In recent years, the scope of virtual assets has expanded rapidly around the world. Decentralized financial products have not only impacted the boundaries of the traditional financial system, but also challenged the existing financial regulatory framework. As we all know, virtual assets have two major characteristics: high price volatility and high leverage in transactions. This has posed a series of unprecedented regulatory challenges to both regulatory authorities and trading platforms: How to regulate cross-border capital flows? How to complete customer identity identification (KYC)? How to avoid systemic financial risks such as death spirals? ... This series of question marks all express the fact that the regulation of virtual assets will inevitably become a comprehensive issue that requires cross-departmental and cross-national collaboration.

The importance of Hong Kongs virtual asset regulatory policy is well known: on the one hand, as the worlds third largest global financial center, Hong Kong occupies a key position in the global financial system; on the other hand, Hong Kong carries the special system under Chinas one country, two systems. Its regulatory policy must not only shoulder the mission of promoting the global virtual asset financial market, but also meet the central governments requirements for financial stability. Hong Kong must find a balance between linking the international capital market and the financial security of the mainland. At the same time, Hong Kong must be an important window and test field for China to explore the development of emerging financial markets. Therefore, Hong Kongs virtual asset regulatory path must be complex, and it is a process of continuous reconciliation between globalization and localization, innovation and stability.

Therefore, in this article, Crypto Salad will systematically sort out the regulatory policy framework of virtual assets in Hong Kong for readers, hoping to help everyone establish a more comprehensive and clear understanding.

2017-2021: From risk warning to system prototype

This stage is the starting stage of virtual asset regulation in Hong Kong. The Hong Kong government mainly focuses on risk warnings and gradually introduces pilot regulatory elements. During this period, the Hong Kong governments regulatory attitude gradually transitions from a cautious wait-and-see attitude to orderly regulation. Specifically:

On September 5, 2017, the Hong Kong Securities and Futures Commission (SFC) issued a Statement on Initial Coin Offerings, pointing out that some initial coin offerings (ICOs) may constitute securities under the Securities and Futures Ordinance and need to be regulated, laying the foundation for the classification of virtual assets.

On December 11, 2017, the SFC issued a Circular to Licensed Corporations and Registered Institutions on Bitcoin Futures Contracts and Cryptocurrency-Related Investment Products, requiring financial institutions to comply with existing financial regulations if they provide cryptocurrency-related products.

The promulgation of these two first-generation regulations shows that Hong Kongs attitude towards virtual asset regulation during this period was conservative and cautious, but it has begun to try to incorporate virtual assets into the existing legal regulatory system through the classification method of securities attributes.

On November 1, 2018, the SFC issued a Statement on the Regulatory Framework for Virtual Asset Portfolio Management Companies, Fund Distributors and Trading Platform Operators, which aims to clarify the regulatory framework for virtual asset portfolio management and trading platform operations, and proposes to include virtual asset trading platform operators that meet the standards into the CSRCs regulatory sandbox. In the regulatory conceptual framework proposed by the SFC, the core regulatory content is the provisions for professional investors, the prohibition of leverage and derivatives, the restrictions on ICO transactions (trading must be allowed at least 12 months after issuance), and customer asset isolation and other related regulations.

On March 28, 2019, the CSRC issued a Statement on the Issuance of Security Tokens, which defined STOs and made preliminary provisions on the responsibilities of intermediaries. This statement has been replaced and updated by a circular issued on November 2, 2023.

On November 6, 2019, the CSRC issued the Warning on Virtual Asset Futures Contracts and the Position Paper: Regulating Virtual Asset Trading Platforms, warning investors to pay attention to the risks associated with purchasing virtual asset futures contracts. In the Position Paper, a licensing system was proposed, and it was again proposed that platforms must prove that they meet strict standards and voluntarily apply for licenses to be included in the CSRCs regulatory sandbox. In this document, the CSRC also proposed the review rules for token access and plans to set up a committee to evaluate the compliance of tokens.

In November 2020, the Financial Services and the Treasury Bureau launched a consultation on amendments to the Anti-Money Laundering Ordinance and plans to include virtual asset service providers (VASPs) in the licensing system.

In May 2021, the Treasury Bureau released a summary of the above consultation, formally confirming the introduction of a VASP licensing system, requiring those engaged in related businesses to apply for licenses and comply with anti-money laundering regulations.

Hong Kong has gradually shifted from warning of risks to specific regulations on behavior, and has begun to define the responsibilities of participants in the virtual asset market. At this point, regulators have realized that virtual assets will become an important part of the financial market, and their attitudes have slowly shifted toward positive management. However, for participants in the ecosystem, the principle of voluntary participation is still in place. The Hong Kong government has introduced the prototype of a licensing mechanism. If a platform chooses to accept supervision, it needs to actively apply for a license and prove that it meets the standards.

It is worth noting that the mechanism of regulatory sandbox has also entered the publics field of vision and is used in the supervision of virtual asset trading platforms. The concept of sandbox was first proposed and practiced by the United Kingdom. It is a mechanism that allows emerging financial technology companies or projects to test products, services or other business models in a specific, controllable environment and within a limited scope, without having to fully meet all existing regulatory requirements. Since the traditional regulatory model is bound to lag behind the development of technology, the sandbox mechanism can provide some potential innovative projects with relatively free and abundant soil for growth. The significance of the sandbox is that it is different from the traditional one-way government supervision. It is more like the regulator and the market crossing the river by feeling the stones and fully testing the waters in a small area. It has considerable inclusiveness and practical significance.

At this point, Hong Kongs regulation of virtual assets has reached the threshold of maturity and institutionalization. The focus of supervision is no longer limited to the classification and judgment of products, but tends to build a complete compliance ecosystem. Combined with the global trends during this period, even in the United States and the European Union, the virtual asset market is still in its early stages, and excessive regulatory involvement may inhibit technological innovation and industry exploration.

In addition, mainland China has always maintained a high-pressure stance on crypto assets during this period: In 2017, seven Chinese ministries and commissions issued the Announcement on Preventing the Risks of Token Issuance and Financing, which completely stopped ICOs and closed related domestic trading platforms; after 2018, the mainland strengthened the crackdown on disguised transactions and over-the-counter transactions; in September 2021, ten departments jointly issued the Notice on Further Preventing and Dealing with the Risks of Virtual Currency Transaction Speculation, which classified all virtual currency-related businesses (transactions, redemption, intermediaries, advertising, etc.) as illegal financial activities.

In the polarized regulatory direction, Hong Kong chose the third regulatory strategy: neither radically releasing nor banning across the board. As a financial special zone under the framework of one country, two systems, Hong Kong did not have the space to rush to establish an independent path in relevant policies. Moreover, at that time, there was no unified regulatory consensus in the international community, and Hong Kong had neither the conditions nor the need to rush ahead.

2022: A critical juncture for policy transformation

By 2022, this lukewarm regulatory style had undergone a dramatic shift, officially transforming from the previous limited supervision based on wait-and-see approach to active and proactive policy support.

2022 officially became a watershed year for Hong Kongs virtual asset regulatory policy: On October 31, 2022, the Treasury Department issued the first Policy Declaration on the Development of Virtual Assets in Hong Kong, which made it clear for the first time that Hong Kong will actively promote the development of the virtual asset ecosystem. The policy declaration not only stated that the VASP licensing system will be implemented, but also proposed to support emerging scenarios such as tokenization, green bonds and NFTs, marking the shift of regulatory thinking from risk-oriented to opportunity-oriented, establishing a strategic direction for subsequent institutional reforms.

This declaration marks a substantial change in the Hong Kong government’s attitude towards virtual asset regulation. Crypto Salad believes that this change is not groundless. Combined with the international situation at the time, the motivation behind it can be roughly attributed to two points:

1. With the intensification of international competition, Hong Kong needs to maintain its status as a financial center. At that time, although the global virtual asset market experienced fluctuations, emerging Web3 fields such as Web3, NFT and Metaverse accelerated their development, and major financial centers around the world increased their virtual asset layout. As an international financial center, Hong Kong has fallen behind competitors such as the United States and Singapore. In particular, after Singapore introduced the Payment Services Act in 2020, it attracted a large number of Web3 companies and projects to land in Singapore. Hong Kong urgently needs to adjust its policies to compete for industry resources, otherwise it is likely to miss the window for the development of global digital finance.

2. From a market perspective, the development of virtual assets has given rise to multiple demands, and Hong Kong happens to play the role of a key connection point. Hong Kong itself needs a breakthrough and transformation opportunity for a new financial industry to strengthen its position as an international financial center; mainland China hopes to have a test field to explore the digital economy under the premise of compliance; and the pioneering group of practitioners is also eager to find a regulated and orderly foothold in Hong Kong to achieve legal compliance of assets, businesses and identities; trading platforms are eager to obtain institutional protection and legitimacy under the legal framework. These demands gradually converged around 2022, providing realistic conditions for a substantial relaxation of Hong Kongs virtual asset policies.

In short, this transformation is not only about catering to innovative financial markets, but also a proactive strategic choice for Hong Kong to maintain its status as a financial center in a complex international environment.

2023-Present: Rapid iteration, deepening and transformation of regulatory policies

Since 2023, Hong Kongs virtual asset regulation has officially entered the practical implementation stage. The past experimental model has gradually been replaced by a complete and mandatory legal and licensing system. The Hong Kong governments policy has officially evolved from policy statement to regulatory implementation, gradually becoming complete and institutionalized.

In February 2023, the Hong Kong SAR government issued its first tokenized green bond. The bond is held in trust by Bank of China (Hong Kong) and HSBC, and the cash tokens are managed through the HKMAs Central Moneymarkets Unit (CMU).

In June 2023, the SFC officially implemented the Guidelines for Virtual Asset Trading Platforms and launched the VASP licensing system. Only two platforms in the first batch - OSL and HashKey - were successfully approved during the transition period.

In the same month, the Anti-Money Laundering and Terrorist Financing (Amendment) Ordinance officially came into effect, indicating that virtual asset trading platforms (VATPs) must be licensed, and regulatory requirements cover capital adequacy, cold wallet custody, KYC/AML, market manipulation prevention, investor suitability assessment and other aspects. With the introduction of the Virtual Asset Trading Platform Guidelines, Hong Kong has completely shifted from optional regulation to mandatory licensing, establishing clear market access thresholds and operating regulations. In addition, restrictions on investors have also been relaxed from professional investors to retail investors, but the premise is that the platform meets additional protection requirements such as investor suitability assessment, risk disclosure, and cold wallet custody.

In August 2023 , HashKey became the first licensed exchange in Hong Kong open to retail investors, marking that retail investors can participate in virtual asset transactions in compliance with regulations. The first batch of Bitcoin (BTC) and Ethereum (ETH) were listed, marking the beginning of the compliance of the retail market.

This series of legislative measures in 2023 marks that Hong Kongs virtual asset licensing system has officially entered the practical stage, and the supervision of platforms has changed from voluntary acceptance to mandatory requirements. At the same time, Hashkey, as the first platform to be licensed during the transition period, has laid the standard for the industry. At the same time, the entry into force of anti-money laundering legislation has formally included virtual asset trading platforms in the anti-money laundering regulatory framework equivalent to traditional financial institutions, consolidating the legal basis of the licensing system.

In November 2023, the SFC issued a circular on intermediaries engaging in activities related to tokenized securities, which reiterated that although tokenized securities are issued using blockchain technology, they are still traditional securities in nature and must comply with existing securities laws. When distributing, trading, and managing such assets, intermediaries must conduct due diligence, ensure product suitability, and notify the SFC in advance.

In December 2023, the HKMA and the SFC jointly issued an updated version of the Circular on Virtual Asset-Related Activities of Intermediaries, which clarified for the first time that virtual asset spot and futures ETFs are available for compliance sales. The issuance of this circular represents the extension of Hong Kongs compliance requirements from trading platform supervision to intermediary institutions (such as securities firms, banks, and financial advisors), marking that virtual asset supervision has begun to cover the entire financial distribution chain, forming a complete closed loop of supervision. The circular also allows intermediaries to sell virtual asset-related ETFs for the first time, paving the way for the launch of future spot and futures ETF products.

In the same month, the SFC issued a circular on the SFC’s approval of funds to invest in virtual assets, stating that the SFC must comply with relevant regulations when considering allowing a fund to be publicly offered, and that the fund’s net asset value (“NAV”) involves more than 10% of its net asset value (“NAV”) in virtual assets (“VA”).

In January 2024, GF Securities (Hong Kong) successfully issued the first tokenized securities subject to Hong Kong law.

In March 2024, the HKMA launched the Ensemble Project to explore the integration of tokenized assets and wholesale central bank digital currencies (wCBDCs) and test atomic settlement mechanisms for scenarios including green bonds, carbon credits, real estate, and supply chain finance. Among them, the Ensemble sandbox focuses on exploring the application scenarios of tokenization technology, and several RWA projects have been successfully implemented in it.

In July 2024, the HKMA launched the Stablecoin Regulatory Sandbox Program, allowing institutions to test stablecoin issuance and application models in a controlled environment. The first batch of participants included JD Technology, Circle and Standard Chartered Bank. Among them, JD took the lead in launching the JD-HKD stablecoin anchored to the Hong Kong dollar, exploring its scenarios in payment settlement and supply chain management. This marks that Hong Kong is the first in the world to explore the localization, practicality and compliance path of stablecoins.

In August 2024, Langxin Technology and Ant Financial jointly launched the charging pile revenue rights RWA project.

In September 2024, GCL-Poly Energy and Ant Financial jointly launched the photovoltaic power station revenue rights RWA project.

In February 2025, Financial Secretary Paul Chan announced the release of the second Virtual Asset Policy Declaration, planning to integrate traditional finance and blockchain technology to promote over-the-counter trading and custody service systems.

In February 2025, China Asset Management (Hong Kong, China) announced that its China Asset Management Hong Kong Dollar Digital Currency Fund has been approved by the Hong Kong Securities and Futures Commission (SFC), becoming the first tokenized fund for retail investors in the Asia-Pacific region, and is expected to be officially listed on February 28.

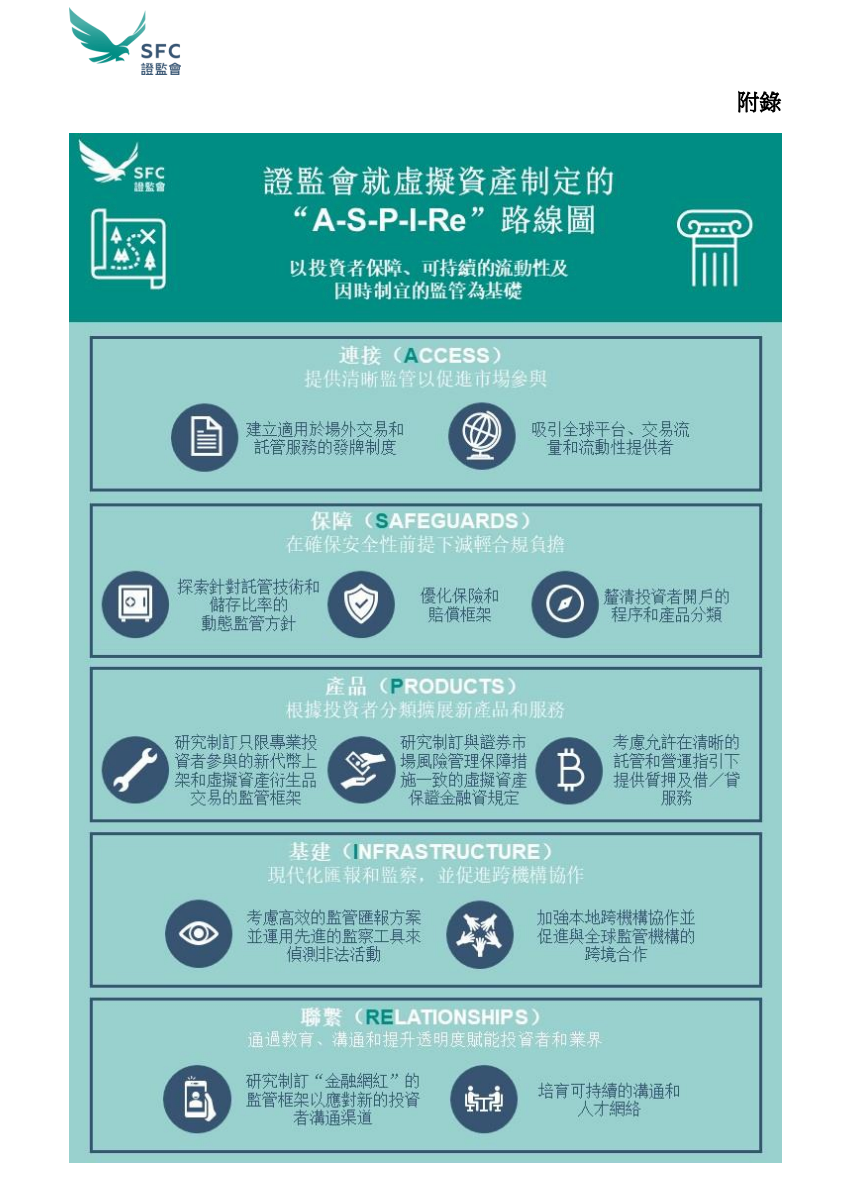

By March 2025, the number of licensed exchanges increased to 10, with 8 under review, and regulatory efficiency and market confidence significantly enhanced. At the same time, the SFC released the ASPI-Re regulatory roadmap to deepen market development with five pillars: connection, security, products, infrastructure, and connection.

In the same month, Patrol Eagle Group successfully launched the worlds first battery swap physical asset RWA project.

Review and analysis of Hong Kongs regulatory system

Through the above overview of the regulatory policies of developed countries for virtual assets and the review of Hong Kongs regulatory path, Crypto Salad believes that Hong Kong did not simply copy the European and American regulatory frameworks, but formed its own governance logic based on international rules.

Hong Kong has always adopted a stamped regulation strategy based on the existing legal framework for virtual assets, that is, to patch digital assets through the issuance of guidelines or circulars, rather than learning from the EU and starting from scratch to formulate a new special code. Combined with Hong Kongs identity as an international financial center, we can make some judgments on the logic behind the regulatory strategy:

The Hong Kong government believes that virtual assets are essentially the same as traditional financial assets, and can even be regarded as an extension of traditional financial assets. Therefore, the most important thing for the supervision of virtual assets is to firmly guard the three lines of defense of financial compliance, anti-money laundering and investor protection, which can be incorporated into the current financial regulatory system for management. As an international city with scarce resources but mature systems, Hong Kong is highly dependent on the financial industry in its economic structure. Its GDP, employment and international influence are closely linked to the stability, transparency and efficiency of the financial system. The rise of virtual assets is an opportunity for Hong Kong, but also a challenge. Objectively speaking, Hong Kongs patch supervision is the most efficient and adaptable supervision method in this field.

From regulatory agencies to financial practitioners, Hong Kong is familiar with risk control and regulatory operations in the fields of securities, banking, and asset management. Although virtual assets are different in terms of technical form, they are similar to financialized assets in terms of function - they can be valued, traded, have markets, have risks, and can be included in a familiar regulatory framework. Therefore, Hong Kongs regulators seem to be more inclined to treat them as extensions of financial assets. This not only reduces the cost of regulatory coordination, but also builds a bridge between financial institutions and emerging technology companies, allowing institutional transformation and industrial development to be better integrated.

This article only represents the personal views of the author and does not constitute legal advice or legal opinion on specific matters.