Original author: 100y

Original translation: TechFlow

Key Takeaways

Visa and Mastercard are the two major operators of the global payment network. It is no exaggeration to say that they almost dominate the global payment market. It is estimated that the total global payment transaction volume will reach 20 trillion US dollars by 2024. If card payments can be processed through blockchain networks in the future, this will bring huge development opportunities to the blockchain and stablecoin industries.

Although the front-end experience of todays payment system has been greatly improved due to the innovation of various fintech companies, the back-end system that actually processes transactions still relies on outdated technology. There are still many problems in settlement and cross-border payments, and blockchain provides an exciting solution to these problems.

In April this year, Visa and Mastercard respectively announced their roadmaps for blockchain and stablecoin applications. Both companies have launched relevant plans in the following areas: 1) card services linked to stablecoins; 2) settlement systems based on stablecoins; 3) peer-to-peer international remittances; 4) institutional tokenization platforms. It remains to be seen who will take the lead in the Web3 payment market.

“Visardilo Crocodilo” and “Tralalero Mastercara”, two characters that symbolize “brain-opening” in the payment field, are fighting for the next generation of payment systems. Yes, for financial companies, adopting blockchain and stablecoin-related technologies has become an obvious choice.

1. Background - Can blockchain be used for payments?

1.1 Two Giants of Traditional Payment

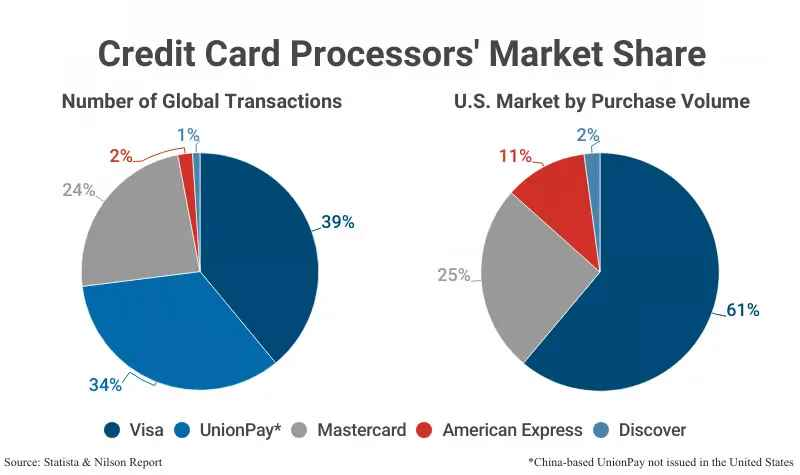

Source: Statista and Nilson

Visa and Mastercard are the worlds leading payment network companies. By 2024, Visa will account for 39% of the global payment market and Mastercard for 24%. Given that China UnionPay mainly processes transactions based in the domestic Chinese market, it is no exaggeration to say that Visa and Mastercard almost dominate the global payment landscape.

Both companies make huge profits by providing card payment networks that process transactions between consumers and merchants and settle settlements between card issuers and acquirers for a small fee. (We’ll explore the payment process in more detail below.) In fact, Visa and Mastercard are expected to have operating margins of 67% and 57%, respectively, in 2023. This reflects the low fixed cost nature of their network businesses based on large transaction volumes.

According to Upgraded Points, card network payment transaction volume in the United States alone is expected to reach approximately $10.5 trillion in 2024. Combined with China UnionPays domestic transaction volume, the global transaction volume is expected to be approximately $20 trillion. If card payment processing is carried out through blockchain networks in the future, this will bring huge opportunities to the blockchain and stablecoin industries.

1.2 Card payment process

Visa and Mastercard both operate open card payment networks that use the four-party model including card issuers, acquirers, merchants, and cardholders. Visa and Mastercard do not directly issue cards or provide loans, but only provide payment networks. The basic process of the four-party model widely used in the United States is as follows:

Payment Request ( D+0: Transaction Day): When a cardholder makes a purchase at a merchant, he or she initiates a payment request through the card. The payment information is passed from the merchant to the acquirer, then to the card network, and finally to the card issuer.

Payment Authorization Day ( D+0: Transaction Day): The card issuer checks the cardholders credit limit, card validity, and whether there are signs of fraud, and then decides whether to approve the payment. The approval information is returned to the merchant in reverse order, completing the transaction.

Settlement ( D+3: 3rd business day after transaction): The issuer pays the acquirer after deducting the settlement fee, and the acquirer pays the merchant after deducting the merchant fee. The card network charges network fees to the issuer and acquirer from each transaction.

Billing and Repayment ( D+ 30: 30th working day after the transaction): The cardholder receives a bill from the card issuer in the following month and repays the amount due.

1.3 Can blockchain be used for payment?

Over the past few decades, a variety of fintech services related to payments have emerged, starting with PayPal and later on Stripe, Square, Apple Pay, and Google Pay. These services have brought innovation on the front end, allowing users to complete payments more easily and quickly than ever before. However, the back-end processes that actually execute payments have remained virtually unchanged. As a result, several issues remain with the existing payment system.

The first issue is settlement time.

In the traditional payment process, most merchants and acquirers process transactions in daily batches. This batch processing usually takes place once a day. In addition, settlements are usually processed only on weekdays, so if holidays or weekends are involved, the overall settlement time may be extended.

The second problem is the high costs of international transactions.

When the card issuer and the merchant are in different countries, cross-border funds transfer is required during the authorization and settlement process. This will add about 1% cross-border transaction fees and 1% foreign exchange fees, making international payments more expensive than domestic payments.

There is a system that can solve both problems: blockchain. As a decentralized network, blockchain can operate 24 hours a day, regardless of national borders, and can achieve fast settlement and low fees even for international transactions. Based on these advantages, Visa and Mastercard have actively adopted stablecoins and blockchain technology in their payment networks in recent years. So, how do they use blockchain specifically?

2. Key point: The payment war has begun

Visas Four Strategies

Source: Visa

Visa operates one of the worlds largest payment networks, VisaNet, which can process up to 65,000 transactions per second and supports payments at 150 million merchants in more than 200 countries. Visa sees stablecoins as a core component of the future digital payment system and announced four specific strategic initiatives in April this year to integrate stablecoins into existing payment networks.

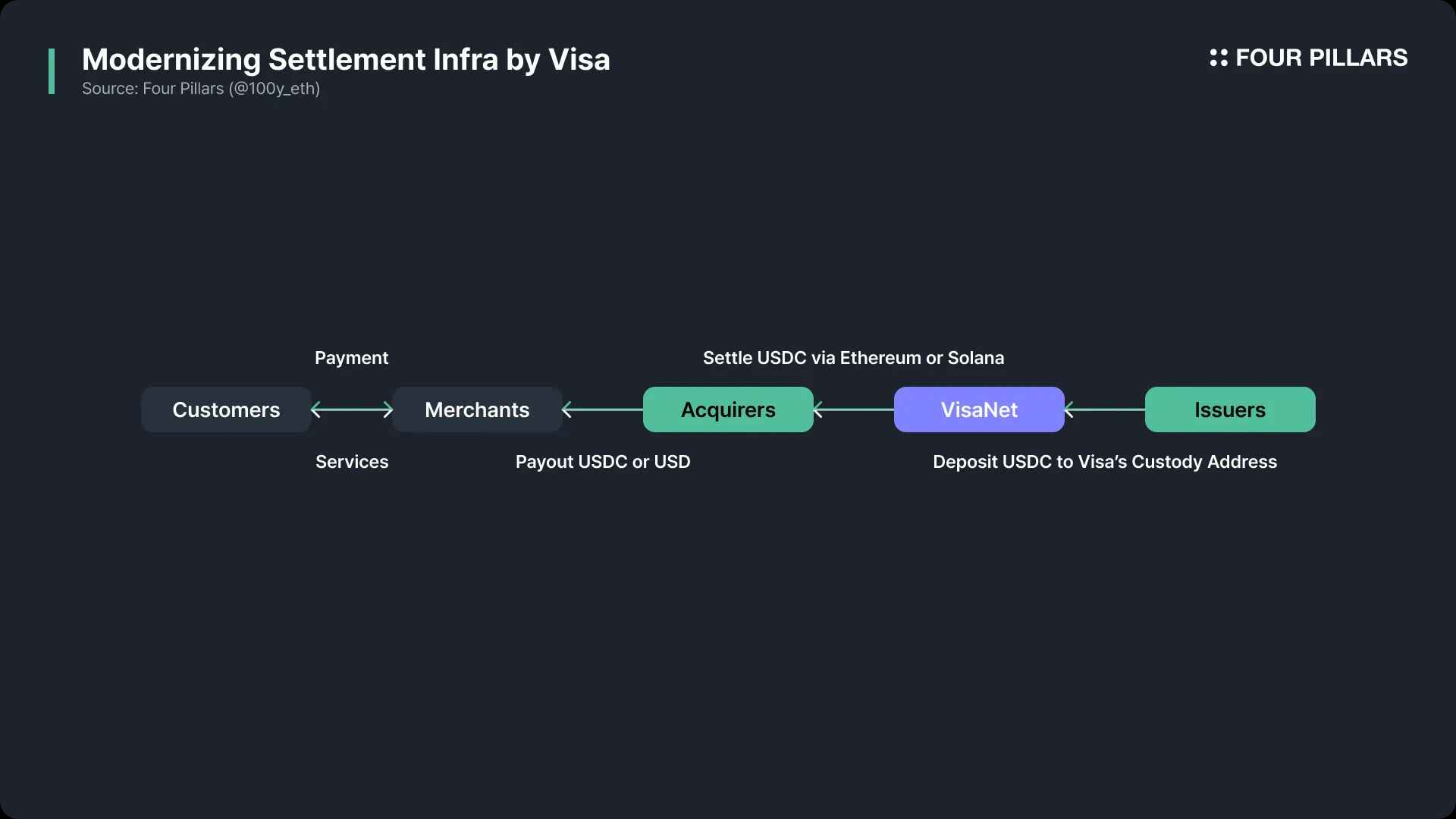

1. Modernization of settlement infrastructure

Since 2021, Visa has started a pilot program to use USDC (US dollar stablecoin) for payment settlement through its existing VisaNet network. So far, more than $225 million in settlements have been completed. Traditionally, card issuers need to remit funds to Visa in US dollars for settlement, but now they can also use USDC directly for settlement . This not only improves settlement efficiency, but also reduces cross-border transaction fees.

For example, the Crypto.com Visa card offered by Crypto.com allows users to pay through their cryptocurrency accounts. In the past, these cryptocurrency-focused companies needed to convert digital assets into fiat currencies such as the U.S. dollar to complete payment processing, a time-consuming and costly process. Now, they can settle directly with USDC. In cooperation with Anchorage, Visa created custodial accounts to safely store stablecoins. Card issuers like Crypto.com can transfer stablecoins to these accounts through the Ethereum network to complete settlement.

By eliminating the need to convert cryptocurrencies into fiat and transfer them across borders, Crypto.com has reduced average upfront payment time from eight days to four days and reduced foreign exchange fees to 20 to 30 basis points .

Visa not only allows card issuers to use USDC for settlement, but also launches the function of allowing acquirers to use USDC for settlement directly . In September 2023, Visa established a settlement infrastructure for acquirers such as Worldpay and Nuvei, allowing them to receive USDC through the Ethereum and Solana networks. Acquirers can pass USDC to merchants or convert it into fiat currency as needed.

In summary, Visa has successfully built a pipeline that enables card issuers to settle with acquirers in USDC instead of USD through the Visa network. In the future, Visa plans to expand this stablecoin settlement system to more partners and regions, implement 24/7 real-time settlement, and support multiple blockchains and stablecoins.

2. Strengthening global remittance infrastructure

Visa already supports large-scale cross-border transactions through the VisaNet infrastructure. One of its services, Visa Direct, allows peer-to-peer fund transfers through cards, wallets, and account numbers, covering payment scenarios between friends and between businesses and customers. Visa plans to further improve the efficiency of global remittances by integrating stablecoins into Visa Direct. In addition, Visa recently invested in BVNK , a startup that develops stablecoin infrastructure for enterprises, aiming to expand its stablecoin capabilities beyond the retail sector to cover the enterprise ecosystem.

3. Launching programmable digital currency

One of the main advantages of stablecoins over traditional cash is the ability to leverage smart contracts on the blockchain. Visa has focused heavily on the potential of automated financial services based on smart contracts and announced the launch of the Visa Tokenized Asset Platform (VTAP) in October 2024.

VTAP is a blockchain-based financial infrastructure that allows banks and financial institutions to issue and manage digital tokens based on fiat currencies (such as stablecoins and tokenized deposits). Since these functions are provided through Visas API, integration with existing financial systems becomes very easy. Tokens issued through VTAP can be used in conjunction with smart contracts to automate complex processes such as conditional payments or customer loans.

Currently, VTAP has not been publicly released and is still running in a sandbox environment. Initially, it tested token issuance, transfer and redemption functions in cooperation with Spanish bank BBVA. According to the roadmap, Visa plans to start a pilot project for real customers on the Ethereum public blockchain in 2025.

4. Develop stablecoin recharge and withdrawal cards

Visa is helping card issuers provide on-ramp and off-ramp services through stablecoin-linked cards. To date, Visa has processed more than $100 billion in cryptocurrency purchases and $25 billion in cryptocurrency spending through its cards. To expand this ecosystem, Visa is working with stablecoin card infrastructure companies such as Bridge, Baanx, and Rain.

Bridge is a stablecoin infrastructure platform acquired by Stripe. Recently, Bridge has partnered with Visa to launch a card issuance solution that enables users to use stablecoins for real-world payments. Fintech companies can provide users with card services associated with stablecoins through Bridges simple API. Cardholders can pay directly with their stablecoin balances, and Bridge converts the stablecoins into cash and pays the merchant. Currently, the service is online in Argentina, Colombia, Ecuador, Mexico, Peru and Chile, and plans to gradually expand to Europe, Africa and Asia.

Baanx is a London-based fintech company founded in 2018 that focuses on connecting traditional finance with digital assets. In April 2025, Baanx announced a partnership with Visa to launch a stablecoin payment card that allows users to pay directly with USDC in their self-hosted crypto wallets. During the payment process, USDC is sent to Baanx in real time via a smart contract, which then converts it into fiat currency to complete merchant settlement.

Rain is a New York-based fintech company founded in 2021 that operates a global card issuance platform based on stablecoins. Rain provides APIs to facilitate enterprises to issue Visa cards linked to stablecoins, and also provides a variety of financial services including 24/7 real-time payment settlement, tokenization of credit card receivables, and automation of settlement processes through smart contracts.

Mastercards full-chain stablecoin payment solution

Source: Mastercard

Mastercard, like Visa, is one of the leading companies in the global payment network space. Unlike Visa, which processes payments through its high-processing centralized network, VisaNet, Mastercard processes payments through Banknet, a powerful distributed structure supported by more than 1,000 data centers around the world. On April 28, 2025, Mastercard announced that it had built an end-to-end infrastructure covering the entire stablecoin-based payment ecosystem, from wallets to checkout functions.

1. Card issuance and payment support

Mastercard has partnered with several crypto wallets (such as MetaMask), crypto exchanges (such as Kraken, Gemini, Bybit, Crypto.com, Binance, and OKX), and fintech startups (such as Monavate and Bleap) to provide stablecoin payment services.

MetaMask has partnered with Mastercard and Baanx to launch the MetaMask card, which allows users to use crypto assets stored in MetaMask for card payments. Payment settlement is completed in the background through Monavates solution, which connects the Ethereum network to Mastercards Banknet and converts cryptocurrencies into fiat currencies. The MetaMask card will first be launched in Argentina, Brazil, Colombia, Mexico, Switzerland, the United Kingdom and the United States.

Mastercard has also partnered with the above-mentioned crypto exchanges to support users to make payments using stablecoins in their accounts.

2. Provide USDC settlement support for merchants

Despite the growing popularity of stablecoin-based payments, most merchants still prefer to settle in fiat currencies. However, if merchants have demand, Mastercard also supports settlement in USDC through partnerships with Nuvei and Circle. In addition to USDC, Mastercard also supports settlement in stablecoins issued by Paxos through its partnership with Paxos.

3. On-chain remittance support: Mastercard Crypto Credential service

Sending stablecoins through blockchain has the advantages of being simple, fast and low-cost. However, when applying it to real life, user experience, security and compliance remain the main challenges. To this end, Mastercard launched the Mastercard Crypto Credential service, which allows users of crypto exchanges to create aliases through a verification process and conveniently send stablecoins through these aliases. Visa and Mastercard are actively expanding the application scenarios of stablecoin payments, from card issuance to on-chain settlement to merchant support. They have promoted the integration of blockchain technology and traditional payment systems through in-depth cooperation with fintech companies, crypto wallets and exchanges. This marks an important step forward for stablecoin payments on a global scale, and also lays the foundation for the future development of the crypto industry.

Mastercards Crypto Credential service simplifies the users payment experience on the blockchain through an alias system, eliminating the need to enter complex crypto wallet addresses, and greatly improving user-friendliness. In addition, if the recipients wallet does not support a specific cryptocurrency or blockchain before the transfer, the transaction will be blocked in advance to prevent asset loss. In terms of compliance, Mastercard automatically exchanges the Travel Rule data required for international remittances to meet regulatory requirements and ensure transaction transparency. Currently, exchanges that support the service include Wirex, Bit 2 Me and Mercado Bitcoin. The service has been launched in Latin American countries such as Argentina, Brazil, Chile, Mexico and Peru, as well as European countries such as Spain, Switzerland and France.

4. Enterprise Tokenization Platform

The Multi-Token Network (MTN) launched by Mastercard is a private blockchain-based service designed to help financial institutions and enterprises issue, destroy and manage tokens and enable real-time cross-border transactions. The following are some application cases of MTN:

Ondo Finance tokenized its US Treasury-backed short-term bond fund (OUSG) and integrated it into MTN. This enables businesses to purchase and redeem OUSG in real time around the clock without relying on traditional financial infrastructure, while also earning a stable return.

JPMorgan Chase has integrated its blockchain payments system Kinexys with MTN to support the real-time payment needs of businesses.

In May 2024, Standard Chartered Bank conducted a pilot project through MTN to successfully tokenize and trade carbon credits as part of a proof of concept.

The time to fight for Web3 payment market dominance

As the US governments support for cryptocurrencies becomes increasingly clear, the adoption of blockchain and stablecoins in various industries continues to grow. As one of the core functions of the blockchain network, financial infrastructure naturally attracts the attention of payment network giants such as Visa and Mastercard. The two companies are actively developing the next generation of payment infrastructure.

Notably, both Visa and Mastercard released plans for blockchain and stablecoin payment systems in April 2025 (Visa released its announcement on the role of stablecoins on April 30, 2025, and Mastercard revealed its full-chain capabilities for stablecoin transactions on April 28, 2025). Both companies highlighted the following four areas: 1) Stablecoin-related card services; 2) Enterprise tokenization platform; 3) Stablecoin settlement system; 4) Peer-to-peer (P2P) remittances.

This suggests that Visa and Mastercard are competing for dominance in the Web3 payment market.

Will the adoption of blockchain payment systems bring about a major disruption to existing market shares and competitive dynamics? The authors believe that the next generation of systems will significantly change the payment infrastructure itself, but will not significantly change market shares or competitive structures. Blockchain payment systems will improve the efficiency of settlement and international transactions, which will help companies optimize their revenue models and enhance competitiveness. However, the market share of the payment industry ultimately depends on the business and marketing relationships with merchants, acquirers, and issuers. These relationships have been deeply rooted after decades of development, so the application of blockchain may not significantly change the competitive landscape.

Resource Links: