Original article by: Marco Manoppo

Compiled by Odaily Planet Daily ( @OdailyChina )

Translated by Azuma ( @azuma_eth )

Editors note: Primitive Ventures investor Marco Manoppo has been quite prolific recently. After his article last week about how he missed out on Virtuals (see VCs Self-Report: How I Missed the Opportunity to Make Hundred-fold Profits from Virtuals ) became a hit, Manoppo published another new article today.

In the article, Manoppo outlined the potential impact of passive investment funds on Bitcoin buying as Bitcoin gradually approaches traditional finance, especially after MicroStrategy (stock code: MSTR) officially joined the Nasdaq 100 Index. Based on this background, Manoppo said that despite the recent pullback in the cryptocurrency market and the current price discovery range, he is more optimistic about Bitcoin than ever.

The following is the full text of Manoppo, translated by Odaily Planet Daily.

After eight weeks of gains, the cryptocurrency market is finally seeing some pullback. Even though we are now in price discovery territory, I am more bullish on Bitcoin than ever before. The reason is simple: Bitcoin, as an asset class, is now entering the TradFi (3, 3) regime.

The growth of passive funds

To understand what the TradFi (3, 3) system is, it is necessary to assess the growth of passive funds in investing. In simple terms, a passive fund is an investment product whose goal is to track and replicate the performance of a specific market index or market segment, rather than trying to outperform it. They follow a set of rules and methodologies that cater to their target market and desired risk profile.

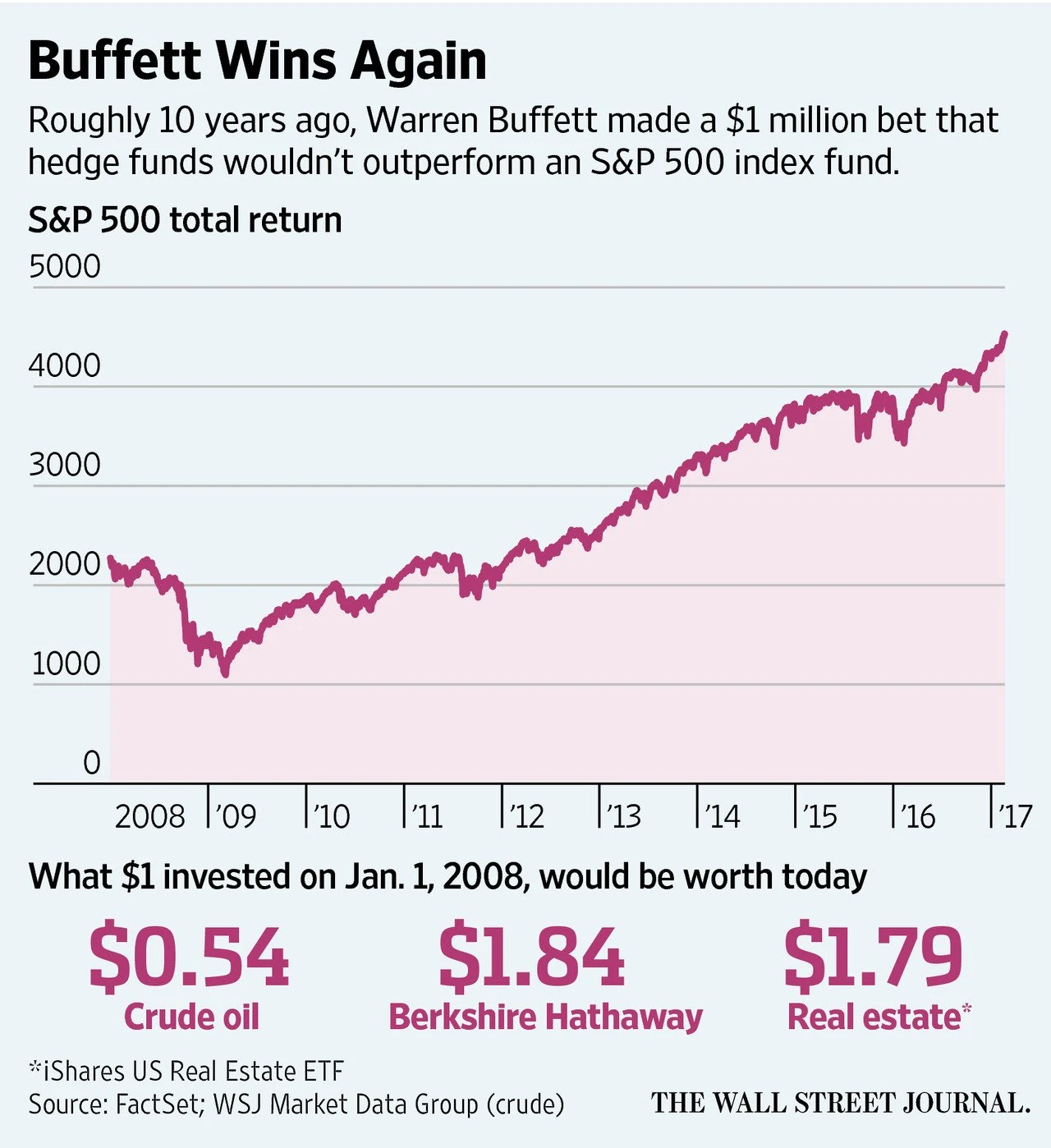

SPY (SPDR SP 500 ETF Trust) and VTI (Vanguard Total Stock Market ETF) are well-known passive funds. Most investment enthusiasts probably remember that Buffett once bet with a hedge fund manager that the SP 500 index would outperform most active fund managers - Buffett has been proven right. Since 2009, passive funds have been performing strongly and have become the preferred investment method for most people.

It would take a long article to delve into all the intricacies of the factors driving the growth of passive funds, but we can boil it down to a few simple factors:

Better cost-effectiveness

Passive funds, such as index funds and ETFs, typically have much lower expense ratios than actively managed funds. This is because they do not require a lot of active work from the fund manager. Once the rules and methodology are in place, the algorithms take over, with only some human intervention during quarterly rebalancing. Lower costs generally mean better net returns on investment, which makes passive funds more attractive to those more cost-conscious investors.

Lower access threshold, wider distribution

In short, passive funds are more accessible. Investors don’t have to go through the hassle of screening fund managers compared to active funds, and there’s a well-established industry around distributing financial products to your grandparents. Passive funds also tend to fit more easily into the financial supply chain for regulatory reasons. Most active funds are limited in their distribution materials, while passive funds are already well integrated into 401k plans, pension systems, and so on.

More stable performance

The wisdom of crowds usually leads to better results. Most active fund managers have failed to outperform their benchmarks over the past 15 years. While you may never get a 10x return from passive funds like you would have if you bought Tesla or Shopify in the early days, most people are not willing to bet 50% of their net worth on a single stock. High risk, high return is not always attractive.

Here are some more interesting statistics:

In the United States, assets in passive funds have grown fourfold over the past decade, from $3.2 trillion at the end of 2013 to $15 trillion by the end of 2023.

As of December 2023, passive funds’ total assets under management (AUM) in the United States officially exceeded active funds for the first time in history.

As of October 2024, U.S. stock index funds held $13.13 trillion in global assets, of which $10.98 trillion were in the U.S., while actively managed stock funds held $9.78 trillion in global assets, of which $7.26 trillion were in the U.S.

Index funds now account for 57% of U.S. stock fund assets, up from 36% in 2016.

In the first ten months of 2024, U.S. stock index funds saw inflows of $415.4 billion, while actively managed funds saw outflows of $341.5 billion during the same period.

This is why the entire traditional financial sector or cryptocurrency fund managers with experience in traditional finance are so enthusiastic about the Bitcoin ETF narrative. Because they know that this is the starting point to open a larger floodgate that will truly introduce Bitcoin into the retirement portfolio of ordinary people.

Cryptocurrency investment products

But what is the relationship between Bitcoin ETFs and passive funds?

Although the three major index providers (SP, FTSE, MSCI) have been working tirelessly to develop cryptocurrency indexes, the adoption rate has been quite slow and only single-asset crypto investment products are currently available. Of course, this is because these products are easier to launch, so everyone is scrambling to be the first to launch a Bitcoin ETF. Today, we are seeing major institutions working hard to promote ETH staking ETFs and more altcoin-based investment products.

However, the real killer product is an investment product that mixes Bitcoin. Imagine a portfolio consisting of 95% SP 500 and 5% Bitcoin, or 50% gold and 50% Bitcoin. Fund managers will be happy to promote this type of product - they are also easier to integrate into the financial supply chain, increasing its distribution channels.

However, it will take time to launch and promote these products, and given that they will be launched as a new product, they are not expected to automatically benefit from the monthly purchasing power of already popular passive products.

MSTR makes TradFi (3, 3) possible

Now its MicroStrategy ( MSTR)s turn.

With MSTR included in the Nasdaq 100, passive funds like QQQ (Invesco QQQ Trust, an ETF issued by Invesco that tracks the Nasdaq 100) will be forced to automatically buy MSTR, and MSTR in turn will be able to use these funds to buy more Bitcoin. In the future, there may be new Bitcoin-Equity-Gold hybrid passive investment products to replace MSTRs role, but in the foreseeable 3-5 years, MSTR as a Bitcoin Treasury Company is more likely to play this role because they are a mature US public company and are eligible to be included in the top passive fund indexes faster than newly launched passive investment products.

Therefore, as long as MSTR continues to use these funds to purchase more Bitcoin, buying of Bitcoin will continue to grow.

If this sounds too good to be true… that’s because there are a few minor issues that need to be addressed for MSTR to be more effective in this role. For example, since the SP 500 requires companies to have positive earnings in the most recent quarter and the past four quarters cumulatively, the likelihood of MSTR being included in the SP 500 is currently slim. However, new accounting rules that will be implemented starting in January 2025 will allow MSTR to report changes in the value of its BTC holdings as net income, potentially making MSTR eligible for inclusion in the SP 500.

This is essentially TradFis (3, 3) system.

5 Minutes of Quick Calculation and Assumptions

I did the following simple calculations in 5 minutes. If there are any errors in the calculations or suggestions for related assumptions, please feel free to correct me.

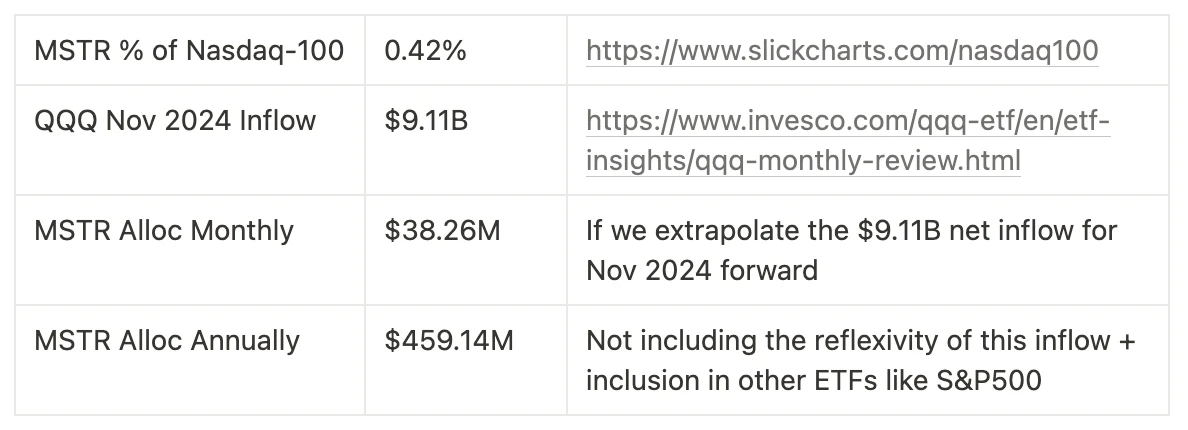

Odaily Note: Taking MSTRs share of 0.42% in the Nasdaq 100 Index as an example, QQQ will have a net inflow of US$9.11 billion in 2024, corresponding to a net inflow of US$38.26 million per month for MSTR and an annual inflow of US$459 million.

In short - the entire traditional financial passive investment ecosystem will unconsciously buy more Bitcoin because MicroStrategy (MSTR) is included in major indexes, just as they don’t realize they hold NVIDIA shares, creating an effect similar to (3, 3) for the price of Bitcoin.