Original title: Type III Stablecoins

Original author: STANFORD BLOCKCHAIN CLUB

Compiled by Odaily Planet Daily Ethan ( @ethanzhang_web3 )

As a key component of the cryptocurrency field, stablecoins have a total market value of more than $200 billion in liquid assets, firmly occupying a core position in todays crypto market. Some people believe that the scale of stablecoins has been decoupled from the volatile crypto market - despite the correction in the crypto market in 2025, stablecoins still show strong resilience, and more and more traditional financial institutions are integrating decentralized finance (DeFi) into their solutions.

Currently, stablecoins have played two main functions: fiat currency settlement and value storage (SoV). The daily trading volume of stablecoins has reached an all-time high of $81 billion, and USDT and USDC account for more than 95% of the market share in mature economies and emerging markets. They represent not only simple transactions, but also financial inclusion and the demand for low-volatility currencies.

However, the acceptance of yield-based stablecoins is quite different from that of value storage. Despite the endless innovation in the DeFi field, yield-based stablecoins are still a niche application among stablecoins. The total market value of yield-based stablecoins is about 10% of the market value of USDT and USDC.

Why is there such a difference? More importantly, how can the status quo of yield-generating stablecoins be improved?

In this article, we will explore the evolution of yield-based stablecoins, analyze the execution mechanism of yield, and finally discuss how Cap solves the scalability and security issues.

The “coming of age ceremony” of income-generating stablecoins: the evolution from “surviving” to “making money”

In the early days, stablecoins’ earnings were mainly generated by endogenous mechanisms; earnings came entirely from DeFi platforms. Specifically, earnings were generated through liquidity provision and platform rewards, and the flow of funds formed a closed loop, with users constantly jumping from one protocol to another in order to speculate on higher annual interest rates. Therefore, the scale of earnings can only increase as the platform expands.

The most representative example is crypto over-collateralized stablecoins or collateralized debt positions (CDPs). The most typical example of CDP is the early MakerDAO, which minted DAI by using ETH as collateral. This model generates income by charging interest to borrowers who mint stablecoins using their collateral. The interest is then distributed to the participants of the protocol, and the entire mechanism operates entirely within the DeFi ecosystem. However, the scale of this model can only expand as the demand for ETH grows.

Another popular model relies on voting custody tokens (veTokens), locking these tokens allows the protocol to issue rewards to specific liquidity pools. This has led to so-called veToken wars in which stablecoin protocols compete for the ability to control liquidity pools to obtain rewards on decentralized exchanges (DEXs). These token wars, such as CRV and BAL, involve strategies that drive returns by purchasing DEX tokens.

While both models have billions of dollars in total locked value (TVL), their yields tend to be highly volatile and speculative. Most importantly, demand for these models is limited, especially when compared to applications outside of the DeFi mechanism, where demand is relatively small.

As a result, founders have been working industry-wide to push for the expansion of stablecoins to break through the limitations of the intrinsic yield model. With the rise of more synthetic dollar strategies backed by fiat or other assets, from T-Bills to hedge fund strategy experiments, stablecoins are beginning to try to solve the scalability problem of yield stablecoins.

So, what perspective should we use to view these new stablecoins?

The Game of Thrones of Stablecoins: Survival Rules for Three Types of Players

The core concept of yield stablecoins is just as the name suggests: reserves issue new currencies by lending highly liquid assets to execute investment strategies.

In addition to the choice of supported assets and lending parameters, the core difference of yield stablecoins lies in how they execute yield: who decides which strategies to implement? In the event of bankruptcy, how do users protect their rights?

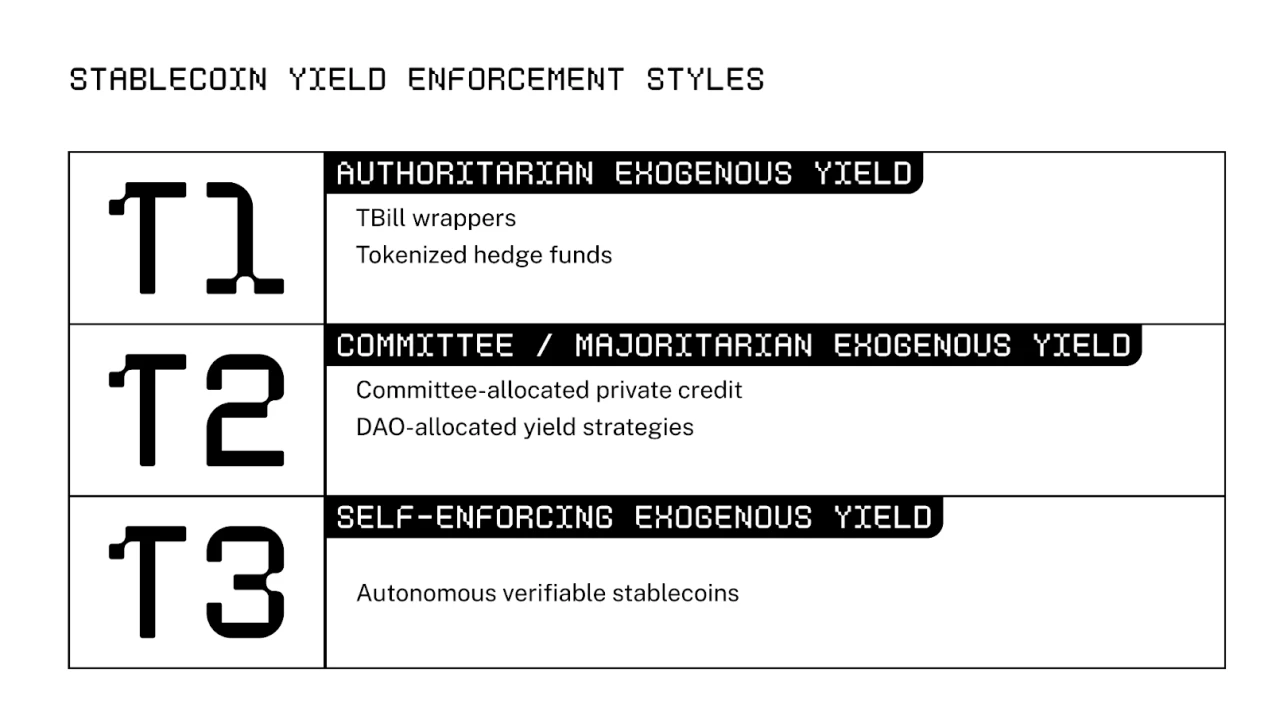

In other words, the framework against which execution mechanisms are evaluated is the capital allocation mechanism and security. Currently, there are two main types of execution in the DeFi space: authoritarian and committee. This article also introduces a third type - the self-reinforcing yield mechanism that the Cap team is pioneering.

The following sections will delve deeper into each stablecoin type, specifically capital allocation and security incentives, and the corresponding trade-offs.

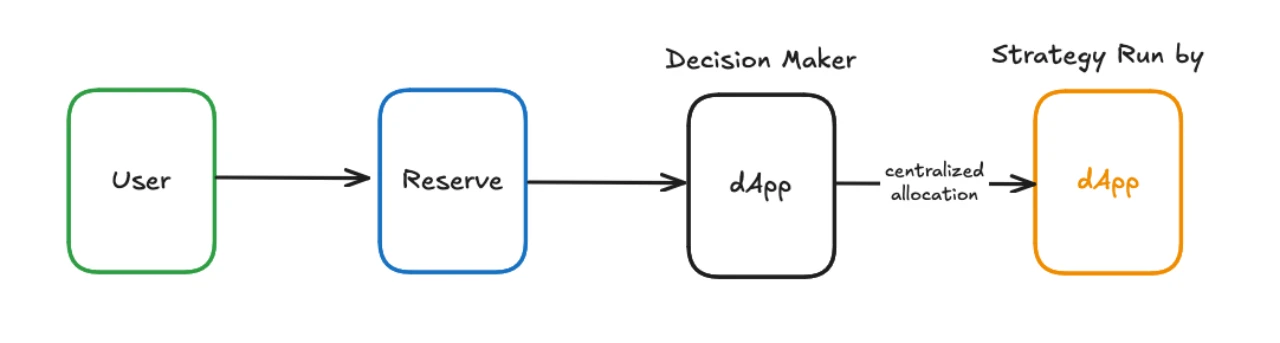

Category 1: The Dilemma of the Dictator: The Efficiency and Risks of “I Have the Final Say”

The first category of stablecoins are one-sided markets where a single entity generates yield on depositors’ capital. Examples of this category of stablecoins include Ondo, Ethena, Usual, Agora, Resolv, and other synthetic assets backed by team-operated strategies. They are similar to hedge funds where a single (sometimes a small number of) strategies are picked and executed by the dApp team. As the name suggests, the first category of stablecoins are centralized, with the team having the final say on capital allocation and recourse. Depending on the team, they may offer safeguards including over-collateralization, decentralization, and transparency, but this is at the team’s discretion, so risk is naturally concentrated.

The main motivation for adopting this model is to reduce team development costs and increase user agency. Development costs are low because the protocol focuses on a single strategy (such as basic transactions). At the same time, users can switch between different stablecoins of this type and choose specific strategies.

Incentive mechanism adjustment

In this model, the decision maker is the dApp team. Generally, the team will optimize yield and security to attract more users. If the yield is not competitive, or user funds are lost, the project may quickly become obsolete as more and more projects are launched. Therefore, the teams attention is often placed on continuing to grow TVL and maintaining competitive yields.

In theory, the team should make the strategy as risk-free as possible. However, most of these stablecoins exist in the form of bankruptcy-remote entities, and users cannot seek regulatory or legal protection, so the team does not have to put user protection and transparency first like those strictly regulated financial institutions.

Weighing the pros and cons

The main reason for choosing the first type of stablecoin design is simplicity. Since this model can concentrate resources to implement a single strategy, they have lower startup costs and can also reduce concerns about potential vulnerabilities. Another advantage is user choice. By focusing on one or two strategies, the team returns decision-making power to users, who can transfer funds between different applications based on market changes.

However, as mentioned earlier, the first type of stablecoins generally lack effective recourse mechanisms. They operate similar to unsecured loans to the application team. If the strategy leads to losses, the custodian goes bankrupt, or the team runs away with user deposits, users have little way to recover their losses. And due to the lack of regulation, the team may protect themselves through legal structures to avoid liability.

Another key issue is strategy obsolescence - no strategy can efficiently generate returns that exceed the market indefinitely. When the team chooses a strategy that meets market conditions, it may achieve abnormal returns of more than 30% . However, as the market environment changes, the teams returns gradually disappear or are diluted as the scale increases. At this time, the team has to constantly look for new strategies to adapt to market changes.

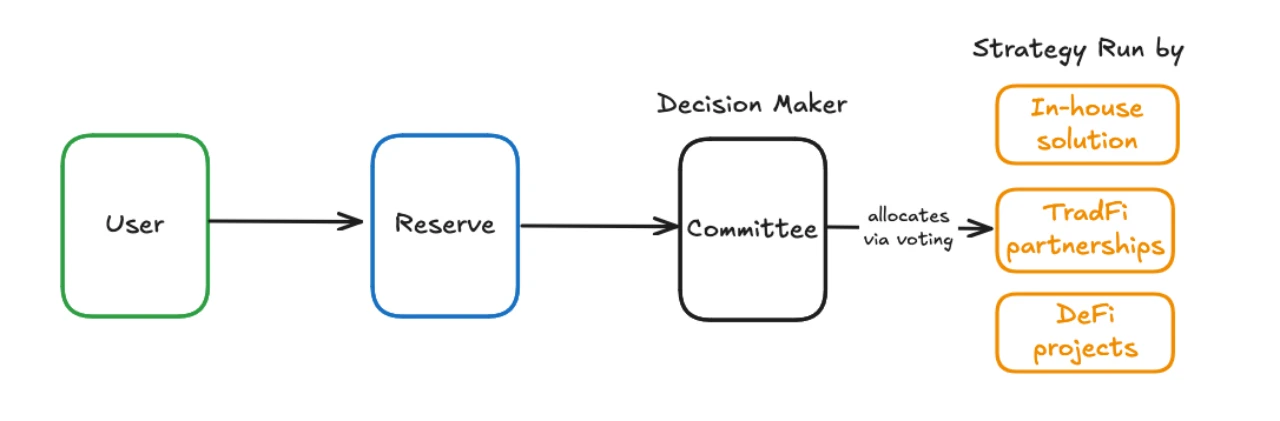

Category 2: Committee game - Can “collective decision-making” cure all diseases?

To solve the problem of outdated strategies, the second type of stablecoins introduces a mechanism for multiple strategies to run in parallel. Examples of the second type of stablecoins include Maple and Sky (formerly MakerDAO). They entrust user deposits to multiple yield strategies, including the first type of stablecoin team, as well as banks and market makers from outside the crypto space, by establishing a committee or decentralized autonomous organization (DAO). Therefore, this model transfers the execution responsibility from a single team to an organization that makes collective decisions.

The main motivation for adopting a second type of stablecoin is scalability. If the current strategy does not bring significant returns or the risk is too high, the DAO can decide to switch to a better strategy. In this way, the second type of stablecoin can provide users with stronger robustness guarantees.

Incentive mechanism adjustment

Overall, capital allocation decisions are made by governance token holders, representatives, and the committee.

The goal of governance token holders is to vote for the most expressive and scalable third-party strategies. Unlike governance tokens in the first category of stablecoins, governance token holders in the second category of stablecoins have greater decision-making power and are able to have a greater influence on the DAOs decisions in an open forum. However, it should also be noted that governance token holders are not necessarily the most risk-savvy participants.

Delegates are actors who do not have governance tokens but exercise voting rights through authorization by governance token holders. Typically, investors and founders delegate voting rights to professional delegates, DAO service providers, or university blockchain clubs. It is worth noting that delegates are not necessarily bound by the interests of depositors, as their main source of income is the compensation they receive for their proxy services, rather than the interests of users.

The committee is the decision-making body in the project, responsible for making a range of specific decisions, including the introduction of new collateral, the development of marketing strategies, and the management of other core functions. The committee is the direct decision-maker in the process of allocating capital to generate returns. Similar to the delegators, the committee is aligned with the depositors through the monetary compensation they receive from the project. Compared with representatives, the entry requirements of the committee are more stringent. Members of these committees are often dxxed - adding an extra layer of protection for members who value their public brand.

Weighing the pros and cons

The distinguishing feature of the second category of stablecoins is scalability through outsourcing. As a layer on top of yield stablecoins (including the first category of stablecoins), they are able to leverage market forces to achieve large-scale returns. In this model, the allocation of capital will change with the changing market environment, and the governance structure will reallocate capital based on returns and security performance. Therefore, the second category of stablecoins has a stronger robustness guarantee than the first category of stablecoins.

However, like the first category of stablecoins, the second category of stablecoins also faces the problem of no guaranteed recourse. If the third-party team loses funds, the end user will not be able to recover the losses. Since these organizations are decentralized, legal recourse is not feasible.

Another important factor to consider is the issue of corruption. As past DAO experiments have shown, the security of capital allocation can be directly affected by bribing and corrupting DAO representatives, voters, and committee members. Special advisory positions, regular payments, and token distributions are common ways to corrupt decision makers. This directly affects the security of the second category of stablecoins, as corrupt decision makers may allocate capital to unsafe or malicious actors.

The third category: Mechanisms are rules - when stablecoins learn to self-generate blood

The third category of stablecoins represents a move away from subjective human decision-making and toward an automatically executed system of shared rewards and penalties. In a sense, they are more like a protocol than a traditional hedge fund. The process of capital allocation and recourse handled by human decision-makers is replaced by unchangeable rules set by smart contracts.

The core motivation for adopting Category III stablecoins is improved security and reduced latency. Users are protected at the smart contract level, and can inspect the code to verify the recourse mechanism when the strategy fails. In addition, the response speed to strategy switching in the open market is greatly accelerated, and it can quickly adjust to changes in market dynamics. This allows Category III stablecoins to fully leverage the power of the market and quickly deploy multiple parallel yield strategies.

Cap’s ambition: to create a “perpetual motion machine” for stablecoins

Currently, there is no third type of stablecoin on the market, and Cap is the first stablecoin to create this category.

Cap innovates the first third-class stablecoin by leveraging lending markets and a shared security model (SSM) to provide efficient capital allocation and trusted financial guarantees. The protocol oversees the ability of third-party operators to generate returns by issuing smart contract-level rules of engagement. Interested readers are advised to read the introduction article for an overview of its mechanisms.

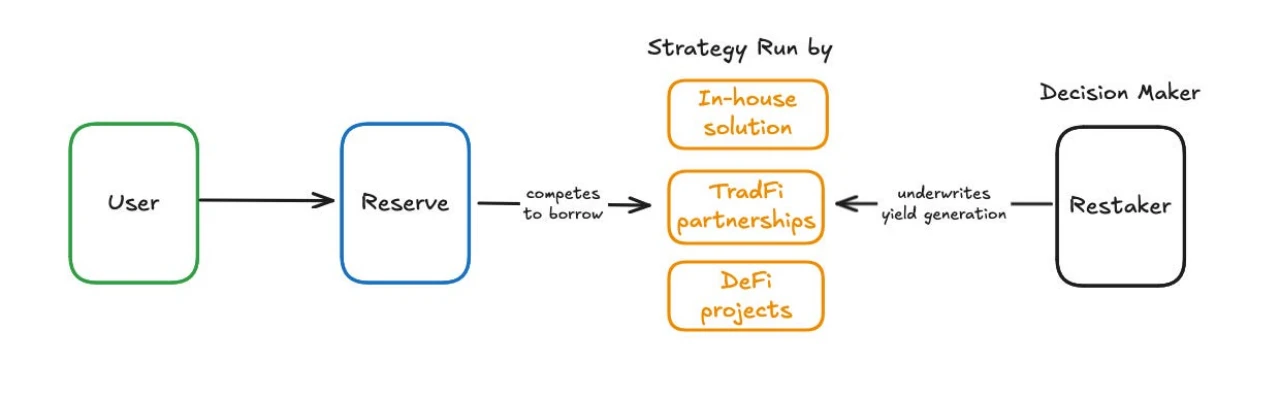

Cap is a three-party market that brings together operators, heavy stakers, and end users.

Cap is a three-party market that brings together operators, heavy stakers, and end users.

Operators are financial institutions responsible for generating yield. Their participation is regulated by smart contracts and market dynamics. Before an operator borrows any assets, the protocol first checks whether they have over-collateralization or over-security, which is common in the crypto lending market. The difference here is that operators do not invest capital themselves, which would reduce capital efficiency, but instead accept the entrustment of heavy stakers to use locked crypto assets as collateral. The previously idle heavy staked assets start to earn yield through this new use. All the operator has to do is convince the heavy stakers to entrust their bets to them.

The allocation of capital to operators is economically regulated through interest rates set by the lending market mechanism. Rather than the team deciding how much funding each operator should receive, operators themselves choose to join the protocol based on whether they can provide a yield at the current benchmark rate. The benchmark rate is also determined programmatically - it is the deposit rate of the main lending market plus a usage premium on Cap. This usage premium is calculated as a percentage of the borrowed capital and indicates the competitiveness of the capital supply under specific market conditions.

Heavy stakers are rewarded for delegating to the operator. The interest rate is determined by the heavy staker and the operator through the agreement. Similarly, end users are rewarded for providing funds, with the interest rate determined by the benchmark yield. The amount they receive is recorded and distributed on-chain, ensuring the transparency of the protocol.

If the operator acts maliciously or a black swan event occurs, resulting in a loss of loan amount, the heavy staker will be subject to slashing. Slashing will remove the cryptocurrency held as collateral by the heavy staker to compensate the end user. The slashed funds will be redistributed to the end user, ensuring that recourse is always available and verifiable through code.

Incentive mechanism adjustment

Since third-party operators must obtain authorization from heavy stakers to borrow, the decision makers of Cap are actually heavy stakers. Heavy stakers have the final say on which third parties can enter the protocol and generate income.

Heavy stakers are incentivized through the delegation premium provided by the operator. Heavy staked assets have low opportunity costs and low capital premiums because they are locked crypto assets. In other words, these assets cannot be used to generate significant returns. Therefore, heavy stakers are motivated to entrust this idle value to the operator for use. While having the power to make decisions, heavy stakers are also directly exposed to the results of the decisions, so they are encouraged to prioritize security.

It can be noted that the ultimate goal of Cap is to be a completely permissionless, minimally governed protocol where operators and heavy stakers are free to participate. However, given the novelty of the design, in the early stages of the protocol, heavy stakers and operators will be certified institutions and will be whitelisted. This provides a safety mechanism for heavy stakers as they have a way to reach an agreement with the other party and enforce legal recourse.

Weighing the pros and cons

The key advantage of this model is its security. Since decision makers bear full risk for the outcome of their decisions, retail holders do not need to worry about the process of generating returns. All rules are enforced by smart contracts, and no human arbitration is required. This provides retail investors with stronger regulatory protection than traditional finance.

Similar to Class II stablecoins, latency is reduced when identifying and adopting new strategies. The system has no switching costs when reallocating capital. Unlike Class II stablecoins, allocating capital does not require lengthy DAO and committee deliberations. Each staker has the right to allocate capital to the operator individually and simultaneously.

However, compared with the second category of stablecoins, the third category of stablecoins is more complex. This complexity may trigger the risk of smart contracts because the entire system relies on code to regulate the execution process.

Conclusion: Paradigm shift is inevitable

Currently, interest yields are still far from reaching a level sufficient to unleash the potential of DeFi. As the stablecoin market continues to grow, there will be more and more interest-yielding stablecoins supported by strategies. But unless there is a paradigm shift in the basic design of these stablecoins, they will once again face the same risks and fatigue and will not be able to scale. Therefore, it is urgent to develop a more efficient, scalable, and secure system that goes beyond the traditional limitations of human decision-making and promotes the widespread use of stablecoins.