Original author: donn

Original translation: TechFlow

I’m always interested in novel tokenomics. It’s always fascinating to see how crypto protocols align incentives, and sometimes they look very tempting — until they inevitably fall apart. So when Bittensor launched its dynamic $TAO (dTAO) system on Valentine’s Day, I was immediately intrigued.

The idea is simple: provide a new, more “fair” way to distribute TAO issuance between subnets.

But just one month later, problems emerged. It turns out that seemingly perfect designs don’t always work as expected in a free market.

How dTAO works

Here is a simplified review of how dTAO works:

Each subnet has its own subnet token ($SN), which exists in the form of a native TAO-SN Uni V2 type pool. Confusingly, although users are staking TAO in exchange for SN, this is actually no different from exchanging TAO for SN in terms of functionality. The only difference is that users cannot add liquidity to the liquidity pool or trade between subnet tokens directly (e.g. SN 1 → SN 2), but can use TAO as an intermediary (SN 1 → TAO → SN 2).

The issuance of TAO is allocated in proportion to the price of the subnet SN token. To smooth price fluctuations or prevent price manipulation, the system uses a moving average price.

The SN token itself also has a high issuance, with a supply cap of 21 million, similar to TAO and BTC. A portion of SN is allocated to the TAO-SN liquidity pool, and the rest is allocated to the subnet stakeholders (miners, validators, subnet owners). The amount of SN allocated to the TAO-SN pool is to balance the issuance of TAO in the pool, thereby keeping the price of SN (in TAO units) stable while increasing liquidity.

However, if the above calculation results show that the number of SNs required by the subnet exceeds the maximum issuance of SNs (based on the issuance curve of SNs), the issuance of SNs will be limited to the maximum value, and the price of SNs (in TAO units) will rise.

The core assumption of this mechanism is that subnets with higher market capitalization create more value for the Bittensor network, so they should receive more TAO issuance.

However, the reality is that the highest priced tokens in the crypto market are often those with the most attention, hype, Ponzi characteristics, and marketing resources. This is why L1 public chains and memecoins always have the highest relative valuations.

Although the starting point of the mechanism design is good, assuming that subnets that generate value by generating revenue will use part of the revenue to repurchase SN tokens, thereby pushing up prices and obtaining more TAO issuance, this idea is somewhat naive.

Subnets flooded with meme coins and out-of-control token economics

Prior to the launch of dTAO, I discussed with a number of crypto analysts the apparent flaws in the dTAO token economics — namely that higher market cap ≠ higher revenue or greater value creation.

But I didn’t expect that this theory would soon be verified in practice. The free market worked in a “wonderful” way.

Just before the upgrade, an anonymous person took over subnet 281 and turned it into a memecoin subnet called TAO Accumulation Corporation (LOL Subnet for short). This obviously has nothing to do with AI.

From the now deleted Github page:

Miners do not need to run any code, and validators score them based on the number of subnet tokens they hold. The more tokens a miner holds, the higher the issuance they receive.

What actually happens is: Speculators buy SN 28 tokens → SN 28 price rises → SN 28 gets more TAO issuance → If the issuance limit of the subnet token is exceeded, the SN 28 price continues to rise → The issuance of SN tokens is distributed proportionally to the miners holding SN → People buy more SN to get more TAO → The price rises further → The Ponzi cycle continues.

As a result, TAO issuance officially began to fund… memes! At one point, the SN 28 subnet even became the seventh-largest subnet by market cap.

But why did SN 28 fail to take over Bittensor? Centralization saved the day

In just a few days, the Opentensor Foundation used its root stake to run custom validator code, incentivizing people to sell SN 28 tokens, causing its price to plummet 98% in a few hours.

Source: Bittensor discord

SN 28 subnet tokens plummet 98% following Opentensor Foundation action

Essentially, the Opentensor Foundation acts as a centralized entity that prevents the free market from exploiting the dTAO mechanism. This centralized intervention is currently possible because we are in a slow transition period from the old TAO issuance mechanism to the new dTAO mechanism.

Transition from the old TAO mechanism to dTAO

TAO’s old mechanism allowed the 64 validators who staked the most TAO on SN 0 (the “root subnet”) to vote on who could receive TAO issuance.

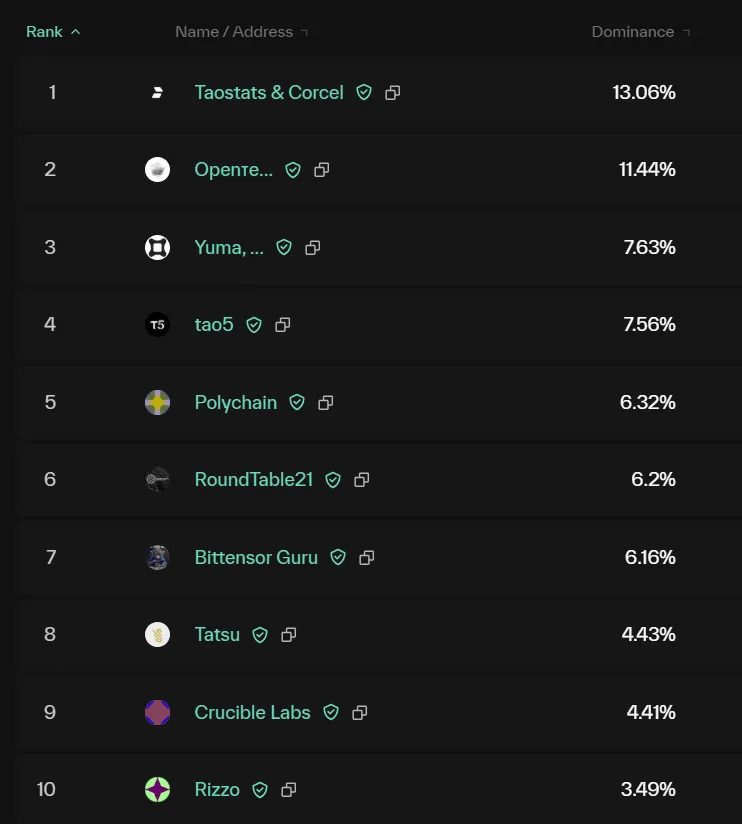

This mechanism itself raises a series of incentive issues brought about by the power held by large validators (such as Opentensor Foundation, DCG Yuma, Dao 5, Polychain, etc.). For example, in theory they can direct TAO issuance to subnets they have invested in or incubated, or to subnets where they run validator nodes and receive TAO rewards from them.

Top validators as shown on taostats.io/validators

Therefore, moving away from this mechanism is a good step towards decentralization. I applaud the team for choosing a more decentralized reward mechanism, even if it means they may lose some of their issuance.

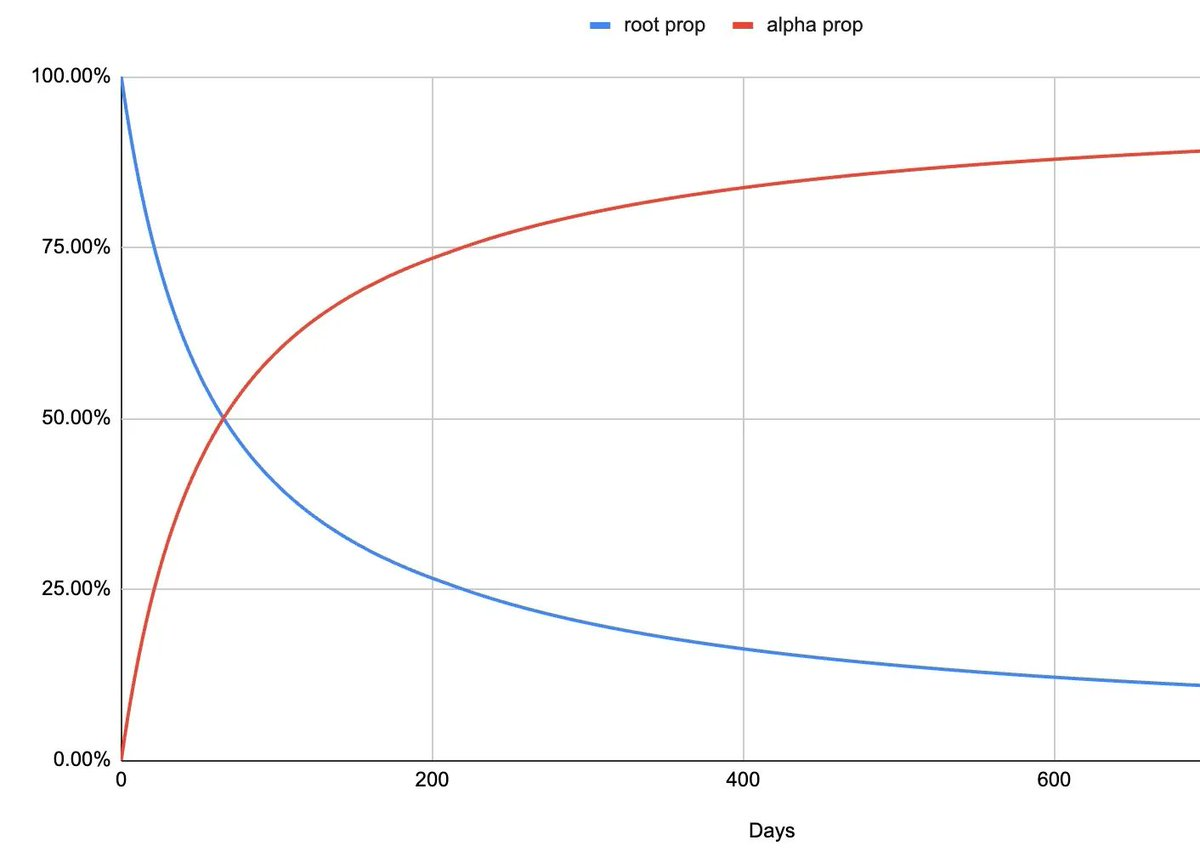

When the SN 28 incident occurred, dTAO had only been launched for about a week, so SN 0 (the blue line in the figure below) still controlled about 95% of the issuance, and the Opentensor Foundation was able to intervene.

However, after about a year, SN 0’s control over issuance will drop to about 20%. This means that if an event similar to SN 28 happens again, it will be almost impossible to intervene through SN 0. In this case, Bittensor may change from a “decentralized AI” project to an incentive network for meme coins.

During this transition period, the power to control emissions will be transferred from the old mechanism (SN 0 or “root property”) to the new dTAO mechanism (“alpha property”)

Admit it, this is more than just a meme

Even if we assume that people are rational enough in a bear market and don’t jump headfirst into meme coin hype, it’s possible that Bittensor will evolve into a general-purpose incentive network that has nothing to do with AI at all.

Imagine a thought experiment: someone launches a subnet dedicated to decentralized Bitcoin mining (although this is not a new idea). The goal of this subnet is to incentivize Bitcoin mining in a resource-efficient manner, while using the mined BTC as recurring income to repurchase the subnet token SN to obtain more TAO issuance.

Therefore, TAO has changed from a decentralized AI project to a general incentive project, and the issuance of TAO is only used to subsidize various random operating costs (OpEx) of enterprises, rather than moving towards a specific goal.

Technically, this is arguably in line with the original intention of the Yuma consensus mechanism, as Yuma consensus is designed to reach consensus around any subjective work, not necessarily limited to AI. However, this lack of a clear goal makes the entire system seem... meaningless.

Final Thoughts

Just one month into the dTAO model’s launch, cracks are already showing.

The incentives of the free market suggest that without any centralized power, Bittensor may no longer be an AI project, but rather an “attention network” dominated by memecoin subnets, or a “general incentive network” dominated by revenue-generating businesses that use TAO issuance to subsidize operating costs without substantially improving the Bittensor network.

I think the network needs a true objective function to unify the goals of all subnetworks. However, it is obviously very difficult to find a clear goal in the field of AI (especially general artificial intelligence, AGI) - as we have encountered various challenges in running a fair large language model (LLM) evaluation framework... This is also why Yuma consensus was created for subjective work.

As the famous quote goes, “Show me the incentives and I’ll tell you the results.”

Best wishes!

Remark

In the previous version, I mentioned that TAO issuance is proportional to market value, but it is actually proportional to price. This error has been corrected, thanks to @nick_hotz for correcting it.

Disclaimer

This article is for general information purposes only and does not constitute investment advice, nor is it a recommendation or solicitation to buy or sell any investment and should not be used as a basis for evaluating any investment decision. This article should not be considered accounting, legal or tax advice or investment advice. The article reflects the current views of the author and does not necessarily represent the views of the authors employer. The opinions expressed in this article may change without further update.