Original: Galaxy

Translator: Denglian Community

Editors Note: This article analyzes the GENIUS Act, a bill proposed by the U.S. Senate, which aims to establish a comprehensive framework for stablecoin issuance and regulation to promote innovation, protect consumers, maintain the security of the financial system, and consolidate the global dominance of the U.S. dollar. The article details the key provisions of the bill, the regulatory framework, and the revisions made since its passage by the Senate Banking Committee. It also discusses the Democratic Partys criticism of the bill and concerns about national security, anti-money laundering, and consumer protection.

Update on Senate Stablecoin Bill

Latest Developments on the GENIUS Act

This report was originally sent privately to Galaxy clients and counterparties. Invest or trade with Galaxy to receive premium research directly as it is published. - Alex Thorn

introduce

At the time of writing, there are over $243 billion in stablecoins in circulation worldwide . Of these, $218 billion (90%) are fully collateralized and denominated in USD. In 2025, over $700 billion worth of these stablecoins could be circulating in over 120 million transactions per month. Stablecoins are widely used for cross-border payments, costing a fraction of traditional remittances per transaction. But today, they exist primarily in a legal gray area in the U.S., where incumbents are not regulated enough to truly thrive in the traditional system, and traditional players face too much regulatory uncertainty to use cryptocurrency rails.

The United States Stablecoin National Innovation Guidance and Establishment Act of 2025 (the “GENIUS Act”) is the Senate’s stablecoin authorization and regulation bill that seeks to bring clarity and certainty to this gray area. It was introduced by Senator Bill Hagerty (R-TN) and co-sponsored by Senator Tim Scott (R-SC), Senator Kirsten Gillibrand (D-NY), Senator Cynthia Lummis (R-WY), and Senator Angela Alsobrooks (D-MD).

The bill would establish strong oversight and regulation for U.S. stablecoins and issuers, create pathways for innovation, and enhance the dollar’s global issuance and reserve status. Stablecoins issued under the framework would be strictly regulated by federal standards, whether they are supervised by federal banking regulators, U.S. states, or foreign issuers. The Senate Banking Committee voted the bill out of committee in March by 18 to 6 (including 5 Democrats).

On Thursday, May 1, an updated draft was released ( published ) that included several substantive updates that enhanced language on national security, financial system safety, and regulatory responsibilities. On Saturday, May 3, nine Democrats released a statement saying they would oppose cloture in Congress if additional improvements covering five areas were not made.

This note provides an overview of the GENIUS Act, explains the regulatory framework it would create, and highlights the key differences between the latest version and the one passed by the Senate Banking Committee.

What is the GENIUS Act?

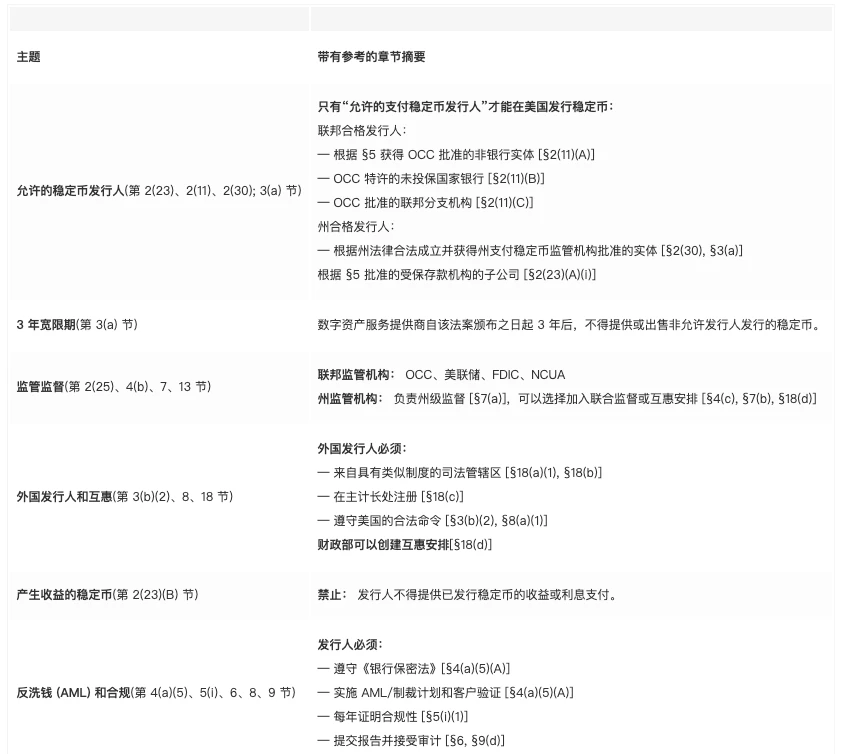

The GENIUS Act creates an overall framework to regulate stablecoin issuers located in the United States or whose stablecoins are circulated or traded within the United States. Currently, stablecoin issuers are typically registered with the Treasury Departments FinCEN as money service businesses (MSBs) and/or have certain state licenses, but other than some state regimes, there is no nationwide, comprehensive regulatory oversight regime governing collateral handling, AML/CFT compliance, creation and redemption mechanisms, supervision, consumer safety, bankruptcy remoteness, or much else. Essentially, there is little regulation of dollar-backed stablecoins in the United States.

The table below describes the framework established in the latest version of the GENIUS Act, released on Thursday, May 1st.

Interpretation of the provisions of the GENIUS Act

Broadly speaking, the bill creates a highly regulated framework for stablecoin issuance in the United States that:

It protects consumers by requiring bank-like regulation of issuers (whether or not they are banks themselves). It has strict short-term collateral requirements, making stablecoin reserves comparable to the stability of money market funds. And, in the event of an issuer’s bankruptcy, stablecoin holders have priority, and reserve assets are considered “bankruptcy remote” in any bankruptcy proceedings.

Protecting the safety and soundness of the financial system by placing the Office of the Comptroller of the Currency (OCC) in the primary regulatory oversight seat for stablecoin issuers. Stablecoin issuers, whether banks or non-banks, must register with the OCC or in a state where regulation is considered comparable to federal minimum standards. The liquidity of the collateral reserves and their full reserve backing ensure that stablecoins are comparable to money market funds.

Allows innovation to flourish. Given the transparency, speed, and efficiency of public blockchains, stablecoins have tremendous utility and represent a beachhead for using such blockchains to settle financial transactions. They are widely used by individuals, businesses, and nation-states around the world and represent a significant improvement over the current financial rails for transferring dollars. The bill gives U.S. “digital asset service providers” (essentially U.S. trading firms and exchanges) a 3-year grace period to allow trading of existing but unregistered stablecoins, allowing the industry and market to transition to the new regime without disruption.

Consolidate and expand the dominance of the US dollar. While the dollar’s influence faces headwinds due to international trade and geopolitical developments, it has no rival in cyberspace. More than 99% of stablecoins in circulation are currently denominated in US dollars. Bringing stablecoins under the regulatory umbrella of the world’s most advanced and trusted capital markets regulatory regime will increase their use and help export the dollar around the world.

Supporting U.S. Treasury issuance. By requiring full reserves to be composed almost entirely of U.S. Treasuries, the growth of stablecoins means growth in the U.S. government’s borrowing capacity.

Criticism from Democrats

Nine Democrats said they would vote against the cloture of the GENIUS Act, including six members of the Senate Banking Committee, five of whom previously voted to advance the bill out of committee.

However, the bill in its current version still leaves many issues that must be addressed, including the addition of stronger provisions on anti-money laundering, foreign issuers, national security, maintaining the safety and soundness of our financial system, and accountability for those who fail to meet the bills requirements, the nine Democrats wrote in a statement Saturday evening. While we are eager to continue working with our colleagues to address these issues, we will not be able to vote for cloture if the bill in its current version is brought to the floor.

Politico reported the announcement under the headline “Democrats change tack against Senate cryptocurrency bill,” though Senator Gallego denied the change, saying “this was not a change Democrats made in a vacuum” and that “the bill introduced for consideration in the chamber departs from much of the progress we have made and does not include the additional improvements we sought.”

Updates on the bill since marking

Below, we provide an analysis of the changes made to the latest draft of the bill (after marking up) versus the version of the bill that passed the Senate Banking Committee. We categorize the analysis of the changes based on the five categories that Gallego and Democrats have indicated they remain concerned about: 1) Anti-Money Laundering, 2) Foreign Issuers, 3) National Security, 4) Maintaining the Safety and Soundness of our Financial System, and 5) Accountability for Noncompliance with the Act.

National Security

Complying with a lawful order (Section 4(a)(6))

Require stablecoin issuers to demonstrate the technical ability to comply with U.S. lawful orders (e.g., to freeze, destroy, block tokens).

Definition of “lawful order”

It now includes clarity requirements and mandates judicial or administrative review.

Ministry of Finance coordination requirements

Where feasible, the Treasury Department must coordinate with issuers when blocking digital assets.

Exemptions for Intelligence and Law Enforcement Agencies (Section 8(e)(3))

Exempt U.S. intelligence and law enforcement operations from key restrictions.

National Security Waiver (Section 8(e)(2))

The Treasury Department, in consultation with the Director of National Intelligence and the State Department, can waive secondary transaction restrictions if national security requires.

Foreign Issuers

Foreign Issuer Restrictions (Section 3)

Foreign issuers may not offer stablecoins to U.S. persons unless they comply with new requirements (e.g., comparable foreign regulation, U.S. reserves, registration).

Reciprocity (Sections 16 and 18)

The Treasury Department could determine that a foreign jurisdiction has equivalent regulatory standards, thereby enabling issuers to participate under the following conditions: they must be registered with U.S. regulators; they must comply with U.S. lawful orders; and they must hold reserves in U.S. custody for U.S. users.

Revocation of the 90-day safe harbor

If the Treasury withdraws comparability status, a 90-day grace period allows the market to adjust before the restrictions take effect.

Prohibition of Secondary Trading (Section 8(c))

Following the designation, trading of non-compliant foreign stablecoins within the United States is prohibited — unless a waiver is granted by the Treasury Department.

Anti-Money Laundering (AML)

Expanded AML Program Requirements (Section 4(a)(5))

Issuers must: implement AML/CIP/sanctions compliance, monitor and report suspicious activity, keep records and conduct enhanced due diligence.

Annual AML Certification (Section 5(i))

Officials must certify AML compliance annually; false certifications trigger criminal liability and risk revocation.

New section on AML innovation (Section 9)

Treasury must research novel tools (e.g., artificial intelligence, blockchain forensics) to improve AML compliance; FinCEN needs to follow up with guidance or rulemaking.

Foreign Issuer AML Designation (Section 8(b))

If a foreign issuer fails to comply with a lawful order related to AML, the Treasury Department must designate it as non-compliant.

Soundness and safety of the financial system

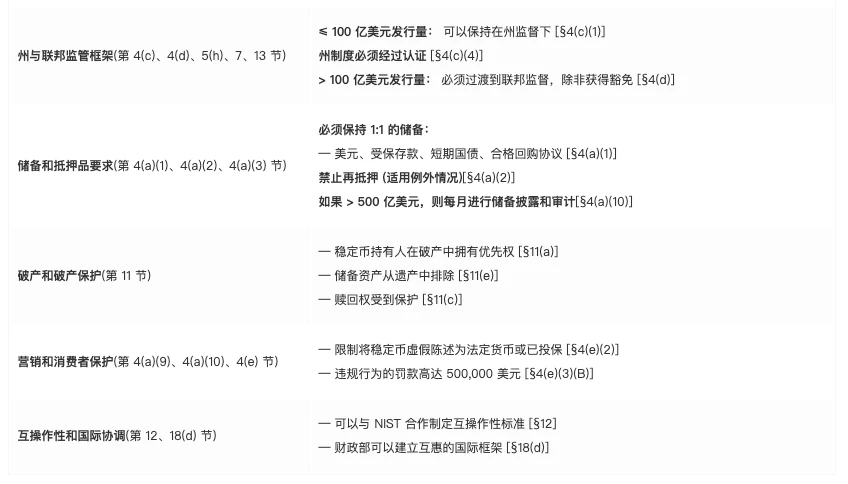

Reserves and Asset Backing (Section 4(a)(1))

Strengthen the 1:1 asset backing requirement; assets must be high quality and highly liquid.

Bankruptcy Protection (Section 11)

Ensure that stablecoin holders have priority claims over other creditors; enforce timely redemption in the event of the issuer’s bankruptcy.

Federal assessment of financial risk (Section 15)

Added a requirement for the FSOC to assess risks associated with stablecoins in its annual Financial Stability Report.

State-Federal Coordination (Section 7)

Strengthen Treasurys oversight of state-regulated issuers by requiring federal certification of substantially similar state systems.

Prohibition of yield-generating stablecoins (Section 2(23))

Permitted stablecoin issuers are not allowed to offer yield or interest on their stablecoins.

Accountability and Enforcement

Civil Penalties for Domestic Violations (Section 6(c)(5))

Unauthorized issuance is subject to a fine of up to $100,000 per day; knowing violations are subject to a fine of $200,000 per day; and post-employment accountability is subject to a maximum of six years after leaving employment.

Penalties for Violations by Foreign Issuers (Section 8(c)(4))

Fines of up to $1,000,000 per day following designation; Treasury may seek an injunction to stop U.S. transactions.

Judicial review of Treasury actions (Section 8(d))

Allows foreign issuers to appeal noncompliant designations to the D.C. Circuit.

Increased powers for regulators (Section 6)

Authorizes federal regulators to deregulate, remove officials, and issue cease-and-desist orders, among other oversight tools.

Each of these changes was made within weeks of the bill’s overwhelming committee vote (18-6, with 5 Democrats joining Republicans in passing), and many reflect specific requests from members of the Senate Banking Committee who either voted against the bill in committee or requested such changes before the bill was sent to the floor for consideration. Our analysis shows that nearly all of the changes make the bill more restrictive on stablecoin issuers than the version voted through by the Senate Banking Committee.

in conclusion

Overall, the GENIUS Act in its latest form represents a strong, pro-innovation, consumer-protecting, win for both the cryptocurrency industry and traditional finance. It creates a reasonable path to registration while also imposing strict oversight and regulatory requirements, as well as stiff penalties for noncompliance. Passage of the GENIUS Act will promote the use of the U.S. dollar both within and outside the United States, making it easier for individuals and businesses to conduct everyday transactions domestically, across borders, or in international trade. All parties involved gain something important here: the cryptocurrency industry gains both a viable path and control, it protects the financial system, and it helps the United States succeed in geopolitical and changing global economics.