Original article by Lawrence Lee, Researcher at Mint Ventures

Recently, there have been many developments in the field of tokenized U.S. stocks:

Centralized exchange Kraken announces launch of tokenized stock trading platform xStocks

Centralized exchange Coinbase announces it is seeking regulatory approval for its tokenized stock trading

Public chain Solana submits blockchain-based tokenized US stock product framework

Public chains and exchanges with American backgrounds are accelerating the process of tokenizing U.S. stocks. Coupled with the recent craze after Circles listing, people cant help but look forward to the prospects of tokenizing U.S. stocks.

In fact, the value proposition of tokenized U.S. stocks is very clear:

1. Expanded the scale of the trading market: It provides a 24/7, borderless, and license-free trading venue for U.S. stock trading, which is currently unavailable to NASDAQ and NYSE (although NASDAQ has applied for 24-hour trading, it is expected to be realized in the second half of 2026)

2. Superior composability: By combining with other existing DeFi infrastructure, U.S. stock assets can be used as collateral, margin, to build indexes and fund products, and derive many currently unimaginable gameplays.

The needs of both supply and demand are also clear:

Suppliers (US listed companies): Through the borderless blockchain platform, they have reached potential investors from all over the world and obtained more potential buying orders

Demand side (investors): Many investors who were unable to trade U.S. stocks directly in the past for various reasons can now directly allocate and speculate on U.S. stock assets through blockchain

Quoted from U.S. Stocks on the Blockchain and STO: A Hidden Narrative

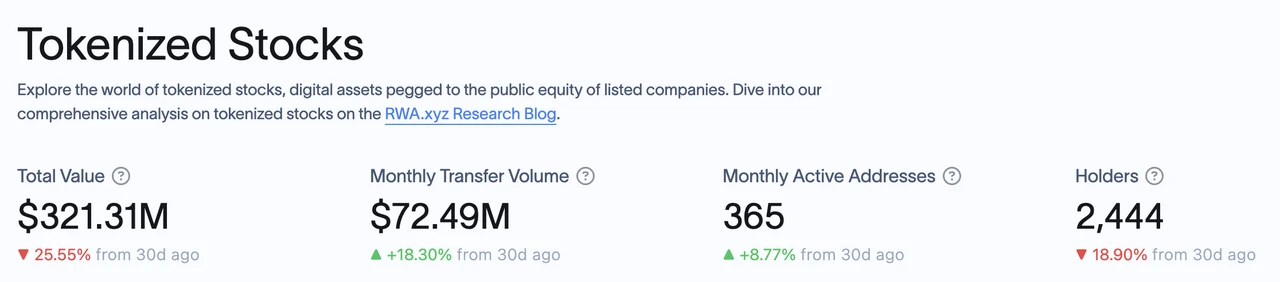

In this round of tolerant crypto regulatory cycle, progress is a high probability event. According to RWA.xyz data, the current market value of tokenized stocks is only $321 million, and there are 2,444 addresses holding tokenized stocks.

The huge market space forms a sharp contrast with the current limited asset size.

In this article, we will introduce and analyze the product solutions of current players in the tokenized U.S. stock market and other players who are promoting the tokenization of U.S. stocks, and list potential investment targets under this concept.

This article is the author’s interim thinking as of the time of publication. It may change in the future, and the views are highly subjective. There may also be errors in facts, data, and reasoning logic. All views in this article are not investment advice, and we welcome criticism and further discussion from colleagues and readers.

According to rwa.xyz, the current tokenized stock market has the following projects by issuance size:

We will look at the business models of Exodus, Backed Finance, and Dinari one by one (Montis Group targets European stocks, and SwarmXs business is similar to Backed Finance but on a smaller scale), as well as the progress of several other important players who are currently working on tokenized US stock business recommendations.

Exodus

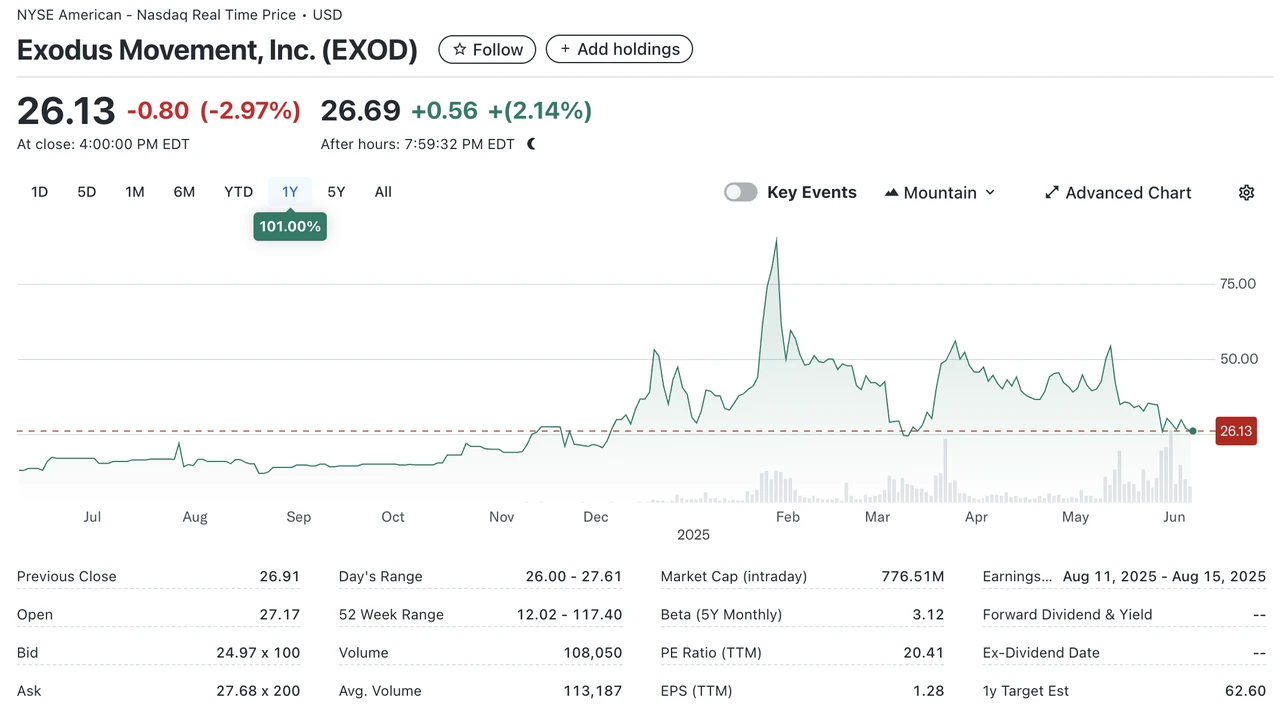

Exodus (NYSE.EXOD) is an American company that develops non-custodial crypto wallets and its shares are listed on the New York Stock Exchange (NYSE.EXOD). In addition to its own branded wallets, Exodus has also collaborated with NFT market MagicEden to launch a wallet.

As early as 2021, Exodus allowed users to migrate their common shares to the Algorand chain through Securitize , but the tokens migrated to the chain could not be traded or transferred on the chain, nor did they include governance rights or other economic rights (such as dividends). The Exodus token is more like a digital clone of real shares, and its symbolic significance on the chain is greater than its actual significance.

The current market value of EXOD is US$770 million, of which approximately US$240 million is on-chain.

Exodus is the first stock approved by the SEC to tokenize its common stock (or to be more precise, Exodus is the first tokenizable stock approved by the SEC to be listed on the NYSE). Of course, this process was not smooth sailing. The listing time of Exodus stock was delayed again and again since May 2024, and it was not officially listed on the NYSE until December.

However, Exodus stock tokenization is only for its own stocks, and the tokenized stocks cannot be traded, which makes little sense for us web3 investors.

Dinari

Dinari is a company registered in the United States. They were founded in 2021. Since its establishment, they have been focusing on stock tokenization under the US compliance framework. They completed a $10 million seed round of financing in 2023 and a $12.7 million Series A financing in 2024. Investors include Hack VC and Blockchange Ventures, Coinbase CTO Balaji Srinivasan, F Prime Capital, VanEck Ventures, Blizzard (Avalanche Fund), etc. Among them, F Prime is a fund under the asset management giant Fidelity. The investment of Fidelity and VanEck also shows the recognition of the tokenized US stock market by traditional asset management institutions.

Dinari only supports non-US users. The process of trading US stocks is as follows:

User completes KYC

The user selects the US stocks they want to buy and pays with USD+ issued by Dinari (a short-term Treasury bond-backed stablecoin issued by Dinari that can be exchanged for USDC)

Dinari submits the order to a cooperating broker (Alpaca Securities or Interactive Brokers). After the broker completes the order, the shares are kept in the custodian bank, and Dinari mints the corresponding dShares for the user.

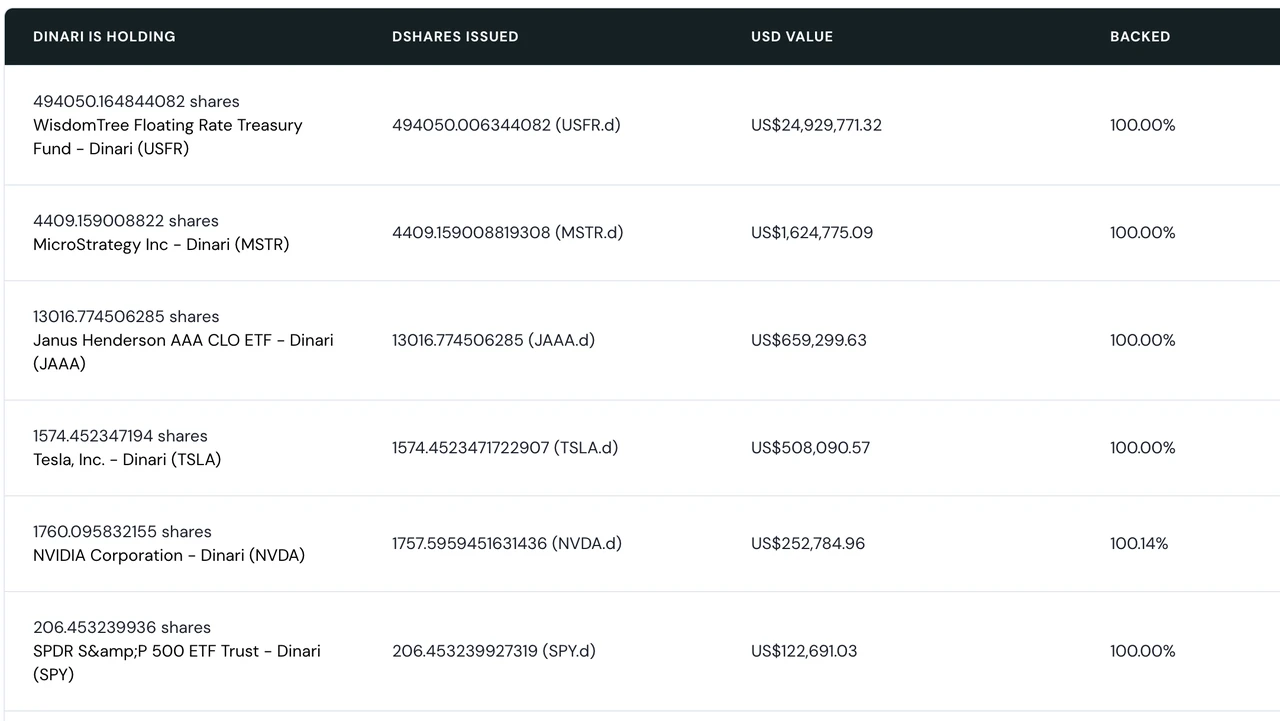

Currently, Dinari operates on Arbitrum, Base, and the Ethereum mainnet. All dShares have a 1:1 correspondence with real-world equity. Users can view the equity corresponding to their dShares through the Dinari official website. Dinari can also distribute dividends or stock splits to users holding its dShares.

However, dShares cannot be traded on the chain. If you want to sell dShares, you can only trade through the Dinari official website. The actual transaction process is the reverse of the purchase process. dShares transactions must also follow US trading hours, and cannot be bought or sold outside of trading hours. In terms of product form, in addition to direct stock trading, they also output stock trading APIs that can work with other trading front ends.

In fact, Dinari’s business process, namely “KYC->payment exchange->clearing and settlement by compliant brokers”, is consistent with the current mainstream way for non-US users to participate in US stock trading. The main difference is that the asset categories paid by users are Hong Kong dollars, euros, etc., while the asset categories accepted by Dinari are encrypted assets. The rest are completely implemented in accordance with the SEC’s regulatory framework.

As a company that mainly deals with the tokenization of US stocks, Dinaris courage to register the company in the United States (the registration places of the corresponding entities of most other projects are in Europe) shows its confidence in its compliance capabilities. Their US stock tokenization products were officially launched in 2023. At that time, the former SEC Chairman Gary Gensler, who was known for his strict regulation of cryptocurrencies, could not find fault with its business model; and after the new SEC Chairman Paul Atkins took office, the SEC once held a special meeting with Dinari, asking Dinari to demonstrate its system and answer relevant questions ( source ), which showed that its products were impeccable in terms of compliance and the teams strong resources in compliance.

However, since Dinaris tokenized U.S. stocks do not support on-chain transactions, cryptocurrency is only an entry and payment method for Dinari. Dinaris products are not much different from Futu, Robinhood and other products in terms of functionality. For its target users, Dinaris product experience has no advantage over its competitors. For a Hong Kong user, the experience of trading U.S. stocks on Dinari is not any better than that of trading U.S. stocks on Futu, and trading functions such as margin trading are not available, and you may even have to pay more expensive fees.

Perhaps because of this, the scale of Dinari’s tokenized stock market has always been small. Currently, there is only one tokenized stock, MSTR, with a market value of more than 1 million US dollars, and there are only 5 tokenized stocks with a market value of more than 100,000 US dollars. Currently, most of its TVL is involved in its floating-rate treasury products.

Source of current tokenized stock market capitalization of Dinari

In general, Dinari’s tokenized stock business model has been certified by regulators, but strict compliance with regulations has also resulted in its tokenized stocks being unable to be traded/pledged on the chain, losing composability, making the user experience of holding its dShare worse than that of traditional brokerages, and the product is not very attractive to mainstream web3 users.

Among the current market players, similar to Dinari is the community project mystonks.org of the Meme coin Stonks. According to the reserve report disclosed by the project party itself, the current market value of their U.S. stock account exceeds 50 million US dollars, and users transactions are more active than Dinari.

However, mystonks.orgs compliance structure still has flaws. For example, the qualifications of its securities custody account are not clearly stated and users cannot verify the reserve report.

Backed Finance

Backed Finance is a Swiss company, also founded in 2021. Its products were launched in early 2023. In 2024, it completed a US$9.5 million financing round led by Gnosis, with participating investors including Cyber Fund, Blockchain Founders Fund, Blue Bay Capital, etc.

Like Dinari, Backed does not provide services to US users. Its business process is as follows:

The issuer (professional investor) completes KYC certification and audit at Backed Finance

The issuer selects the US stocks they want to buy and pays in stablecoins

Backed Finance submits the order to the cooperating broker to complete the stock purchase, and then Backed Finance mints the bSTOCK token corresponding to the stock to the issuer.

Both bSTOCK and its packaged version wbSTOCK can be freely traded on the chain (the packaging is mainly for the convenience of handling stock dividends, etc.). Ordinary C-end investors can directly purchase bSTOCK or wbSTOCK on the chain.

It can be seen that unlike Dinari’s C-end users who directly purchase US stocks, Backed Finance currently has professional investors purchasing US stocks and then transferring them to C-end users, which can significantly improve overall operational efficiency and achieve 24*7 trading hours. Another important difference is that the bSTOCK token issued by Backed is an unrestricted ERC-20 token, and users can form LPs on the chain for other users to purchase.

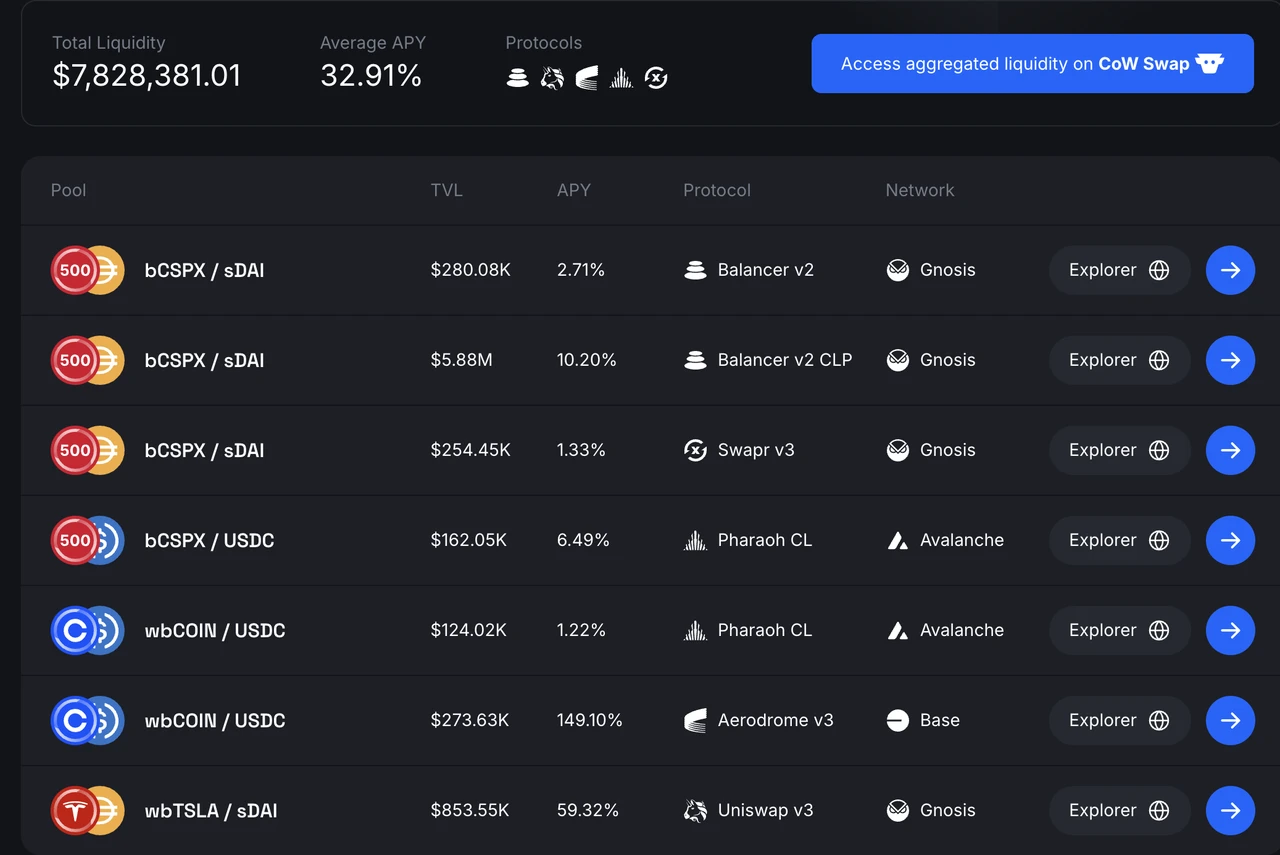

Backed Tokenized Stock Liquidity Source

Backed Finances on-chain liquidity mainly comes from the SPX index, Coinbase and Telsa. Users pair bSTOCK tokens with stablecoins to enter the AMM pool. The total TVL of the liquidity pool is currently close to 8 million US dollars, with an average APY of 32.91%. Liquidity is distributed in Gnosiss Balancer and Swapr, Bases Aerodrome and Avalanche chains Pharaoh, among which the APY of the bCOIN-USDC pool reaches 149%.

It should be noted that Backed Finance does not restrict the on-chain trading function of its bSTOCK tokens at all, giving users a second path to hold their bSTOCK, namely:

On-chain users (no KYC required) can directly use stablecoins such as USDC or sDAI to purchase bSTOCK

This actually breaks through the KYC restrictions, and the trading experience is no different from trading ordinary on-chain tokens, which is easier to promote among web3 users. An ERC-20 token with no restrictions also opens the door to composability for tokenized stock holders, such as pairing with stablecoins to form liquidity with an average APY of 33%. This may also be the reason why Backed Finances TVL is close to 10 times that of Dinari.

In terms of compliance, the entity behind Backed Finance is registered in Switzerland, and the above-mentioned tokenized stocks corresponding to ERC-20 tokens can be freely transferred business model has been recognized by European regulators ( source ). Backed Finance also disclosed the reserve certificate audited by The Network Firm.

However, the US SEC has not yet commented on Backed Finances business. The securities traded by Backed are all US stocks. It is good to obtain permission from Switzerland, where it is registered, but what is more important is how the US regulatory authorities evaluate this business model.

Among other projects, SwarmXs business model is consistent with Backed Finance, but its business scale and compliance details are significantly different from Backed Finance.

Although the market value of Backed Finance’s tokenized stocks is ten times that of Dinari, its asset size of more than 20 million US dollars and TVL of 8 million are still not high, and transactions on the chain are not active. The reasons are:

There are not enough use cases for tokenized stocks on the chain. Currently, they can only be used as LPs. The advantages of composability have not been fully utilized. Of course, this may be related to the concerns of related lending, stablecoin and other protocols about the legitimacy of this model.

More importantly, liquidity is insufficient. Backed itself is not an exchange, and there is no natural liquidity to support its tokenized stock trading. Under the current model, the liquidity of its tokenized stocks depends on the issuer, including how many tokenized stocks the issuer is willing to hold and how much liquidity it is willing to add to LP. From the current perspective, Backeds issuer has no intention of increasing investment in this area.

If the SEC can further clarify the regulatory framework and determine the feasibility of the Backed model, both of the above points may improve.

xStocks

In May of this year, the US exchange Kraken announced that it would cooperate with Backed Finance and Solana to launch xstocks.

On June 30, the xStocks product was officially launched. In addition to Backed, Kraken and Solana, its partners include centralized exchanges Kraken and Bybit, decentralized exchanges Raydium and Jupiter on Solana, lending protocol Kamino, Dex Byreal incubated by Bybit, oracle Chainlink, payment protocol Alchemy Pay and brokerage Alpaca.

Source: xStocks official website

The legal structure of xStocks products is completely consistent with Backed Finance. It currently supports more than 200 stock products, and Krakens trading hours are 5*24. From the perspective of partnerships, Kraken, Bybit, Jupiter, Raydium and Byreal are all exchanges that support xStocks; Kamino can support xStocks as collateral, and Kamino Swap can also trade xStocks; Solana is the public chain running xStocks; Chainlink is responsible for reserve reporting; Alpaca is a cooperative broker;

At present, since the product has just been launched, the data statistics are not perfect and the transaction volume is not large. However, compared with Backed Finance’s own products, xStocks has more key partners:

On the Cex side, there are Kraken and Bybit, which are more likely to leverage existing market makers and users to provide better liquidity for xStocks;

On the chain, there are various Dex and Kamino. Kamino is the first to provide other use cases for tokenized U.S. stocks besides being an LP. In the future, other protocols may support xStocks to further expand its composability.

From this perspective, although xStocks has just been launched, I believe that xStocks will soon surpass existing players and become the largest issuer of tokenized US stocks.

Robinhood

Robinhood, which has been actively developing its crypto business, also submitted a report to the SEC in April 2025, hoping that the SEC would establish an RWA regulatory framework that includes tokenized stocks. In May, Bloomberg reported that Robinhood would create a blockchain platform to allow European investors to invest in U.S. stocks, with the alternative public chains being Arbitrum or Solana.

Also on June 30, Robinhood officially announced the launch of a tokenized U.S. stock trading product for European investors. The product supports dividend payments and 24/5 access time.

Robinhoods tokenized stock product was initially issued based on Arbitrum. In the future, its tokenized stock underlying will run on Robinhoods own L2, which is also based on Arbitrum.

However, according to Robinhood’s official documents , its current tokenized stock products are not real tokenized stocks, but contracts that track the corresponding US stock prices. The relevant assets are safely held by US licensed institutions in Robinhood Europe accounts. Robinhood Europe issues contracts and records them on the blockchain. Its tokenized stocks can currently only be traded on Robinhood and are not allowed to be transferred.

Other players who are planning

In addition to the products mentioned above that have already been launched, there are many other players who are planning to tokenize U.S. stocks, including:

Solana

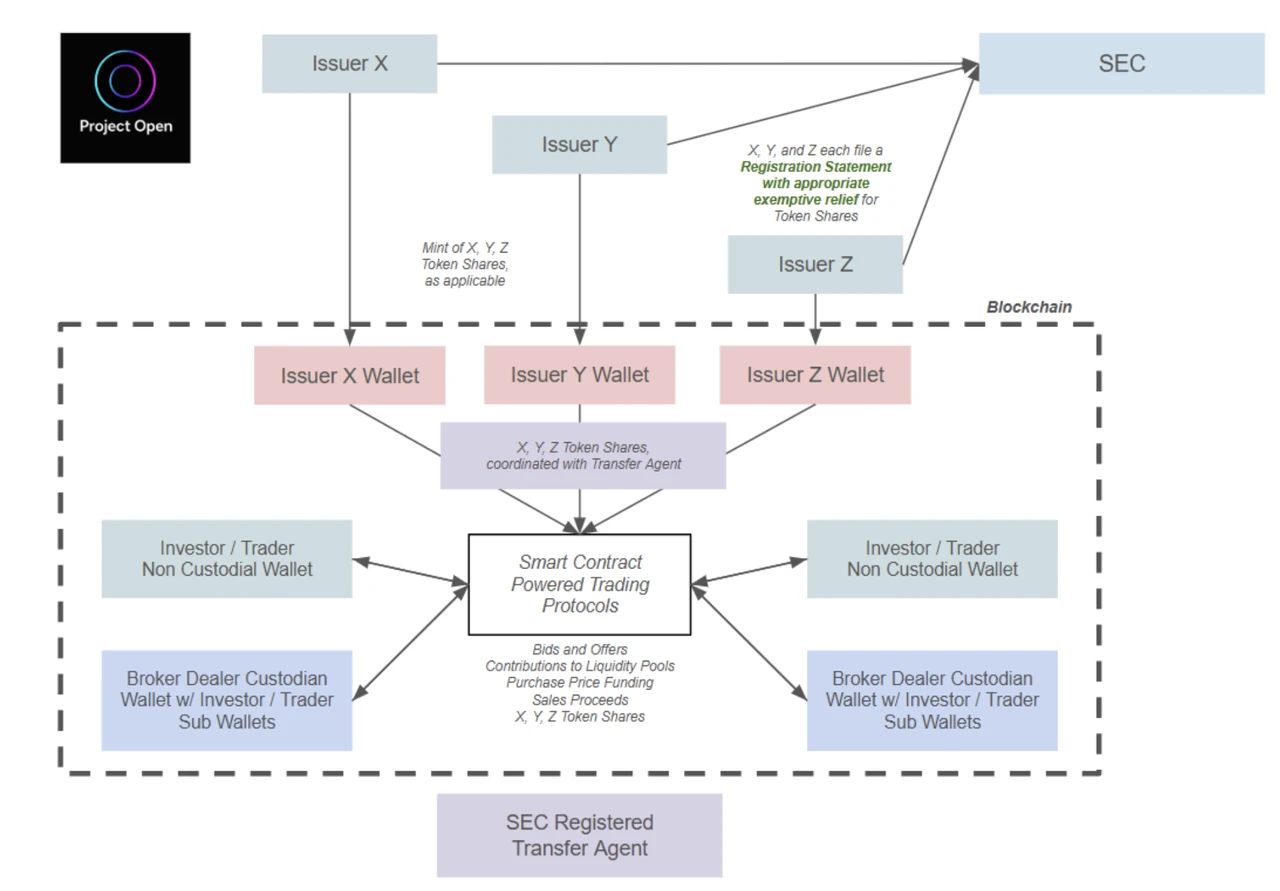

Solana attaches great importance to tokenized stocks. In addition to the xStocks mentioned above, Solana has also established the Solana Policy Institute (SPI), aimed at educating policymakers why decentralized networks like Solana are the future infrastructure of the digital economy . One of the two projects currently being promoted is that they have established a project called Project Open, aimed at achieving compliant blockchain-based securities issuance and trading, using blockchain technology to create a more efficient, transparent and accessible capital market while maintaining strong investor protection . In addition to SPI, members of Project Open include Dex Orca on the Solana chain, RWA service provider Superstate, and law firm Lowenstein Sandler LLP.

Project Open began submitting public written opinions to the SECs Crypto Working Group several times in April this year. The SEC Crypto Working Group also held a meeting with it on June 12 to discuss the issue. After the meeting, Project Open members submitted further explanations of their business.

The tokenized U.S. stock issuance and trading process advocated by Project Open is as follows:

Source: SEC official website documents

The process is summarized as follows:

Issuers need to apply for SEC approval in advance, after which they can issue tokenized US stocks

Users who want to buy tokenized US stocks need to complete KYC in advance, after which they can use cryptocurrency to purchase tokenized US stocks issued by the above issuers

The transfer agent registered with the SEC records the transfer of shares on the chain

Project Open also specifically proposed that it hopes the SEC will allow peer-to-peer tokenized US stock trading through smart contract protocols, that is, tokenized US stock holders can trade in AMMs, thus opening the door to on-chain composability. However, according to the framework proposed in the document, all users holding tokenized US stock shares must complete KYC. In order to implement the above process, Project Open applied for an 18-month exemption relief or confirmatory guidance for many operations (see references for details).

In general, Project Open’s solution is based on the existing solution of Backed Finance and adds KYC requirements. From my point of view, it is almost certain that this solution will be passed during the term of the SEC, which is more tolerant of DeFi. The only question is when it will be passed.

Coinbase

As early as 2020, when Coinbase applied for NASDAQ listing, its application documents included the idea of issuing tokenized COIN on the chain, but it was abandoned because it did not meet the requirements of the SEC at the time. Recently, Coinbase is seeking a no-action letter or exemptive relief from the SEC for its tokenized stock business. However, there is no detailed document information at present, and we can only get a confirmed message from the press release:

Coinbase’s tokenized stock trading program is now open to U.S. users.

This is the main difference from other current tokenized stock market players, and it also allows Coinbase to compete directly with Internet brokers such as Robinhood and traditional brokers such as Charles Schwab. Of course, this has far less impact on web3 investors than it does on Nasdaq:COIN.

Ondo

Ondo, which has achieved success in the Treasury RWA market (see Mint Ventures previous article for more information on Ondo), has also long planned to conduct tokenized U.S. stock business. According to their documents, their tokenized U.S. stock products have the following features:

Available to non-US users

Trading hours are 24*7

Tokens are minted and destroyed in real time

Allows the use of tokenized US stock assets as collateral

Judging from the above feature descriptions, Ondo’s products are quite similar to the new framework proposed by Solana. Ondo also proposed at Solana’s Accelerate conference to launch tokenized U.S. stock products on the Solana network.

Ondo’s tokenized U.S. stock product, Ondo Global Markets, is scheduled to launch later this year.

The above is the current status of the tokenized U.S. stock market, as well as the status of several other players who are making plans.

In terms of the fundamental motivation of demand, the main purpose of users buying tokenized stocks is to profit from stock price fluctuations. They are concerned about the liquidity, repayment ability and KYC-free transactions of the trading venue. Whether there must be a compliant organization to carry out tokenization is not a point of concern for users. Therefore, the web3 market has always used derivatives to provide users with U.S. stock trading products.

Providing US stock trading through derivatives

Currently, the main providers of US stock derivatives services are Gains Network (in Arbitrum and Polygon) and Helix (in Injective). Their users do not actually trade US stocks, so there is no need to tokenize US stocks.

Its core product logic is equivalent to applying the perpetual contract logic to US stocks, which is usually:

Trading users do not need KYC, use stablecoins as collateral, and allow leveraged trading

Trading hours are the same as US stock trading hours

The underlying price is directly read from a trusted data source, such as using Chainlink

Use funding rates to balance the difference between the on-site price and the fair price

However, whether it is the current Gains and Helix or the previous Synthetix and Mirror, the platforms that use synthetic assets to trade US stocks have not brought too high actual trading volume. Currently, the average daily trading volume of Helixs US stock products does not exceed 10 million US dollars, while Gains daily trading volume is less than 2 million US dollars. The reasons may be:

This form has obvious regulatory risks, because although they do not actually provide US stock trading, they have in fact become exchanges for users to trade US stocks, and regulatory authorities have clear requirements for the supervision of any exchange, and KYC is the most basic part of supervision. If the platform is not well-known, the regulator may not have time to pay attention to it, but if the platform becomes more popular, it will easily be targeted by regulators.

The above products do not have sufficient liquidity to support users real trading needs. The liquidity of the above products needs to be solved on their own, and cannot rely on any third party, and the above products cannot bring users real available trading depth.

Helixs US stock foreign exchange product trading volume and the order book of the most traded COIN

On the centralized exchange side, Bybit recently launched a US stock trading platform based on MT5. Its products also adopt the logic similar to perpetual contract products. It does not conduct actual transactions in US stocks, but uses stablecoins as collateral to trade indexes.

In addition, the Shift project, which has not yet been launched, has introduced the concept of Asset-Referenced Tokens (ART), which is said to enable KYC-free US stock trading. Its product process is as follows:

Shift buys US stocks and pledges them at compliant brokers such as Interactive Brokers, using Chainlink as proof of reserves

Shift uses the reserved U.S. stocks to issue reference asset tokens ART. Each ART has a corresponding U.S. stock asset behind it, but ART is not a tokenized U.S. stock.

C-end users can purchase ART tokens without KYC

Shifts solution maintains 100% correspondence between ART and the underlying US stocks, but ART is not a tokenized US stock and does not have stock ownership, dividend rights, and voting rights. Therefore, it is not subject to various regulatory rules on securities, thus achieving the KYC-free feature ( source) .

Of course, from a regulatory perspective, ART is not allowed to be anchored to securities assets. It is not clear how the shift team intends to implement the goal of anchoring ART to U.S. stocks, and it is not certain whether the specific product plans to be launched can really follow the above process. However, this plan also realizes KYC-free U.S. stock transactions through certain loopholes in the regulatory terms, which deserves continued attention.

What kind of tokenized U.S. stock products does the market need?

Regardless of the method of tokenizing U.S. stocks, the core process is as follows:

Tokenization: The process is usually handled by compliance agencies, and proof of reserves is regularly produced. In essence, users who meet KYC requirements purchase U.S. stocks and then put them on the chain. This step is not much different between the various solutions.

Trading: C-end users trade tokenized stocks. This is where the differences between the various solutions lie: some do not allow trading (Exodus), some only allow trading through traditional brokerage channels (Dinari and mystonks.org), and some support on-chain trading (Backed Finance, Solana, Ondo, Kraken). Even more special is Backed Finance, which currently supports users without KYC to purchase its tokenized US stock products directly through AMM through the Swiss compliance framework.

For C-end users, the tokenization process mainly focuses on compliance and asset security. At present, most current market players can ensure these two points well. The main focus is on the transaction process. For example, Dinari can only trade through traditional brokerage channels, and it does not provide liquidity mining, lending and other services for tokenized stocks. In this case, the significance of stock tokenization is largely eliminated. Even if the compliance is perfect and the process is perfect, it is difficult to attract users.

Solutions such as xStocks, Backed Finance, and Solana are more meaningful tokenized U.S. stock solutions in the long run. After tokenization, U.S. stocks are not traded through traditional brokerage channels, but on the chain. This can more effectively utilize the 7*24 availability and composability advantages brought by DeFi.

However, in the short term, on-chain liquidity will be difficult to match the liquidity of traditional channels. Low-liquidity exchanges are equivalent to being unavailable. If the venues that provide tokenized US stocks cannot attract more liquidity, then the influence of tokenized US stocks will also be difficult to expand. This is why I am optimistic that xStocks will soon become a tokenized US stock exchange.

From this perspective, if the regulatory framework becomes clearer and tokenized U.S. stock products become popular in web3, the exchanges that will eventually gain more trading market share may still be those that currently have better liquidity and more trader users.

In fact, we can also see from the few examples in the last cycle: Synthetix, Mirror and Gains all launched products that include US stock trading in 2020, but the most influential US stock trading product is FTX. FTXs solution is actually similar to the current Backed Finance solution, but FTXs stock trading volume and AUM are much higher than the latecomer Backed Finance.

Potential investment targets

Although there is huge market space for tokenization of U.S. stocks, there are not many investment targets available for investors to choose from at present.

Among the existing players, neither Dinari nor Backed Finance has issued tokens. Dinari has also made it clear that it will not issue tokens. Only the Meme token stonks corresponding to mystonks.org can be regarded as a potential investment target.

Among the players who are actively deploying, the token market value of Coinbase, Solana and Ondo is already relatively high, and their main business is not tokenized U.S. stocks. The promotion of tokenized U.S. stocks will have a certain impact on their tokens, but the extent of the impact is difficult to predict.

xStocks’ partners include Solana’s leaders Dex Raydium and Jupiter, as well as lending protocol Kamino, but it’s unlikely that this collaboration will bring significant improvements to the aforementioned protocols.

Among the members of SPIs Project Open: Phantom and Superstate have not yet issued tokens, only Orca has issued tokens.

Among the derivative projects, Helix has not yet issued a coin, and only GNS is an optional target.

Since the above projects have different business categories and different forms of participation in tokenized U.S. stocks, we are unable to compare their valuations. We only list the basic information of the relevant tokens as follows:

References

https://x.com/xrxrisme69677/status/1925366818887409954

https://www.odaily.news/post/5204183

Project Open related information:

The framework first filed in April: https://www.sec.gov/files/ctf-written-project-open-wireframe-04282025.pdf

On June 12, the SEC Crypto Working Group met with the Project Open team to discuss https://www.sec.gov/files/ctf-memo-solana-policy-institute-et-al-061225.pdf

On June 17, SPI updated the proposal framework and submitted supplementary materials on the meeting content with Phantom, Superstate, and Orca.

SPI updated proposal framework: https://www.sec.gov/files/project-open-chain-equities-infrastructure-061725.pdf

SPI Supplementary Information: https://www.sec.gov/files/project-open-061725.pdf

Phantom: https://www.sec.gov/files/phantom-technologies-061725.pdf

Superstate: https://www.sec.gov/files/ctf-superstate-letter-061725.pdf

Orca: https://www.sec.gov/files/orca-creative-061725.pdf

The Exemptive Relief or Confirmatory Guidance for Project Open applications includes:

Blockchain, as a technological tool, does not itself require or mandate any SEC registration.

Blockchain network fees are technology costs and are not securities trading-related fees.

Peer-to-peer transactions conducted through smart contract protocols are permitted and are not regulated equivalents to transactions on an exchange or alternative trading system (ATS) (because they are bilateral transactions, such as those contemplated by section 4(a)(1) of the 33 Act).

Provides an exemption for broker-dealers engaging in section 4(a)(1) transactions (in a limited management role).

Non-custodial/self-custodial wallets (and their issuers) are not broker-dealers.

Allows holding tokenized shares in non-custodial/self-custodial wallets that have passed appropriate whitelisting and KYC.

Broker-dealers may create sub-wallets for clients to hold their tokenized shares, which constitutes appropriate “possession and control” of the securities for broker-dealer custody purposes.

Transfer agents, if they have KYC information of whitelisted wallet owners and modern qualified investor education information, can use blockchain to perform their duties. a) Ability to enforce transfer restrictions. b) Ability to enforce restrictive legends (e.g., securities held by related parties).

A Registration Statement can be used to register tokenized shares after obtaining appropriate exemptions. a) Will propose - specific content and form requirements. b) Will propose - the method of periodic reporting.

The purchase of Shares directly from the Issuer in the manner contemplated above will not make the purchaser an underwriter or broker-dealer; such purchases are not being made in the capacity of a broker or dealer.

Appropriate exemptions from Reg NMS (e.g., Order Protection Rule, Best Execution, Access Rule, etc.).