry.

5.3 Bonds

In the past decade, tokenized bonds with a total notional value of over $10 billion have been issued globally (out of $140 trillion in notional bonds outstanding globally). Recent notable issuers include Siemens, City of Lugano, and the World Bank, as well as other companies, government-related entities, and international organizations. In addition, blockchain-based repurchase (Repo) transactions have been adopted, with monthly volumes in North America reaching trillions of dollars, creating value through operational and capital efficiencies in existing funding flows.

Digital bond issuance is likely to continue because of the high potential returns once scaled up and the relatively low barriers to entry at present, partly due to a desire to stimulate the development of capital markets in certain regions. For example, in Thailand and the Philippines, issuing tokenized bonds has enabled small investors to participate through decentralization.

While the benefits to date have been primarily on the issuance side, an end-to-end tokenized bond lifecycle could improve operational efficiency by at least 40% through data clarity, automation, embedded compliance (e.g., transferability rules are coded into the token), and streamlined processes (e.g., asset intermediation services). In addition, lower costs, faster issuance, or asset fragmentation could improve financing for smaller issuers by enabling “instant” funding (i.e., optimizing borrowing costs by raising a specific amount at a specific time) and tapping into global capital pools to expand the investor base.

5.4 Repurchase Transactions

Repurchase agreements (Repo) are an example of where tokenization adoption and its benefits can be observed today. Broadridge Financial Solutions, Goldman Sachs, and JPMorgan Chase currently trade trillions of dollars in Repo volume per month. Unlike some tokenization use cases, Repo transactions do not require the entire value chain to be tokenized to realize real benefits.

Financial institutions that tokenize repo primarily achieve operational and capital efficiency. On the operational side, supporting the execution of smart contracts automates daily lifecycle management (e.g., collateral valuation and margin replenishment), which reduces system errors and settlement failures and simplifies reporting. On the capital efficiency level, 24/7 instant settlement and real-time analysis of on-chain data can improve capital efficiency by meeting intraday liquidity requirements through short-term lending while enhancing collateral.

Historically, most repurchase agreements have maturities of 24 hours or longer. Intraday liquidity can reduce counterparty risk, lower borrowing costs, enable short-term incremental lending, and reduce liquidity buffers.

Real-time, around-the-clock, cross-jurisdictional collateral flows can provide access to higher-yielding, high-quality liquid assets and enable the optimized flow of this collateral between market participants, maximizing its availability.

6. After the First Wave of Tokenization

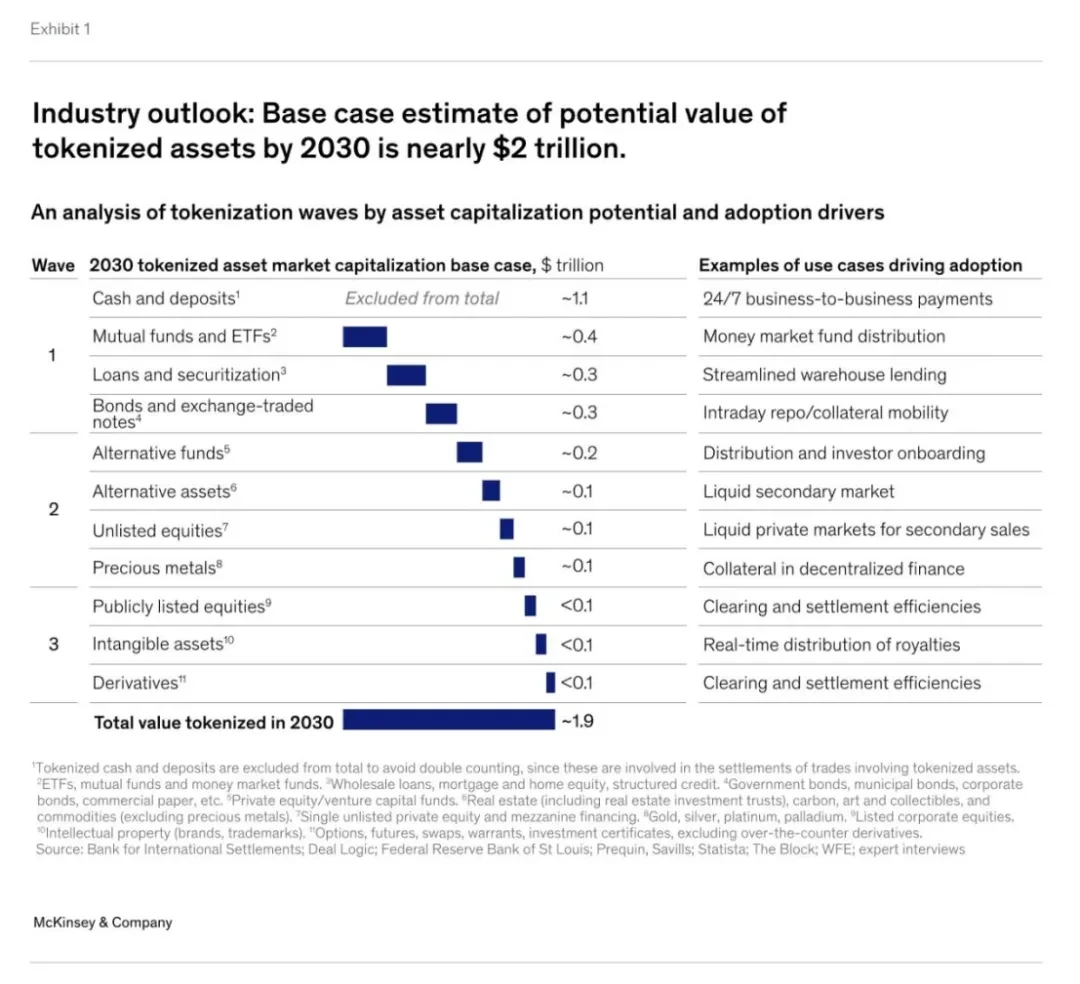

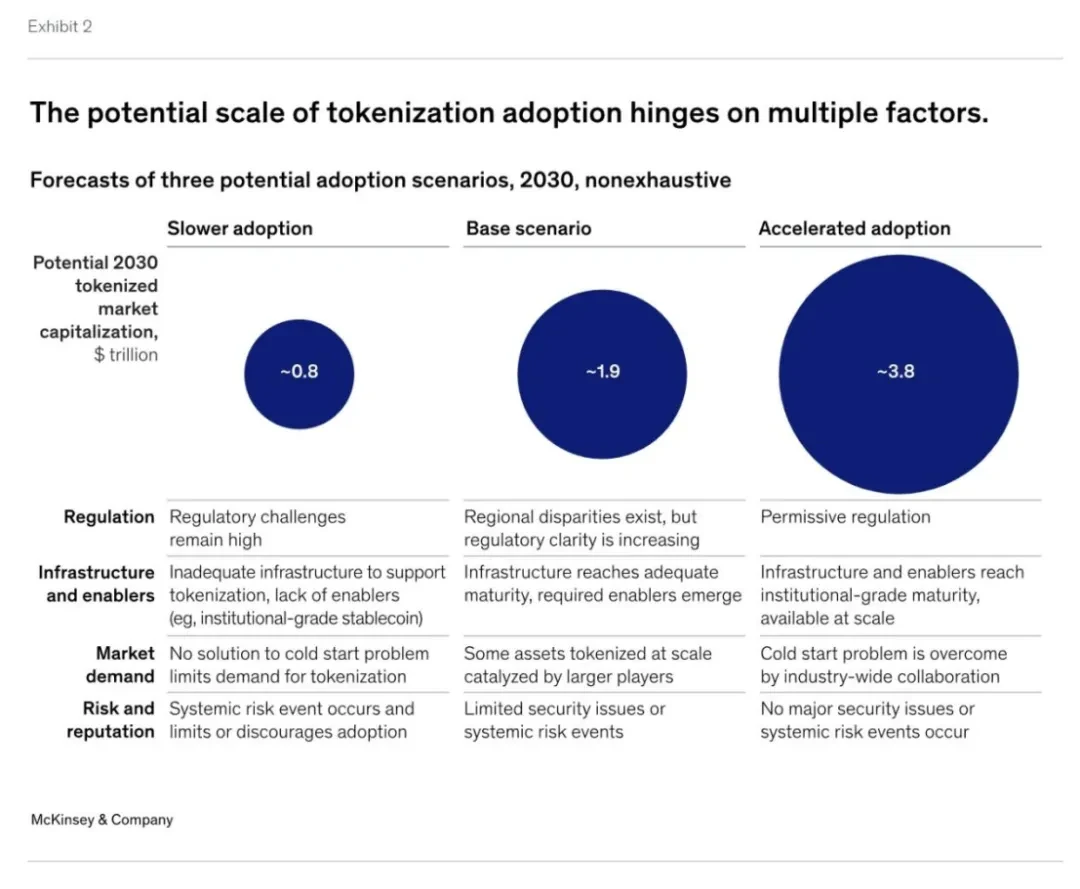

The tokenization market is currently advancing steadily and is expected to accelerate as network effects strengthen. Due to their characteristics, some asset classes may enter the realistic mass adoption stage faster, with tokenized assets exceeding $100 billion by 2030.

McKinsey expects that the first asset classes that can be realized will include cash and deposits, bonds, mutual funds, ETFs, and private credit. For cash and deposits (stable currency use cases), the adoption rate is already high, thanks to the high efficiency and value gains brought by blockchain, as well as higher technical and regulatory feasibility.

McKinsey estimates that by 2030, the tokenized market capitalization of all asset classes could reach approximately $2 trillion, with pessimistic and optimistic scenarios ranging from approximately $1 trillion to approximately $4 trillion, respectively, driven primarily by the following assets. This estimate does not include stablecoins, tokenized deposits, and central bank digital currencies (CBDCs).

(From ripples to waves: The transformational power of tokenizing assets)

Previously, Citigroup also predicted in its Money, Tokens and Games (Blockchains Next Billion Users and Trillion Value) research report that in addition to tokenized cash, the tokenized market size will reach US$5 trillion by 2030.

(Citi RWA Research Report: Money, Tokens and Games (Blockchains Next Billion Users and Trillion Value))

The first wave of tokenization described above has already accomplished its arduous task of mass market adoption, and the tokenization of other asset classes is more likely to scale only after the previous first wave of asset tokenization has laid the foundation or when a clear catalyst emerges.

For several other asset classes, adoption may be slower, either because the expected benefits are only incremental or because of feasibility issues, such as difficulty meeting compliance obligations or lack of incentives for key market participants. These asset classes include publicly traded and unlisted stocks, real estate, and precious metals.

(From ripples to waves: The transformational power of tokenizing assets)

VII. How should financial institutions respond?

Whether or not tokenization is at a tipping point, a natural question is how financial institutions should respond to this moment. The exact time frame and ultimate adoption of tokenization is unclear, but early institutional experiments with certain asset classes and use cases (e.g., money market funds, repo, private equity, corporate bonds) suggest that tokenization has the potential to scale in the next two to five years. Those looking to ensure a leading position in this ecosystem can consider the following steps.

7.1 Revisiting the basic business case

Institutions should reassess the specific benefits and value proposition of tokenization, as well as the implementation path and costs. Understanding the impact of higher interest rates and volatile public markets on specific assets or use cases is critical to properly assessing the potential benefits of tokenization. Likewise, continually exploring the provider landscape and understanding early applications of tokenization will help refine estimates of the costs and benefits of the technology.

7.2 Building technical and risk capabilities

Regardless of where existing institutions are in the tokenization value chain, they will inevitably need to reserve knowledge and capabilities to meet the new wave. The first and most important thing is to establish a basic understanding of tokenization technology and its associated risks, especially about blockchain infrastructure and governance responsibilities (who can approve what and when), token design (restrictions on assets and the enforcement of these restrictions) and system design (decisions on where books and records are stored and the impact on the nature of asset holders). Understanding these basic principles can also help to stay proactive in subsequent communications with regulators and customers.

7.3 Building ecosystem resources

Given the relatively fragmented nature of the current digital world, institutional leaders must develop an ecosystem strategy in order to integrate it with other (legacy) systems and partners to maintain their advantage.

7.4 Participation in Standards Development

Finally, organizations looking to take a leading role in the tokenization space should maintain a dialogue with regulators to provide input on emerging standards. Some examples of key areas where standards could be considered include controls (i.e., appropriate governance, risk, and control frameworks to protect end investors), custody (what constitutes qualified custody of tokenized assets on private networks, when to use digital twins vs. digital native records, what is a good position of control), token design (what types of token standards and associated compliance engines are supported), and blockchain support and data standards (what data is kept on-chain vs. off-chain, reconciliation standards).

8. The Way Forward

Comparing the current state of the tokenization market to major paradigm shifts in other technologies shows that we are in the early stages of the market. Consumer technologies (such as the Internet, smartphones, and social media) and financial innovations (such as credit cards and ETFs) typically show the fastest growth (over 100% per year) within the first five years of their birth. After that, we see annual growth slowing to around 50%, and ultimately achieving more modest compound annual growth rates of 10% to 15% after more than a decade.

Although tokenization experiments began as early as 2017, it is only in recent years that a large number of tokenized assets have been issued. According to McKinsey’s estimate of the tokenization market in 2030, it assumes an average compound annual growth rate of 75% for all asset classes, with asset classes that emerged in the first wave of tokenization taking the lead.

Although it is reasonable to expect that tokenization will drive the transformation of the financial industry in the coming decades, and mainstream financial institutions in the market are already actively participating in the layout, such as Blackrock, Franklin Templeton, and JPMorgan Chase, more institutions are still in a wait-and-see mode, waiting for clearer market signals.

We believe that the tokenization market is at a tipping point and that tokenization will accelerate once we see some important signs, including:

Infrastructure: Blockchain technology can support trillions of dollars in transaction volume;

Integration: Blockchain is used for seamless interconnection of different applications;

Enablers: Widespread availability of tokenized cash (e.g., CBDCs, stablecoins, tokenized deposits) for instant settlement of transactions;

Demand: Buy-side participants’ interest in investing in on-chain investment products at scale;

Regulation: Actions that provide certainty and support a fairer, more transparent, and more efficient financial system across jurisdictions, with clarity on data access and security.

While we have to wait for more catalysts to emerge, we expect the wave of mass adoption to follow the first wave of tokenization described above. This will be led by financial institutions and market infrastructure players, who will collectively capture market value and establish a leading position.